|

|

|

|

|||||

|

|

|

The Cooper Companies, Inc. COO delivered third-quarter fiscal 2025 adjusted earnings per share (EPS) of $1.10, which improved 15% year over year. The figure beat the Zacks Consensus Estimate of $1.07 by 2.8%. Operational improvements drove the bottom-line growth.

GAAP EPS for the quarter was 49 cents, down 6% year over year.

Revenues totaled $1.06 billion, up 6% year over year on a reported basis. The figure, however, missed the Zacks Consensus Estimate by 0.5%.

The quarterly revenues were up 3% year over year at constant exchange rate (CER) and 2% on an organic basis.

The lower-than-expected top-line performance was mainly due to weakness in Clariti sales, caused by a noticeable drop in Asia Pac and a slowdown in the Americas and EMEA.

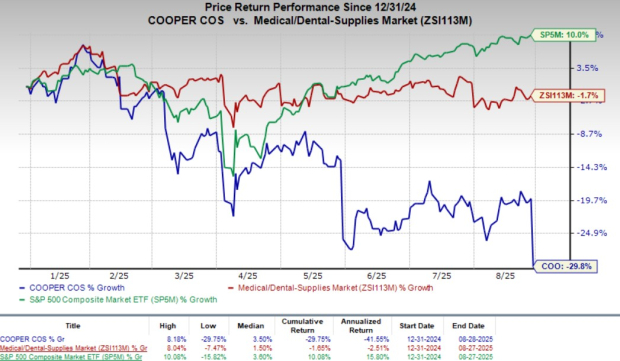

Following a mixed result, shares of COO were down 12.9% on Aug. 28. The company’s shares have lost 29.8% so far this year compared with the industry’s decline of 1.7%. The S&P 500 Index was up 10% during the same period.

COO conducts its business via two reportable segments — CooperVision (“CVI”) and CooperSurgical (“CSI”).

For the third quarter of fiscal 2025, the CVI segment’s revenues totaled $718.4 million, up 6% year over year on a reported basis and 2% at CER as well as organically. This figure compares to our segmental projection of $717.6 million.

Growth was led by strong momentum in MyDAY, which posted double-digit gains with multifocal lenses rising 20%, and continued strength in MiSight myopia management lenses, which grew 23% and delivered a record quarter in EMEA.

Category-wise, CVI derives revenues from Toric and multifocal, Sphere and others.

In the fiscal third quarter, Toric and multifocal revenues totaled $358.8 million, up 10% year over year on a reported basis, and up 6% organically as well as at CER. This figure compares to our projection of $355.6 million.

Sphere, other revenues totaled $359.6 million, up 3% year over year on a reported basis but down 1% at CER as well as organically. This figure compares to our projection of $361.9 million.

Geographically, CVI derives revenues from the Americas, Europe, and Asia Pacific.

Americas revenues totaled $286 million, up 2% year over year on a reported basis and up 3% at CER and organically. The figure compares to our projection of $296.9 million.

EMEA revenues amounted to $292.1 million, up 14% year over year on a reported basis and up 6% at CER and organically. This figure compares to our projection of $271.2 million.

Asia Pacific revenues in the fiscal third quarter totaled $140.3 million, up 1% year over year reportedly but down 5% organically and at CER due to Clariti weakness and softness in e-commerce channels. This figure compares to our projection of $149.5 million.

The CSI segment’s revenues totaled $341.9 million, which moved up 4% on a reported basis as well as at CER, and 2% organically. This figure compares to our projection of $344.4 million.

Category-wise, CSI derives revenues from Office and surgical, and Fertility.

In the fiscal third quarter, Office and surgical revenues totaled $204.8 million, up 3% on a reported basis and at CER, and up 1% organically. This figure compares to our projection of $193.4 million. Sales in this category are benefiting from double-digit growth in the labor and delivery portfolio and robust momentum in specialty surgical devices, including a 23% gain from obp Surgical. However, PARAGARD sales declined 10% following advanced purchases earlier in the year.

Fertility revenues in the fiscal third quarter amounted to $137.1 million, up 6% on a reported basis, up 3% organically and up 4% at CER year over year, supported by genomics and consumables and market share gains in EMEA. This figure compares to our projection of $133.2 million.

In the quarter under review, Cooper Companies’ adjusted gross profit rose 6.8% to $713.4 million. The adjusted gross margin expanded almost 100 basis points (bps) to 67%, supported by favorable product mix, efficiency gains and FX tailwinds. We had projected 67.8% of gross margin for the fiscal third quarter.

Selling, general and administrative expenses rose 10.7% to $421.7 million. Research and development expenses increased 14.4% to $44.6 million. Adjusted operating costs totaled $437 million, reflecting a 6.2% increase from the prior-year quarter’s level.

Adjusted operating profit totaled $276.4 million, reflecting an 11% increase from the year-earlier quarter’s level. The adjusted operating margin in the fiscal third quarter remained flat at 26%.

COO exited the third quarter of fiscal 2025 with cash and cash equivalents of $124.9 million compared with $116.2 million at the end of the fiscal second quarter.

Total debt at the end of the fiscal third quarter was $2.48 billion compared with $2.77 billion at the end of the fiscal second quarter.

Cooper Companies has updated its outlook for fiscal 2025.

The company now expects revenues to be in the range of $4,076-$4,096 million (prior $4,107-$4,146 million), suggesting an organic improvement of 4-4.5% from the prior-year figure. The Zacks Consensus Estimate is pegged at $4.12 billion.

COO expects the CVI segment’s revenues to be in the range of $2,734-$2,747 million (previously $2,759-$2,786 million), suggesting an organic improvement of 4-5% from the year-earlier registered figure.

The company anticipates the CSI segment’s revenues to be in the range of $1,343-$1,349 million (prior $1,347-$1,359 million), indicating an organic improvement of 3-3.5% from the year-earlier figure.

For the entire fiscal year, adjusted EPS is expected to be in the $4.08-$4.12 range (previously $4.05-$4.11). The Zacks Consensus Estimate is pegged at $4.06.

The Cooper Companies, Inc. price-consensus-eps-surprise-chart | The Cooper Companies, Inc. Quote

The Cooper Companies’ third-quarter results highlight mixed performance, with earnings beating estimates but sales missing the same. Moreover, the company lowered its sales outlook for fiscal 2025 but raised its EPS view.

Sales likely fell short of expectations due to clariti softness and e-commerce weakness in Asia Pacific. However, margins expanded meaningfully, and management raised its earnings outlook on the back of strong operational execution. With continued MyDAY and MiSight expansion, fertility market opportunities, and organizational restructuring aimed at driving efficiencies, the company is well-positioned to outpace its markets and deliver sustainable shareholder value.

The company’s innovation pipeline remains central to growth. MyDAY is expected to gain further traction with new launches such as MyDAY Energys in Europe and multifocal introductions in APAC, alongside ongoing toric expansions. MiSight is poised for expansion with regulatory approval secured in Japan and commercialization planned for early 2026.

Fertility remains a compelling long-term market opportunity, supported by demographic shifts and rising treatment access. Meanwhile, organizational restructuring and IT investments are expected to enhance efficiency and leverage artificial intelligence for long-term operational benefits.

COO currently has a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader medical space that have announced quarterly results are Medpace Holdings, Inc. MEDP, West Pharmaceutical Services, Inc. WST and Boston Scientific Corporation BSX.

Medpace Holdings, sporting a Zacks Rank #1 (Strong Buy) at present, reported second-quarter 2025 EPS of $3.10, which beat the Zacks Consensus Estimate by 3.3%. Revenues of $603.3 million outpaced the consensus mark by 11.5%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Medpace Holdings has a long-term estimated growth rate of 11.4%. MEDP’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 13.9%.

West Pharmaceutical reported second-quarter 2025 adjusted EPS of $1.84, which beat the Zacks Consensus Estimate by 21.9%. Revenues of $766.5 million surpassed the Zacks Consensus Estimate by 5.4%. It currently flaunts a Zacks Rank #1.

West Pharmaceutical has a long-term estimated growth rate of 8.5%. WST’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

Boston Scientific reported second-quarter 2025 adjusted EPS of 75 cents, which beat the Zacks Consensus Estimate by 4.2%. Revenues of $5.06 billion surpassed the Zacks Consensus Estimate by 3.5%. It currently carries a Zacks Rank #2 (Buy).

Boston Scientific has a long-term estimated growth rate of 14%. BSX’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 8.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 7 hours | |

| 9 hours | |

| 13 hours | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite