|

|

|

|

|||||

|

|

|

Snowflake stock shot up impressively following its latest quarterly report.

The company is getting an AI-powered boost, and its earnings growth outpaced that of Nvidia in the previous quarter.

Snowflake has the ability to clock faster earnings growth than Nvidia going forward, thanks to the adoption of AI in the data cloud space.

All eyes were on Nvidia on Aug. 27 in anticipation of the semiconductor giant's latest quarterly report, but it looks like investors were not impressed with the chip designer's results.

Though Nvidia coasted past Wall Street's expectations and delivered a healthy year-over-year increase in both revenue and earnings, concerns about the company's business in China weighed on the stock. As a result, the stock remained almost flat the following day. However, there's another artificial intelligence (AI) company that released its results on the same day, and its stock soared impressively. In fact, this stock has outpaced Nvidia stock significantly in the past year.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Let's take a closer look at that name and why it has the potential to fly even higher.

Image source: Getty Images

Snowflake (NYSE: SNOW) operates a cloud-based data platform on which customers can securely store data for processing and analysis. Its data cloud platform is available on leading cloud computing platforms such as Amazon Web Services, Microsoft Azure, and Google Cloud. Moreover, Snowflake also operates a marketplace on which its customers can get access to applications and data shared by other customers.

The company has been offering AI tools to its customers so they can get more out of their data, and this strategy has been paying off nicely in recent quarters. So, it wasn't surprising to see Snowflake exceeding Wall Street's expectations when it released its fiscal 2026 second-quarter results (for the three months ended July 31).

The company's revenue shot up 32% year over year to $1.1 billion last quarter, an acceleration of three percentage points from the year-ago period. The rapidly improving adoption of Snowflake's AI solutions is playing a key role in driving this acceleration. The company's customer base was up by 19% year over year in the previous quarter, and just over half of its customer accounts were using Snowflake AI solutions.

The company's AI platform helps customers build AI agents for analyzing documents, develop and deploy AI models and applications, and access popular large language models (LLMs) that they can apply to their data. Snowflake management made it clear on the latest earnings conference call that AI is indeed the reason why its customer base is swelling. In the words of CEO Sridhar Ramaswamy, "Today, AI is a core reason why customers are choosing Snowflake, influencing nearly 50% of new logos won in Q2. And once they're on our platform, AI becomes a cornerstone of their strategy, powering 25% of all deployed use cases with over 6,100 accounts using Snowflake's AI every week."

Even better, AI is helping Snowflake drive stronger spending from its existing customer base. This is evident from the company's net revenue retention rate of 125% last quarter, a metric that compares the spending by its customers in a period to the spending by the same customer cohort in the previous year. A reading of more than 100% means that its existing customers have expanded their usage of Snowflake's solutions or are buying more of its offerings.

The growth in Snowflake's customer base and the expansion in spending by existing customers led to an impressive year-over-year growth of six percentage points in its non-GAAP (adjusted) operating margin. As a result, Snowflake's adjusted earnings almost doubled from the year-ago period to $0.35 per share. What's more, the company's solid revenue pipeline and huge addressable market indicate that it can continue to deliver more upside.

Shares of Snowflake have jumped 108% in the past year, well ahead of the 40% gains clocked by Nvidia during the same period. Looking ahead, Snowflake has room for further growth considering that its remaining performance obligations (RPO) jumped by 33% in the previous quarter to $6.9 billion. Not surprisingly, the company has now raised its fiscal 2026 product revenue forecast to $4.4 billion from the earlier estimate of $4.33 billion.

Snowflake could further raise its forecast as the year progresses since it is sitting on a sizable revenue opportunity, which could jump higher in the future thanks to the proliferation of AI. The company expects its total addressable market (TAM) to more than double in the next five years to $355 billion in 2029, suggesting that the company is on track to enjoy years of terrific growth.

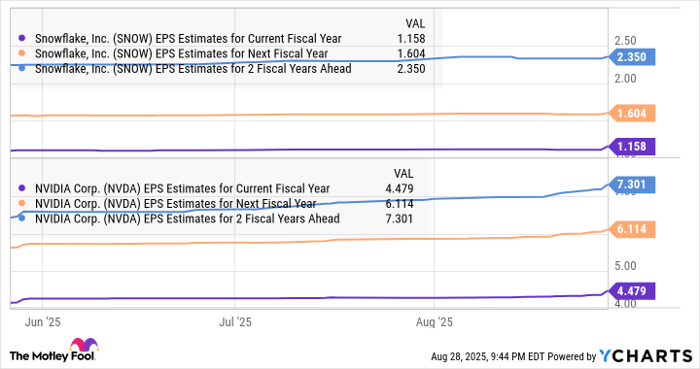

Another thing worth noting is that Snowflake's earnings increased at a faster pace than the 54% year-over-year growth reported by Nvidia last quarter. Analysts are expecting it to keep outpacing Nvidia's earnings growth in the future as well.

SNOW EPS Estimates for Current Fiscal Year data by YCharts

So, don't be surprised to see Snowflake stock deliver more gains to investors in the long run. And with the stock trading at 19 times sales as compared to Nvidia's price-to-sales ratio of 30, growth investors can still consider buying Snowflake even after the healthy gains it has clocked in the past year.

Before you buy stock in Snowflake, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Snowflake wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $651,599!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,067,639!*

Now, it’s worth noting Stock Advisor’s total average return is 1,049% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Microsoft, Nvidia, and Snowflake. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 26 min |

Snowflake Earnings, Revenue Edge By Estimates As Guidance Underwhelms

SNOW +5.06%

Investor's Business Daily

|

| 29 min | |

| 35 min | |

| 58 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours |

AI Stocks At Crossroads As Nvidia, Snowflake, CoreWeave, Salesforce Step Into Spotlight

SNOW +5.06%

Investor's Business Daily

|

| 8 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite