|

|

|

|

|||||

|

|

|

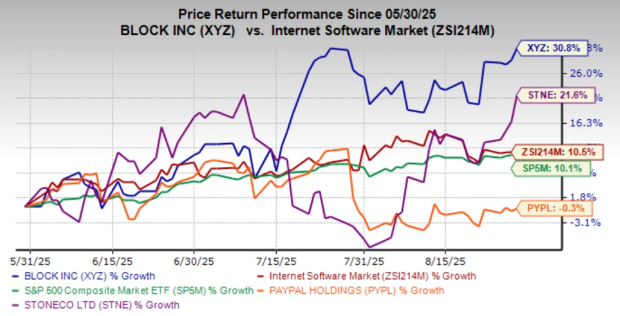

Block XYZ, the parent of Cash App and Square, has staged an impressive 30.8% rally over the past three months, outpacing many fintech peers. The run-up reflects investors’ optimism around the company’s improving profitability and continued product innovation.

Block has seen encouraging updates recently. In Canada, Purdys Chocolatier adopted Square’s modern POS and retail solutions across more than 80 locations, enhancing efficiency and customer engagement with features like Square Register, handheld devices, marketing tools, gift cards and DoorDash integration. In the United States, Block expanded Afterpay’s BNPL services via a partnership with Caleres, a leading footwear company, offering flexible payments at brands like Famous Footwear and Sam Edelman.

XYZ stock has not only outpaced its peers, such as PayPal Holdings, Inc. PYPL and StoneCo Ltd. STNE, but also outperformed the S&P 500 composite over the same time frame. In the past three months, PayPal shares have declined 0.3%, while StoneCo shares have appreciated 21.6%.

Yet, as with many high-growth financial technology stocks, the story is nuanced. Block’s strengths in ecosystem expansion and margin improvements stand against persistent challenges in revenue momentum, competition and exposure to volatile segments like Bitcoin. With these dynamics in mind, let’s evaluate whether Block is a buy, hold or sell after its recent surge.

Block’s second quarter of 2025 painted a mixed picture. On one hand, the company reported a 1.6% year-over-year revenue decline to $6.05 billion, falling short of expectations. This softer top-line performance suggests macroeconomic pressures on discretionary consumer spending, as well as a more competitive payment landscape.

On the other hand, the gross profit climbed 13.6% to $2.54 billion, underscoring that the company’s business model is scaling more efficiently. Cash App, the crown jewel of Block’s ecosystem, posted $1.5 billion in gross profit, up 15.6% year over year, while Square reported an 11.3% gross profit increase. Even more encouraging, adjusted operating income surged 37.7%, with margins expanding 400 basis points on a year-over-year basis to 22%, reflecting both disciplined expense management and growing leverage in its platform.

This profitability trajectory marks a shift in Block’s narrative — from a hyper-growth disruptor prioritizing expansion to a fintech company demonstrating that it can balance growth with sustainable returns.

The biggest driver behind Block’s momentum is Cash App, which has evolved into far more than a peer-to-peer payments platform. It now functions as a multi-service financial hub, particularly for younger, digitally native consumers. With products spanning payments, banking, commerce and Bitcoin transactions, Cash App is broadening its role in users’ financial lives.

Innovations such as Cash App Pools (enabling group payments), Afterpay integrations (strengthening buy-now-pay-later capabilities) and enhanced borrowing features are deepening customer engagement. These offerings allow Block to cross-sell services, drive stickiness and capture more wallet share.

Meanwhile, Square — Block’s merchant-facing ecosystem — remains solid. Double-digit growth in gross payment volume (GPV) alongside innovations like Square AI tools and Tap to Pay on iPhone highlights the company’s efforts to keep Square competitive in the evolving point-of-sale and software landscape. Together, Cash App and Square form a powerful dual ecosystem that positions Block as a unique player aiming to become a comprehensive financial operating system.

Despite its strengths, Block faces material headwinds. First, competition in digital payments is intensifying. PayPal continues to command stronger merchant acceptance globally, while Apple Pay and other wallet providers are expanding their reach. In consumer finance, established banks and emerging fintechs are vying for the same demographics that Block targets. Maintaining Cash App’s growth trajectory in such a crowded space will require relentless innovation and marketing spend. Second, Bitcoin remains a meaningful part of Block’s strategy, but it also adds volatility.

Finally, Block is still highly concentrated in the U.S. market and heavily reliant on a younger demographic base through Cash App. While this has fueled strong growth to date, geographic and demographic concentration may limit long-term resilience compared with more globally diversified peers.

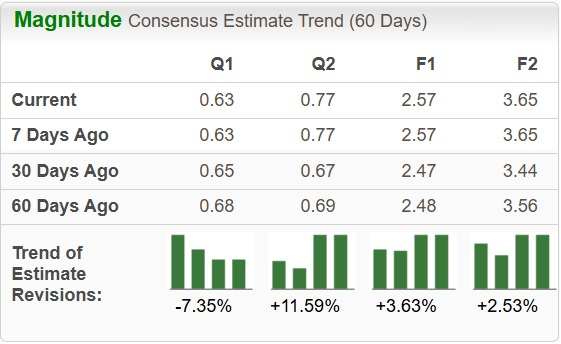

The consensus estimate for Block’s 2025 sales calls for a year-over-year rise of 2.02%, while that for EPS suggests a 23.7% decline year over year. However, EPS estimates have also been trending northward over the past month.

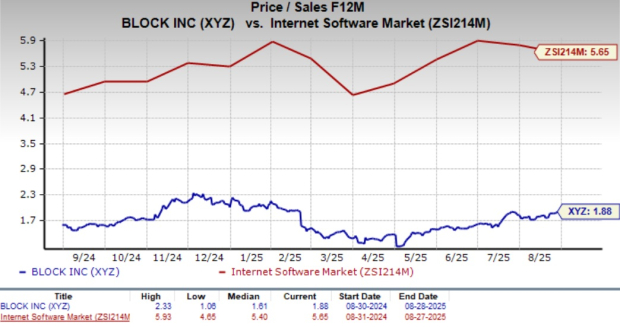

Block shares are overvalued, as suggested by the Value Score of D. In terms of forward 12-month Price/Sales (P/S), Block is trading at 1.88X, below its industry’s 5.65X, but ahead of its one-year median of 1.61X. XYZ is also trading at a premium to StoneCo, which is trading at a forward 12-month P/S of 1.74X.

Block’s recent rally reflects renewed confidence in its path toward profitability. Investors are rewarding management’s ability to expand margins while sustaining double-digit gross profit growth. Still, the stock now trades at a richer multiple than it did earlier in the year, implying that much of the near-term optimism may already be priced in.

With ongoing competition and macro uncertainties, it may be premature to view Block as a clear-cut buy despite its solid fundamentals. Yet, the company’s ability to execute on product innovation and margin expansion suggests that it is far from a sell. For now, maintaining a position in XYZ seems prudent as it navigates challenges while unlocking new growth avenues.

At present, Block carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-03 | |

| Jul-03 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 | |

| Jul-01 | |

| Jul-01 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-29 | |

| Jun-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite