|

|

|

|

|||||

|

|

|

Energy Transfer LP ET is one of the most diversified midstream companies in the United States, with strategically located assets that span natural gas, natural gas liquids (NGLs), crude oil and refined products. The firm owns and operates, either through wholly owned subsidiaries or joint ventures, an extensive network of natural gas gathering pipelines, processing plants, treating and conditioning facilities, with a combined processing capacity of nearly 12.9 Bcf/d.

Energy Transfer’s midstream operations center on gathering, compression, treating, blending and processing of natural gas, with assets strategically located across key producing basins and major shale regions of the United States. A significant share of these midstream assets is integrated with the firm’s intrastate transportation, storage and NGL infrastructure.

Natural gas produced from some wells fails to meet downstream pipeline standards or commercial use requirements. Energy Transfer addresses this issue by using its treating plants to remove carbon dioxide, hydrogen sulfide and other impurities, ensuring the gas meets pipeline quality specifications. The firm’s midstream segment primarily generates results from margins on natural gas gathered, transported, bought and sold through pipelines, as well as from natural gas and NGL volumes processed and treated at its facilities.

Energy Transfer’s integrated midstream system, strengthened by scale efficiencies and long-term, fee-based contracts, enables it to maintain steady cash flow generation.

Collectively, these assets provide a strong competitive moat, positioning Energy Transfer as a compelling investment option for both income-oriented investors and those seeking long-term growth.

Midstream assets provide pipeline operators with a competitive edge by ensuring steady cash flows through fee-based contracts, enhancing operational integration across gathering, processing, storage and transportation. These assets also offer diversification, reduce exposure to commodity price volatility and support long-term growth in energy demand.

Kinder Morgan KMI benefits from its vast natural gas pipeline and storage network, generating stable fee-based revenues. Similarly, The Williams Companies WMB leverages its midstream assets, particularly in the Marcellus and Utica shales, to capture growing natural gas demand. Both firms gain resilience, diversification and consistent cash flows from their integrated midstream platforms.

Units of ET have risen 10.8% in the past year compared with the Zacks Oil and Gas - Production Pipeline - MLB industry’s growth of 3.5%.

The Zacks Consensus Estimate for Energy Transfer’s 2025 and 2026 earnings per unit indicates year-over-year growth of 8.59% and 11.15%, respectively.

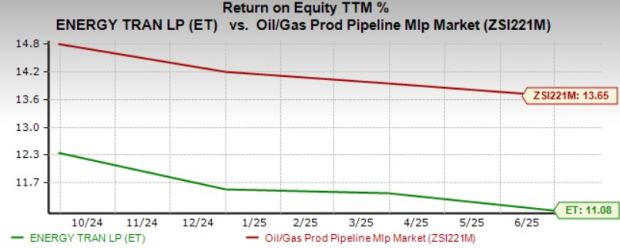

Energy Transfer’s trailing 12-month return on equity (“ROE”) is 11.08%, lower than its industry average of 13.85%. ROE, a profitability measure, indicates how effectively a company utilizes its shareholders’ funds to generate income.

Energy Transfer currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-16 | |

| Feb-15 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite