|

|

|

|

|||||

|

|

|

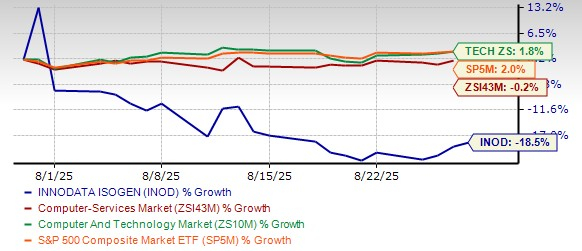

Innodata Inc. INOD, one of the fastest-growing names in AI data engineering, has seen its shares tumble 18.5% over the past month. The stock has sharply underperformed its peer set, with the Zacks Computer - Services industry down just 0.2% and the broader Zacks Computer and Technology sector up 1.8% over the same period. By comparison, the S&P 500 gained 2%.

At $39.51 as of Aug. 28, 2025, the stock trades at a 44% discount to its 52-week high of $71 but still commands a premium of more than 200% to its 52-week low of $13.02. This positioning underscores both the volatility and investor debate around the name: is Innodata’s pullback an opportunity to buy a growth leader on sale, or does it reflect deeper risks that merit caution?

INOD’s 1-Month Share Performance

Innodata’s share performance reflects both optimism and volatility. Shares soared above $65 in February 2025 amid the generative AI boom but have since retraced. As of Aug. 28, 2025, the stock closed at $39.51, with technical indicators flashing caution.

The stock is currently trading below its 50-day SMA of $45.88 and slightly under its 200-day SMA of $42.41, a bearish setup that suggests weakness in both short- and long-term momentum. Trading volume has normalized after earlier spikes, signaling that speculative froth has cooled, but investor conviction remains tepid. Unless strong catalysts emerge, the technical picture implies the stock could remain range-bound near-term, even as fundamentals remain supportive.

Project-Based Revenue Model and Visibility Risks: Innodata’s Digital Data Solutions segment, its largest contributor, relies heavily on project-based contracts that are largely at-will. This structure introduces revenue volatility, as large projects may be scaled back, delayed, or canceled at short notice. Customer concentration compounds this risk: in second-quarter 2025, the largest client alone contributed $33.9 million, more than half of total revenues. Dependence on a handful of customers makes Innodata vulnerable to shifts in budgets or vendor preferences.

Heavy Reliance on Key Customers: Despite rapid growth, Innodata remains highly concentrated in a limited set of large technology clients. In second-quarter 2025, its largest customer alone contributed nearly $34 million of revenue—more than half of total sales. Such reliance exposes the firm to potential volatility. Any slowdown, budget reallocation, or contract termination from these few marquee accounts could significantly disrupt performance.

Competitive Pressures in a Crowded Market: The market for generative AI training and evaluation data is becoming increasingly competitive. Scale AI’s prominence, coupled with well-funded new entrants, raises the bar on execution. While Innodata emphasizes data quality and domain expertise, rivals may compete on pricing or vertically integrated offerings. Moreover, consolidation trends—where large tech companies acquire or build in-house data capabilities—could limit Innodata’s addressable market or pressure margins.

Innodata faces rising competition from C3.ai AI, Palantir Technologies PLTR, and BigBear.ai BBAI. C3.ai continues to push enterprise AI applications that overlap with Innodata’s services. Palantir, with deep government and commercial ties, competes for large-scale AI budgets where Innodata also seeks traction. Meanwhile, BigBear.ai, though smaller, is scaling quickly in defense and logistics AI, creating overlap with Innodata’s project-driven business. The presence of C3.ai, Palantir and BigBear.ai underscores the crowded field in which Innodata must differentiate on quality and execution.

Rising Operating Investments: While the company delivered strong EBITDA gains, it is deliberately ramping investments in talent, delivery capacity, and product innovation. In second-quarter 2025 alone, Innodata spent about $1.4 million in growth initiatives, with plans to step this up in the second half. These investments, while strategically necessary, could weigh on near-term margins. If revenue conversion lags behind expense growth, operating leverage could turn negative, impacting profitability.

Geopolitical and Macroeconomic Uncertainty: Innodata’s filings also highlight exposure to macro and geopolitical risks. Management cites ongoing conflicts in regions such as Russia-Ukraine, Israel-Iran, and India-Pakistan as potential disruptors. Given its global delivery model, instability in offshore operations could affect service continuity, labor costs, or customer perceptions. Broader risks tied to U.S. monetary policy, interest rates, and global trading conditions further add uncertainty to customers’ technology budgets. Any sustained slowdown in AI spending cycles due to macroeconomic headwinds could dampen demand for Innodata’s services.

Strong Q2 Performance and Raised Guidance: Innodata posted a standout second-quarter 2025. Revenues climbed 79% year over year to $58.4 million, EPS of 20 cents beat by 81.8%, and adjusted EBITDA soared to $13.2 million, or 23% of sales, versus just 9% in the prior-year quarter. Net income swung to $7.2 million from a small loss last year. On the back of this momentum, management lifted its full-year organic revenue growth guidance to at least 45%, up from 40% previously. This “beat-and-raise” quarter illustrates execution strength and a demand backdrop that remains exceptionally strong.

Expanding Relationships With Big Tech: Growth is anchored by deepening ties with top technology players. Innodata’s largest customer generated nearly $33.9 million in revenues during the second quarter, and new project wins are expanding the engagement pipeline. Another major technology client is expected to contribute $10 million in the second half of 2025, up from just $200,000 across the prior 12 months. These step-ups highlight Innodata’s growing role as a trusted partner in the generative AI ecosystem, with multi-year potential to scale.

Leadership in Generative and Agentic AI: Beyond revenue wins, Innodata is positioning itself as a frontier player in “smart data”—high-quality, complex datasets required to improve model factuality, safety, and reasoning. Management sees Agentic AI as the next catalyst, enabling autonomous systems and robotics with real-world applications. CEO Jack Abuhoff even suggested a forthcoming “ChatGPT moment for robotics,” where Innodata’s simulation data and evaluation services could open massive new addressable markets. This forward-looking positioning helps justify its elevated valuation relative to peers.

Solid Balance Sheet and Investment Capacity: Liquidity provides another growth lever. Innodata closed second-quarter 2025 with $59.8 million in cash and an undrawn $30 million credit facility, ensuring flexibility to scale operations. The company continues to invest aggressively—roughly $1.4 million in the second quarter alone—on product innovation, go-to-market initiatives, and talent, while still projecting higher adjusted EBITDA for 2025 than in 2024. This combination of profitability and reinvestment highlights Innodata’s ability to balance growth and financial discipline.

Innodata trades at a forward 12-month P/E ratio of 42.3x, compared to just 16.4x for the industry average. This valuation gap means the stock is priced for perfection. Any miss on earnings, slowdown in revenue growth, or delay in customer projects could trigger a sharp downside, as investors reassess whether Innodata deserves such a premium. The market is currently less forgiving of richly valued stocks, particularly in the AI space, where hype cycles can swing sentiment quickly.

INOD’s P/E Ratio (Forward 12-Month) vs. Industry

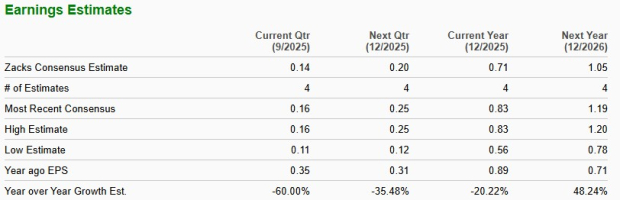

The 2025 EPS estimates have ticked up to 71 cents from 69 cents over the past month. However, the figure still represents a 20% year-over-year decline. Yet, earnings are expected to grow 23.6% in 2026.

By contrast, revenues are projected to rise nearly 43%. This divergence signals that heavy investment in expansion—while necessary for long-term positioning—may weigh on near-term profitability, leaving earnings leverage muted.

Innodata’s second quarter confirmed its role as a critical enabler of the generative AI ecosystem, with marquee customers, strong profitability gains, and a raised growth outlook. Its positioning in Agentic AI and robotics offers an exciting multi-year runway. A strong balance sheet further supports aggressive investment in growth.

Yet, near-term risks are meaningful: stretched valuation multiples, projected EPS declines despite revenue expansion, and a technical chart that shows weakening momentum. For now, Innodata looks best suited as a Hold—consistent with its current Zacks Rank #3 (Hold). This stance allows investors to maintain exposure to its long-term AI growth story while waiting for either a better entry point or stronger signals of sustained profitability. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 20 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 4 hours | |

| 8 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite