|

|

|

|

|||||

|

|

|

The companies operating in the Zacks Oil-Energy sector present a strong long-term investment case, supported by vast shale reserves, advanced extraction methods, and resilient global energy demand. Breakthroughs such as hydraulic fracturing and horizontal drilling have unlocked substantial unconventional resources, cementing the United States’ role as a global leader in oil and natural gas production and exports.

As energy security becomes increasingly critical, U.S. exploration and production companies benefit from their strategic geopolitical position and the rapid growth of LNG export markets. A disciplined approach to capital allocation and cost efficiency has bolstered free cash flow generation, while ongoing consolidation and improved operational performance continue to enhance the industry’s ability to deliver consistent earnings and sustainable shareholder returns, even in volatile pricing environments.

Amid such a backdrop, let’s focus on Occidental Petroleum OXY and Diamondback Energy FANG as both companies derive a significant portion of their production from the Permian Basin. Both companies are leveraging technology and operational efficiencies to maximize recovery and reduce emissions, aligning their strategies with the broader industry trend toward sustainable, cash flow-driven growth.

Occidental presents an attractive investment proposition, supported by its diversified portfolio, solid free cash flow generation, and strategic emphasis on low-carbon solutions. Courtesy of OXY’s dominant position in the Permian Basin and contributions from international assets, the company delivers consistent production and reliable earnings. Its prudent capital management, ongoing debt reduction, and substantial commitments to carbon capture initiatives enhance long-term growth potential. With a broad upstream presence across global markets, Occidental is well-positioned for further expansion, making it a strong choice for investors seeking exposure to the energy sector.

Diamondback offers a compelling investment case driven by its premier position in the Permian Basin, one of the most prolific basins. The company benefits from a high-quality asset base, efficient operations, and a disciplined capital strategy that prioritizes shareholder returns through dividends and share repurchases. Diamondback’s low breakeven costs, strong balance sheet, and consistent free cash flow generation provide resilience across commodity cycles. Its focus on operational efficiency, technology adoption, and strategic acquisitions has strengthened scale and profitability. These strengths position Diamondback as a leading independent producer capable of delivering sustainable long-term value.

Both companies are leading names in the oil and gas sector. Examining their fundamental metrics more closely will help highlight how they compare and identify which stock offers the stronger investment opportunity.

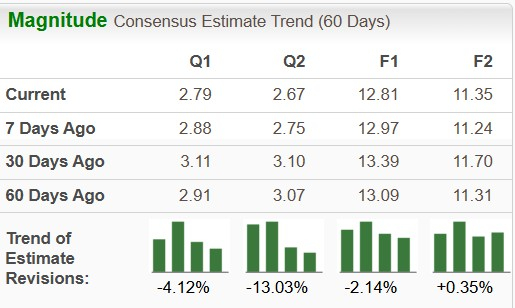

The Zacks Consensus Estimate for Diamondback’s earnings indicates a decline of 2.14% for 2025 and an increase of 0.35% for 2026 in the past 60 days.

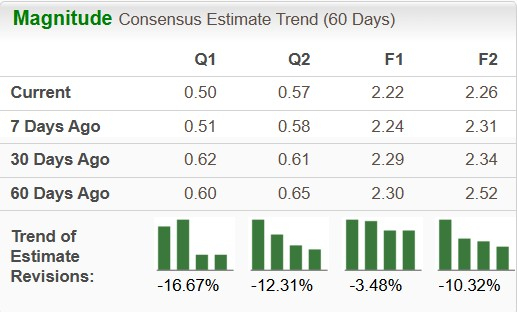

The Zacks Consensus Estimate for Occidental’s earnings indicates a decline of 3.48% for 2025 and 10.32% for 2026 in the past 60 days.

Oil and Energy companies typically maintain high debt levels because of the industry’s capital-intensive requirements. Large upfront investments are needed for exploration, infrastructure development, and major projects. Firms also rely on leverage to navigate commodity price swings, support acquisitions, and uphold shareholder returns in volatile market conditions.

Diamondback Energy’s debt to capital currently stands at 26.09% compared with Occidental Petroleum’s debt to capital of 39.22%. FANG’s debt to capital is better than the S&P 500 level of 38.33%. It indicates FANG is utilizing much less debt to run its operations.

Capital expenditure plays a vital role in the oil and gas industry, fueling exploration, development, and the upkeep of key energy assets necessary for sustained production and long-term revenue growth. Companies allocate funds to infrastructure and advanced technologies to boost operational efficiency and minimize environmental impact. The potential for further reductions in the second half of the year stands to benefit oil and gas firms by lowering borrowing costs and supporting investment.

OXY plans to invest in the range of $7.1-$7.3 billion in 2025 to further strengthen its existing operations. FANG plans to plans to invest in the range of $3.4-$3.6 billion in 2025.

ROE is an essential financial indicator that evaluates a company’s efficiency in generating profits from the equity invested by its shareholders. It demonstrates how well management is utilizing the capital provided to increase earnings and deliver value.

OXY’s current ROE is 13.78% compared with FANG’s ROE of 9.48%, both underperforming the sector’s ROE of 15.12%.

Occidental Petroleum currently appears to be cheaper compared with Diamondback Energy on trailing 12-month Enterprise Value/Earnings before Interest Tax Depreciation and Amortization (EV/EBITDA).

OXY is currently trading at 5.56X, while FANG is trading at 6.62X, compared with their sector’s 5.07X.

Dividends are regular payments made by a company to its shareholders and represent a direct way for investors to earn a return on their investment. They are an important indicator of a company’s financial health and stability, often signaling strong cash flow and consistent earnings.

Currently, the dividend yield for Diamondback is 2.72%, while the same for Occidental is 2.05%. The dividend yields of both companies are higher than the S&P 500’s yield of 1.48%.

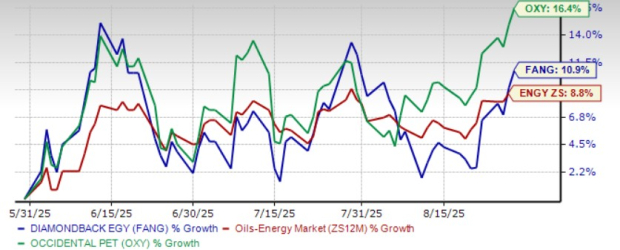

In the past three months, Occidental Petroleum’s shares have gained 16.4% compared with Diamondback Energy’s rally of 10.9% and its sector’s return of 8.8%.

Occidental and Diamondback are strategically investing in their infrastructure to expand operations and cater to the rising global demand for hydrocarbons.

Based on the above discussion, it appears OXY has a marginal edge over FANG, despite the companies currently carrying a Zacks Rank #3 (Hold) each. Diamondback is using a lower volume of debt to run its operation, but Occidental’s wider capital expenditure plan, cheaper valuation, better ROE, and stronger share price return turn the tide in its favor.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-13 | |

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite