|

|

|

|

|||||

|

|

|

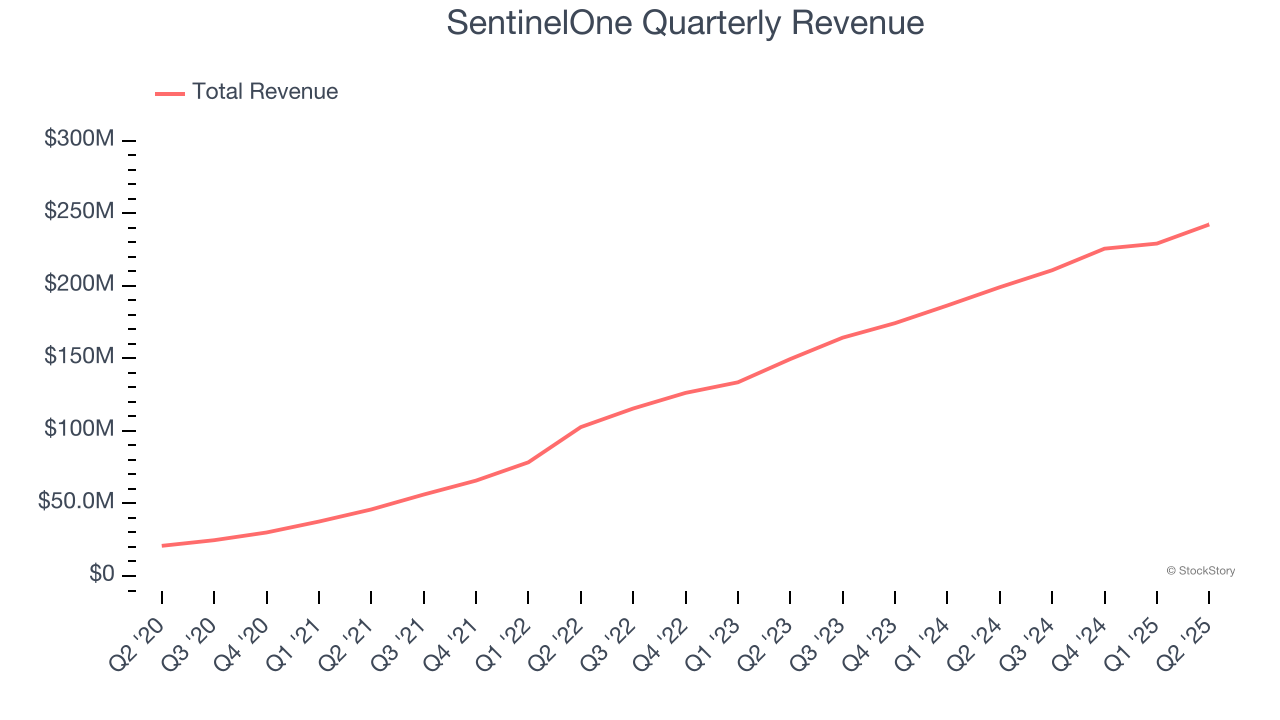

Cybersecurity AI platform provider SentinelOne (NYSE:S) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 21.7% year on year to $242.2 million. The company expects next quarter’s revenue to be around $256 million, close to analysts’ estimates. Its non-GAAP profit of $0.04 per share was $0.01 above analysts’ consensus estimates.

Is now the time to buy SentinelOne? Find out by accessing our full research report, it’s free.

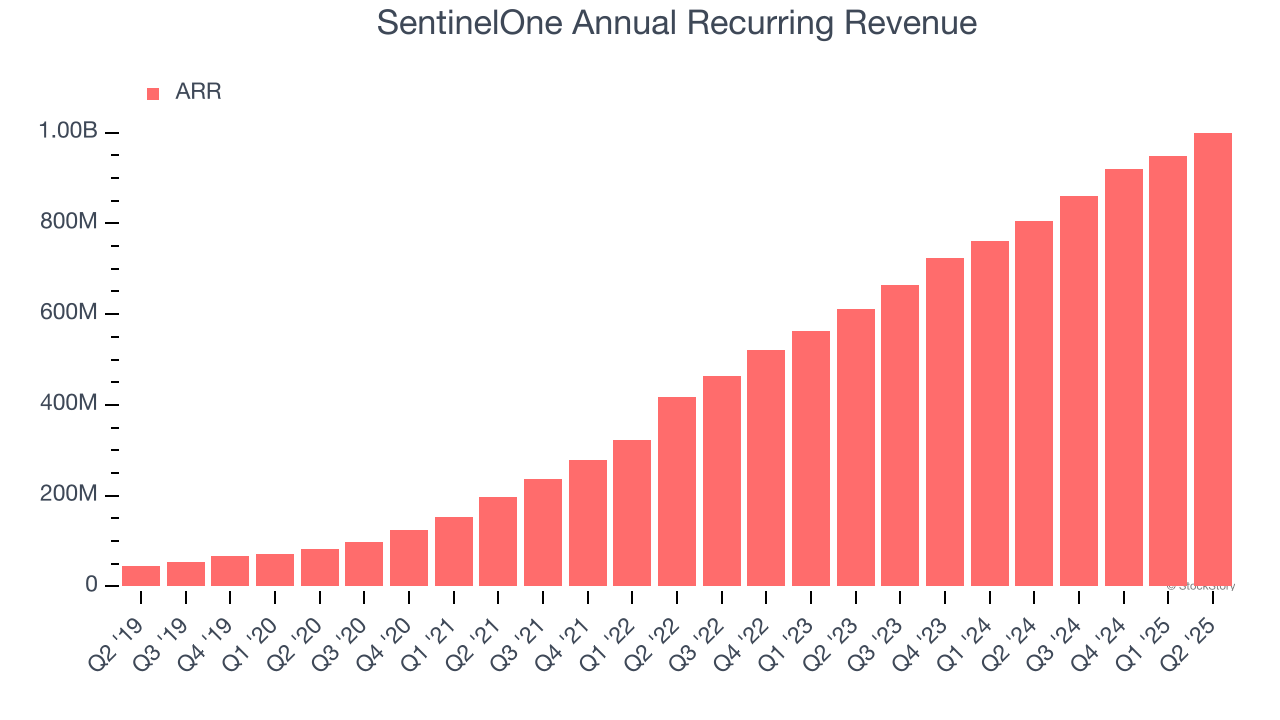

“We surpassed $1 billion in ARR and delivered record net new ARR, continuing to deliver robust growth and platform adoption across AI, data, cloud, and endpoint,” said Tomer Weingarten, CEO of SentinelOne.

Built on the principle of "fighting machine with machine," SentinelOne (NYSE:S) provides an AI-powered cybersecurity platform that autonomously prevents, detects, and responds to threats across endpoints, cloud workloads, and identity systems.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, SentinelOne’s sales grew at an incredible 44.2% compounded annual growth rate over the last three years. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

This quarter, SentinelOne’s year-on-year revenue growth of 21.7% was excellent, and its $242.2 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 21.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 21% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is healthy and implies the market is forecasting success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

SentinelOne’s ARR punched in at $1 billion in Q2, and over the last four quarters, its growth was fantastic as it averaged 26.2% year-on-year increases. This performance aligned with its total sales growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes SentinelOne a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

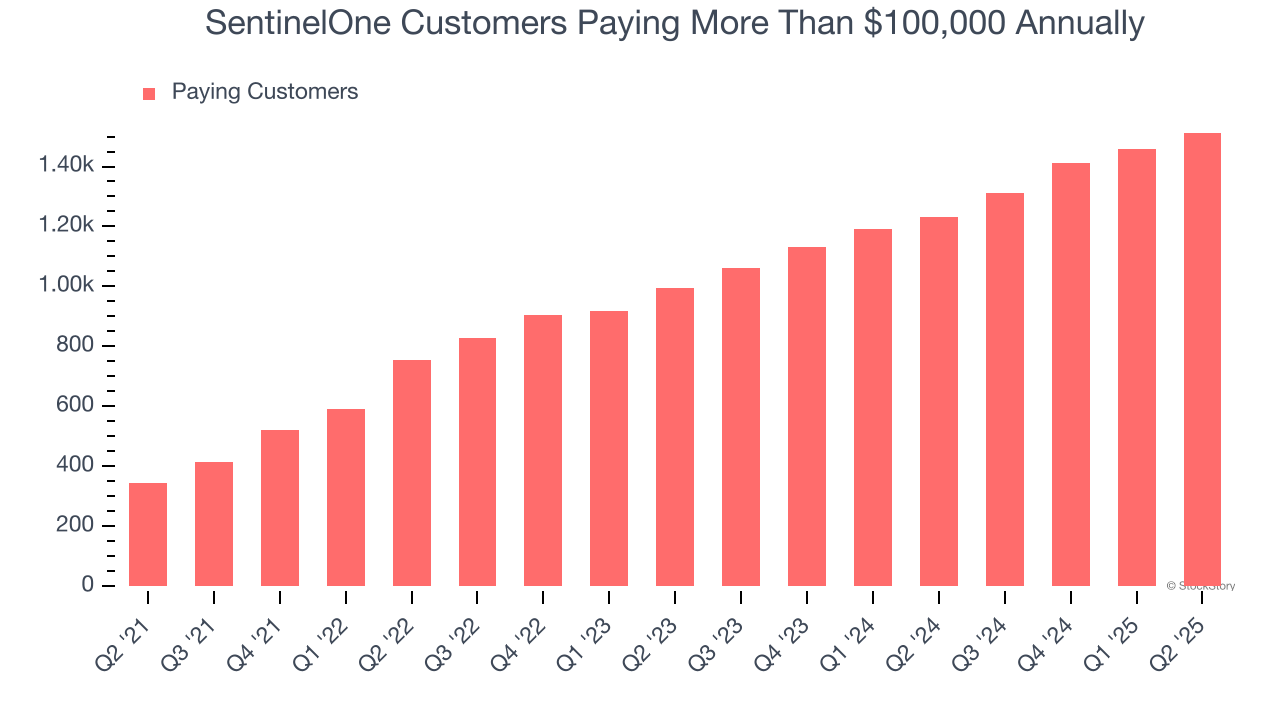

This quarter, SentinelOne reported 1,513 enterprise customers paying more than $100,000 annually, an increase of 54 from the previous quarter. That’s quite a bit more contract wins than last quarter but also quite a bit below what we’ve observed over the previous year. This indicates the company is optimizing its go-to-market strategy to reinvigorate growth.

It was good to see SentinelOne narrowly top analysts’ annual recurring revenue expectations this quarter. Full-year sales guidance was also in line with analysts' estimates. Zooming out, we think this was a decent quarter. The stock traded up 6.9% to $18.85 immediately after reporting.

So do we think SentinelOne is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| 10 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite