|

|

|

|

|||||

|

|

|

Douglas Dynamics’s 30.4% return over the past six months has outpaced the S&P 500 by 20.7%, and its stock price has climbed to $34 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Douglas Dynamics, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We’re glad investors have benefited from the price increase, but we don't have much confidence in Douglas Dynamics. Here are three reasons you should be careful with PLOW and a stock we'd rather own.

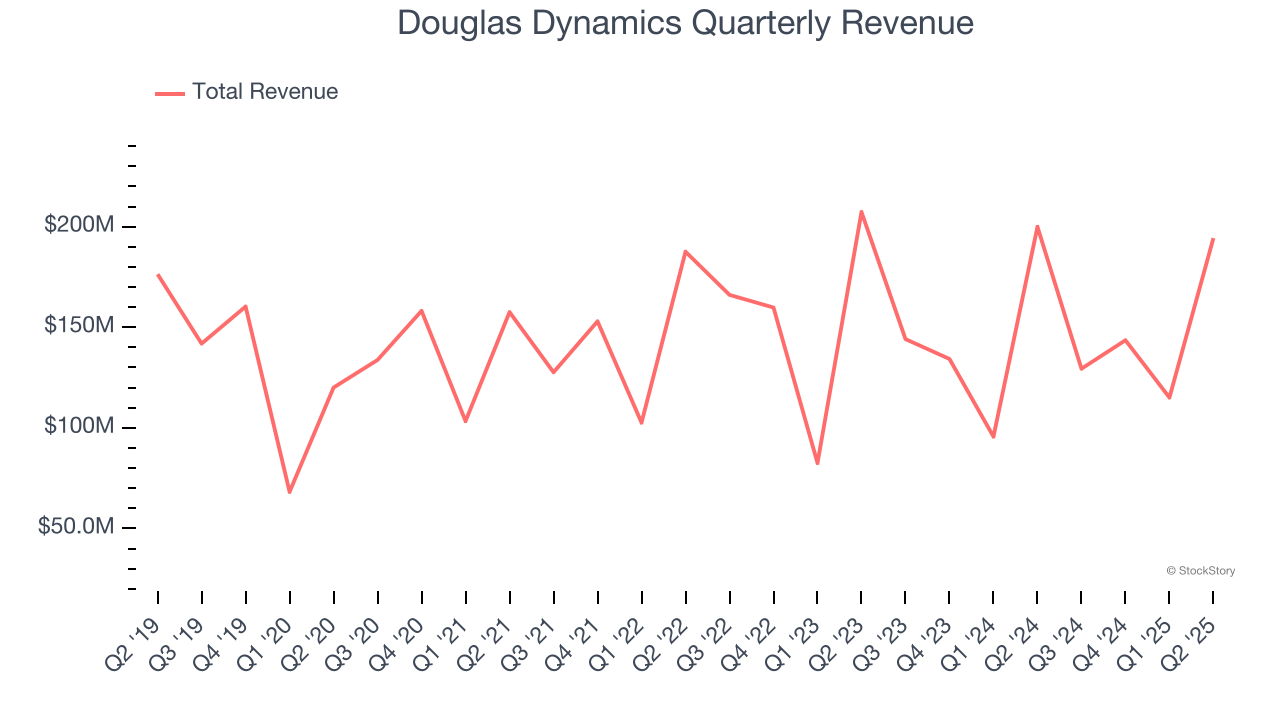

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Douglas Dynamics’s 3.5% annualized revenue growth over the last five years was sluggish. This was below our standard for the industrials sector.

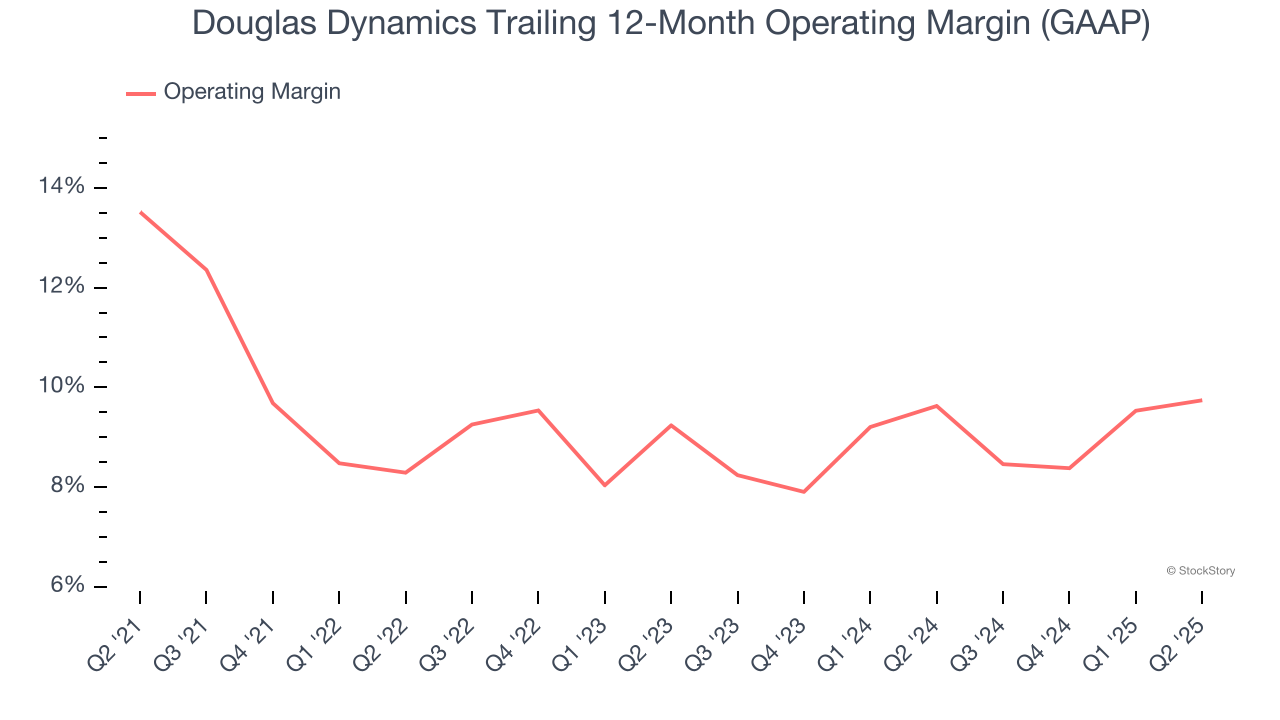

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Looking at the trend in its profitability, Douglas Dynamics’s operating margin decreased by 3.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 9.7%.

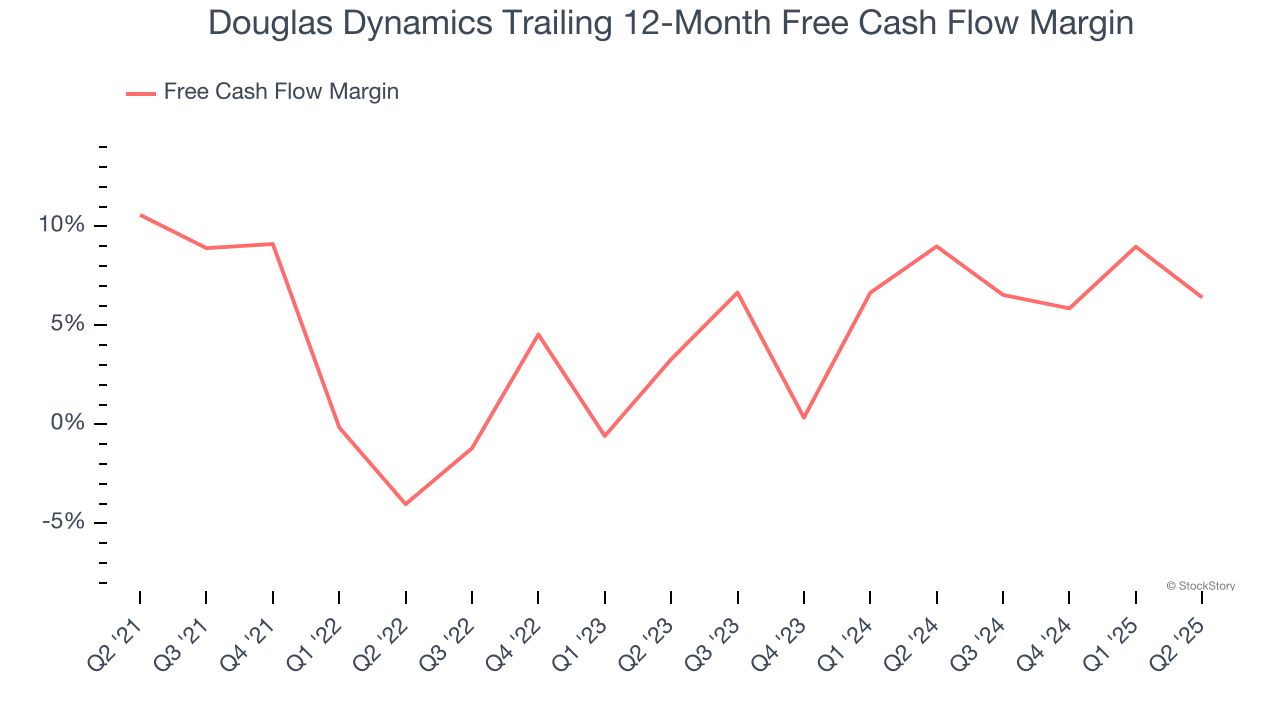

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Douglas Dynamics’s margin dropped by 4.2 percentage points over the last five years. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s in the middle of an investment cycle. Douglas Dynamics’s free cash flow margin for the trailing 12 months was 6.4%.

We cheer for all companies making their customers lives easier, but in the case of Douglas Dynamics, we’ll be cheering from the sidelines. With its shares outperforming the market lately, the stock trades at 15.4× forward P/E (or $34 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Jul-21 | |

| Jun-05 | |

| May-05 | |

| May-04 | |

| May-04 | |

| Apr-21 | |

| Mar-02 | |

| Feb-27 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite