|

|

|

|

|||||

|

|

|

Opendoor Technologies OPEN reported cautiously encouraging second-quarter 2025 results, with revenues of $1.57 billion, up 3.7% year over year. During the quarter, the firm posted its first positive adjusted EBITDA in three years at $23 million, reversing from a $5 million loss in the prior-year period. While the contribution margin slipped to 4.4% from 6.3% a year earlier, management highlighted the second-quarter performance as evidence of operating leverage and disciplined underwriting.

Looking ahead to the third quarter, Opendoor expects a sharp sequential drop, guiding revenues to between $800 million and $875 million, while forecasting an adjusted EBITDA loss between $21 million and $28 million. Elevated mortgage rates and suppressed buyer demand are likely to have weighed on transaction volumes, while an unfavorable mix of older inventory is expected to pressure contribution margins in the second half of the year.

Meanwhile, Opendoor is pushing forward with what management described as the company’s most important strategic pivot yet — evolving from a single cash-offer product to a distributed, agent-driven platform. Early pilot results indicate 2x higher customer conversion to cash offers and 5x higher listing conversion rates compared with the legacy direct-to-consumer model. The rollout of Cash Plus — a hybrid offer blending upfront liquidity with resale upside — is expanding across markets and provides a more capital-light, risk-adjusted path to growth.

For investors, the near-term outlook remains cloudy, but the company’s strategic reorientation bodes well for long-term resilience. With proprietary transaction data, strong Net Promoter Scores and rising agent engagement, Opendoor is laying the groundwork for higher-margin, capital-light revenue streams. Even as the company’s upcoming quarter performance likely indicates pressure on top-line momentum, the move toward platform-enabled scale could support profitability as housing market conditions stabilize.

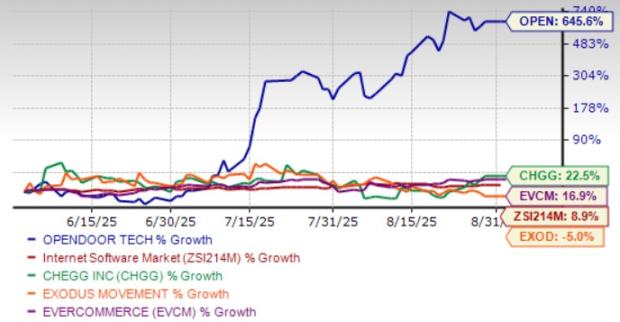

Shares of Opendoor have skyrocketed 645.6% in the past three months compared with the industry’s growth of 8.9%. In the same time frame, other industry players like Chegg, Inc. CHGG and EverCommerce Inc. EVCM have gained 22.5% and 16.9%, respectively, while shares of Exodus Movement, Inc. EXOD have declined 5% in the same time frame.

OPEN Three-Month Price Performance

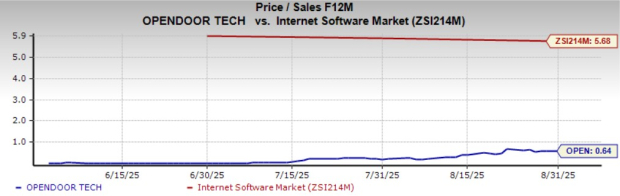

From a valuation standpoint, OPEN trades at a forward price-to-sales (P/S) multiple of 0.64X, significantly below the industry’s average of 5.68X. Conversely, industry players, such as Chegg, Exodus and EverCommerce, have P/S multiples of 0.42X, 5.81X and 3.41X, respectively.

The Zacks Consensus Estimate for OPEN’s 2025 loss per share has widened from 21 cents to 24 cents in the past 30 days. This reflects weakening analyst sentiment and diminished confidence in the stock’s near-term outlook.

The company is likely to report strong earnings, with projections indicating a 35.1% rise in 2025. Conversely, industry players like Chegg and Exodus are likely to witness a fall of 114.7% and 52.2%, respectively, year over year in 2025 earnings. Meanwhile, EverCommerce’s earnings in 2025 are expected to surge 131.8% year over year.

OPEN stock currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-10 | |

| Jul-09 | |

| Jul-07 | |

| Jun-17 | |

| Jun-15 | |

| Jun-15 | |

| Jun-12 | |

| Jun-12 | |

| Jun-12 | |

| Jun-11 | |

| Jun-10 | |

| Jun-03 | |

| Jun-03 | |

| Jun-02 | |

| May-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite