|

|

|

|

|||||

|

|

|

Bumble BMBL is facing mounting challenges as revenues for its flagship Bumble app dropped 7.6% year over year to $201.4 million in the second quarter of 2025. The real concern lies in the shrinking paying user base. Bumble App Paying Users fell 11% to 2.5 million, signaling a deeper problem of user churn.

While Bumble raised its Average Revenue Per Paying User (ARPPU) by 4%, this uptick wasn’t enough to offset the loss of subscribers. Higher ARPPU can offer temporary relief, but with fewer users, engagement drops, matches become harder to find and monetization potential erodes.

The outlook doesn’t inspire confidence either. Management projects Bumble app revenues of $204-$208 million for the third quarter of 2025, down 9%-12% year over year. This cautious outlook underscores the difficulty of reversing churn, even with pricing tweaks and new premium features.

To counter this, Bumble is betting on innovation beyond dating. Its revamped Bumble For Friends app, powered by AI-driven discovery and community tools, aims to capture the growing social networking trend. While this could unlock new growth avenues, the immediate challenge remains retaining core dating users.

If the slowdown continues at its current pace, it could hurt Bumble's long-term growth much more than revenue volatility.

Match Group MTCH faces churn at Tinder, with paying users down 5% year on year to about 14.1 million in the second quarter of 2025, yet its multi-brand strategy and Hinge's double-digit growth have cushioned the blow. By contrast, Bumble leans heavily on a concentrated portfolio. Match Group is also scaling AI-driven matchmaking faster, strengthening engagement. Crucially, its superior operating and net profit margins highlight resilience and financial flexibility, clear advantages over Bumble’s negative margins, making Match Group a more competitive player in the dating app landscape.

Grindr GRND leverages its niche LGBTQ+ community to drive exceptional engagement, with users averaging nearly an hour daily, far outpacing Bumble’s declining retention, where paying users fell 8.7% and total users dropped to 50 million by mid-2025. Unlike Bumble, Grindr is expanding MAUs and revenues through feature-led monetization, including “Right Now,” “Albums,” “Roam,” and its AI “Wingman.” With stronger ARPU growth, payer penetration, and a rising subscriber base, Grindr demonstrates superior retention and monetization strength.

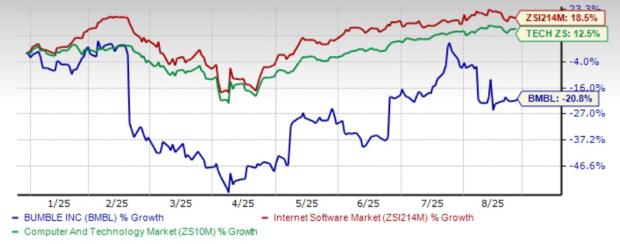

Shares of Bumble have declined 20.8% in the year-to-date period against the Zacks Computer and Technology sector’s growth of 12.5% and the Zacks Internet - Software industry’s 18.5% return.

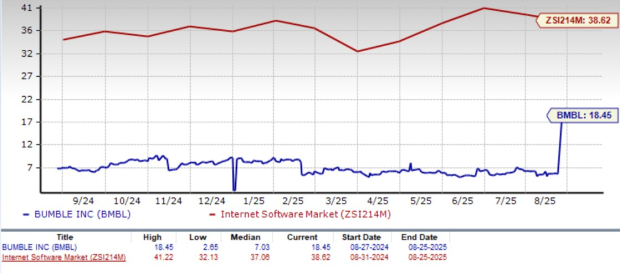

From a valuation standpoint, Bumble trades at a significant discount with a forward P/E of approximately 18.45X, notably below the Zacks Internet - Software industry average of 38.62X. Bumble carries a Value Score of B.

The Zacks Consensus Estimate for Bumble’s 2025 revenues is pegged at $970.56 million, indicating a 9.43% year-over-year decline, with earnings expected to improve by 61.2%, narrowing the loss to $1.79 per share.

Bumble Inc. price-consensus-chart | Bumble Inc. Quote

Bumble stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 15 hours | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 |

Match Group Revenue Ticks Down as Tinder Continues to Weigh on Results

MTCH MTCH -7.49%

The Wall Street Journal

|

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-02 | |

| Jul-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite