|

|

|

|

|||||

|

|

|

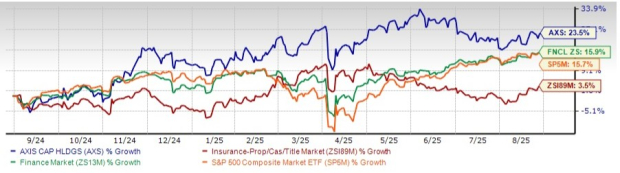

Shares of AXIS Capital Holdings Limited AXS have gained 23.5% in the past year, outperforming its industry, the Finance sector and the Zacks S&P 500 composite’s growth of 3.5%, 15.9% and 15.7%, respectively.

AXIS Capital has outperformed its peers, The Travelers Companies, Inc. TRV and Cincinnati Financial Corporation CINF, which have risen 18.5% and 11.9%, respectively, in the past year. Meanwhile, shares of Kinsale Capital Group, Inc. KNSL have lost 7.3% in the same time frame.

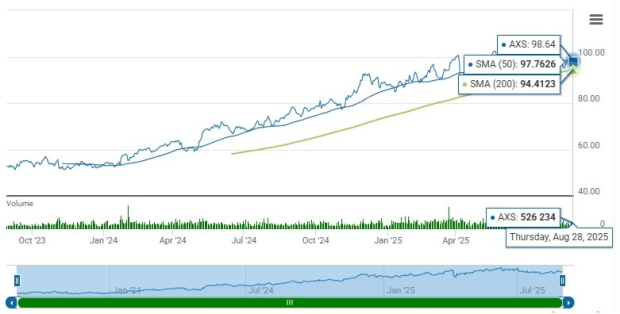

Shares of AXIS Capital closed at $98.64 on Thursday, near its 52-week high of $107.19. This proximity underscores investor confidence. It has the ingredients for further price appreciation.

The insurer has a market capitalization of $7.71 billion. The average volume of shares traded in the last three months was 0.7 million.

The insurer has a solid track record of beating earnings estimates in each of the last four quarters, the average being 13.39%.

The stock is trading above the 50-day and 200-day simple moving averages (SMA) of $97.82 and $95.00, respectively, indicating solid upward momentum. SMA is a widely used technical analysis tool to predict future price trends by analyzing historical price data.

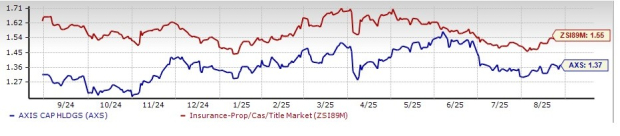

AXIS Capital’s shares are trading at a discount compared to the industry. Its forward price-to-book value of 1.37X is lower than the industry average of 1.55X, the Finance sector’s 4.26X and the Zacks S&P 500 Composite’s 8.42X. Also, it has a Value Score of B.

The Zacks Consensus Estimate for AXIS Capital’s 2025 earnings per share indicates a year-over-year increase of 6.8%. The consensus estimate for revenues is pegged at $6.44 billion, implying a year-over-year improvement of 5.6%. The consensus estimate for 2026 earnings per share and revenues indicates an increase of 4.5% and 6.9%, respectively, from the corresponding 2025 estimates.

Earnings have grown 67.1% in the past five years, better than the industry average of 20.9%.

Each of the four analysts covering the stock has raised estimates for 2025, and one analyst has raised the same for 2026 over the past 30 days. Thus, the Zacks Consensus Estimate for 2025 and 2026 earnings has moved up 3.8% and 0.08%, respectively, in the past 30 days.

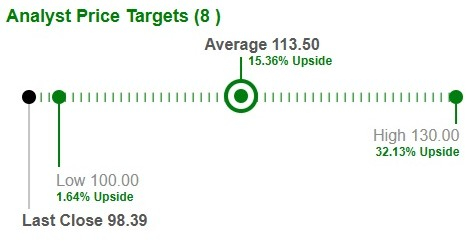

Based on short-term price targets offered by eight analysts, the Zacks average price target is $113.50 per share. The average suggests a potential 15.3% upside from the last closing price.

Return on equity in the trailing 12 months was 18.7%, better than the industry average of 7.6%. This highlights the company’s efficiency in utilizing shareholders’ funds.

AXIS Capital aims to be a leading specialty underwriter and thus focuses on growth areas, including wholesale insurance and lower middle markets. Lowering risk exposure while concentrating on accident and health, excess and supply property, casualty, credit and surety, and specialty reinsurance lines bodes well for growth.

The Insurance segment is poised to benefit from a diversified portfolio of global specialty businesses, leadership positions and growth opportunities across major business lines.

The Reinsurance business should benefit from strong cycle management, focusing on improving the business mix.

AXIS Capital stays focused on expanding digital capabilities to create new business growth in desirable and smaller accounts. Simplifying operating structure, delivering efficiencies and capitalizing on productivity gains should help it achieve a general and administrative ratio of less than 11% by 2026.

Strategic initiatives have been driving improvement in its operating earnings over the past few years.

Axis Capital's dividend track record is impressive. It hiked its dividend for 18 straight years and currently yields 1.7%, way above the industry average of 0.2%. The insurer boasts one of the highest dividend yields among its peers.

This leading specialty insurer and global reinsurer, which aims to lead in specialty risks, has been repositioning its portfolio and strengthening its book of business. Focusing on prudently deploying resources while enhancing efficiencies, improving its portfolio mix and underwriting profitability, poises Axis Capital for growth.

Higher return on capital, favorable growth estimates, as well as attractive valuations should continue to benefit Axis Capital over the long term. The stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-25 | |

| Apr-24 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-21 | |

| Apr-20 | |

| Apr-17 | |

| Apr-16 | |

| Apr-16 | |

| Apr-16 | |

| Apr-16 | |

| Apr-16 | |

| Apr-16 | |

| Apr-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite