|

|

|

|

|||||

|

|

|

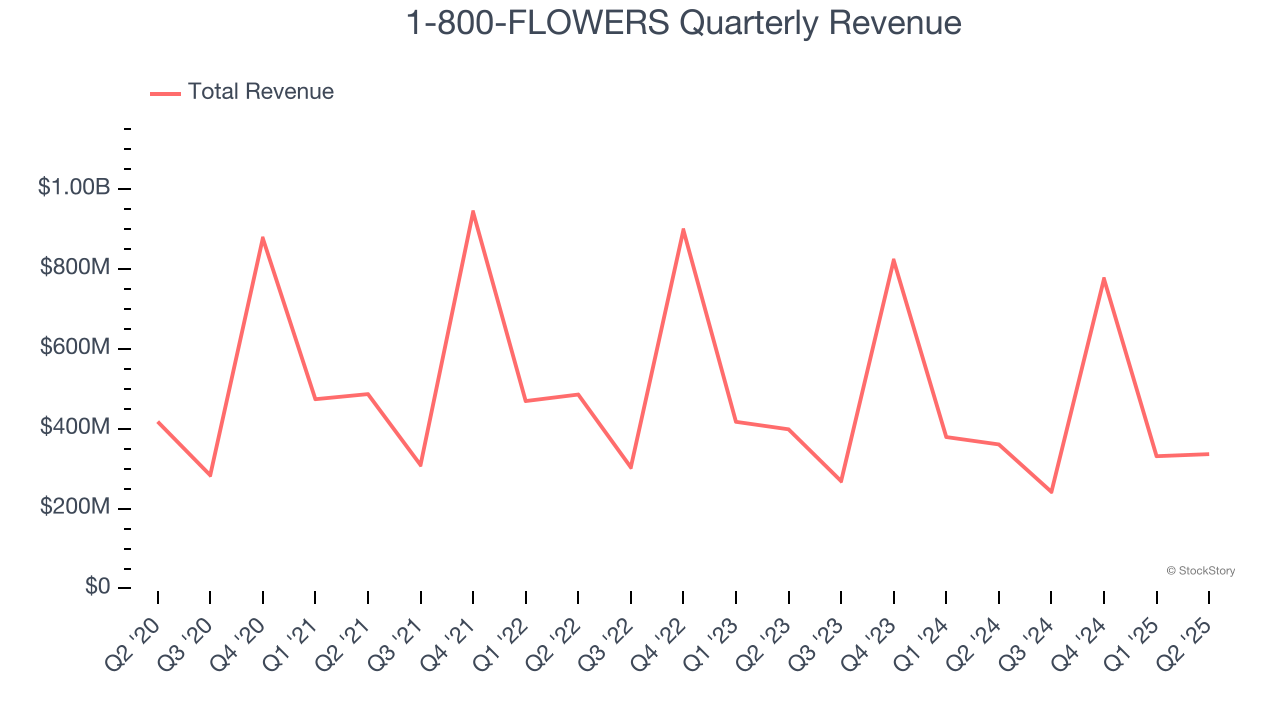

E-commerce florist and gift retailer 1-800-FLOWERS (NASDAQ:FLWS) reported Q2 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 6.7% year on year to $336.6 million. Its non-GAAP loss of $0.69 per share was 34.4% below analysts’ consensus estimates.

Is now the time to buy 1-800-FLOWERS? Find out by accessing our full research report, it’s free.

“I’m excited to have joined 1-800-FLOWERS.COM, Inc. at such a pivotal moment. This is an iconic brand with products people love, but we haven’t fully lived up to our potential in recent years. Customer expectations are shifting, technology is moving fast, and competition is evolving. That creates real opportunity. We’re making the company leaner and more agile, putting the customer at the center of everything we do, and using data to make smarter decisions. We’re sharpening how we attract and retain customers, broadening our reach beyond our e-commerce sites, and modernizing the customer experience. At the same time, we’re driving operational discipline, efficiency, and accountability. These changes will position us to get back to growth, deliver a better experience for our customers, and create long-term value for shareholders,” said Adolfo Villagomez, Chief Executive Officer.

Founded in 1976, 1-800-FLOWERS (NASDAQ:FLWS) is an online retailer of flowers, gifts, and gourmet foods, serving customers globally.

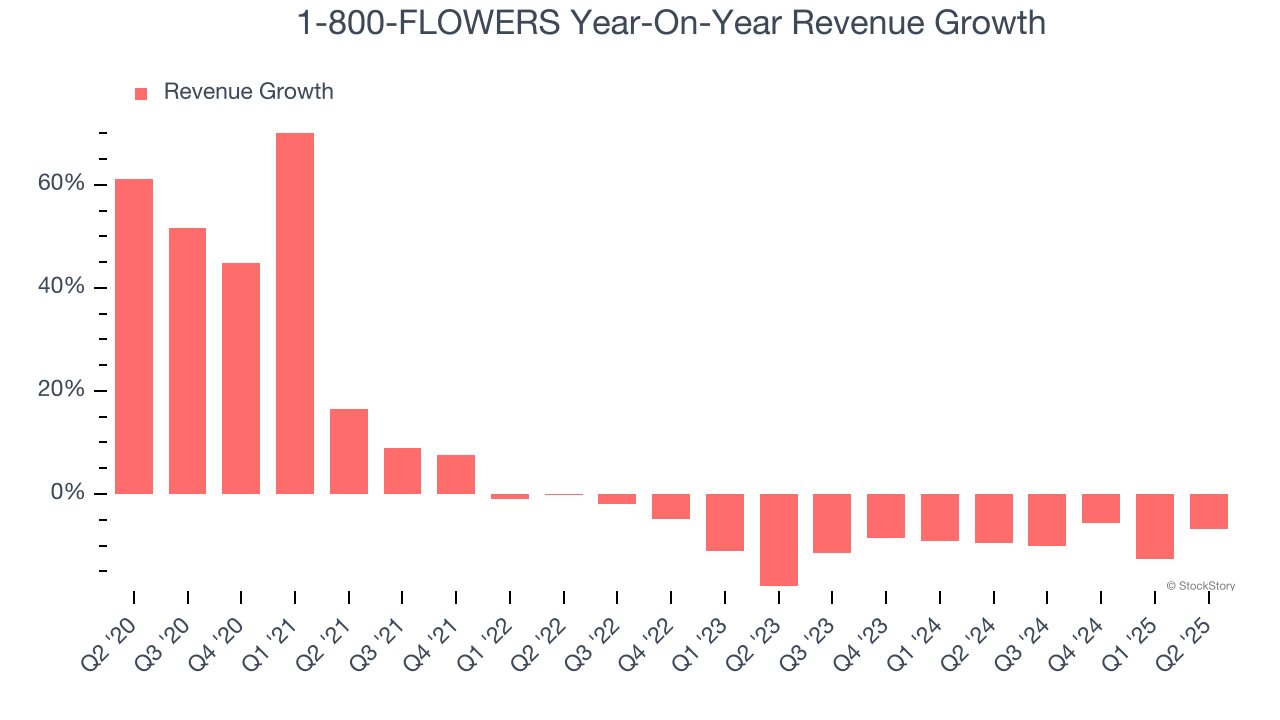

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, 1-800-FLOWERS grew its sales at a weak 2.5% compounded annual growth rate. This fell short of our benchmarks and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. 1-800-FLOWERS’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 8.6% annually.

This quarter, 1-800-FLOWERS’s revenue fell by 6.7% year on year to $336.6 million but beat Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

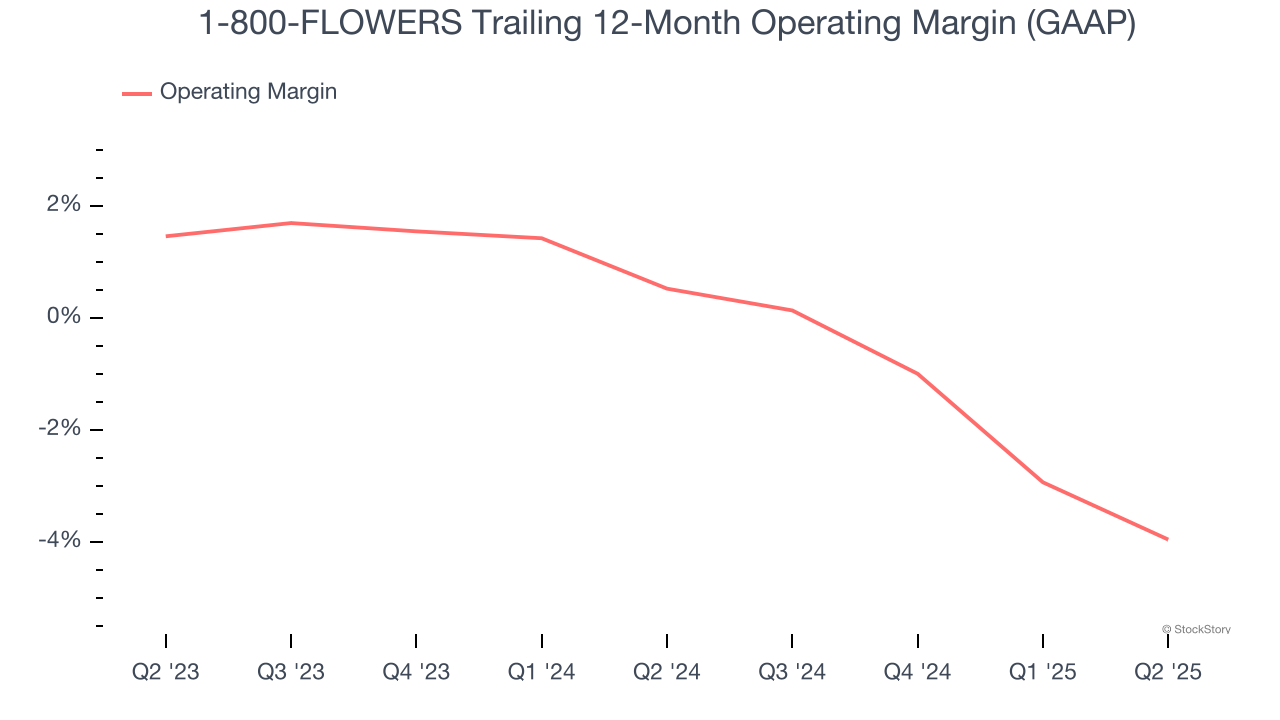

1-800-FLOWERS’s operating margin has been trending down over the last 12 months and averaged negative 1.6% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

This quarter, 1-800-FLOWERS generated a negative 16.5% operating margin. The company's consistent lack of profits raise a flag.

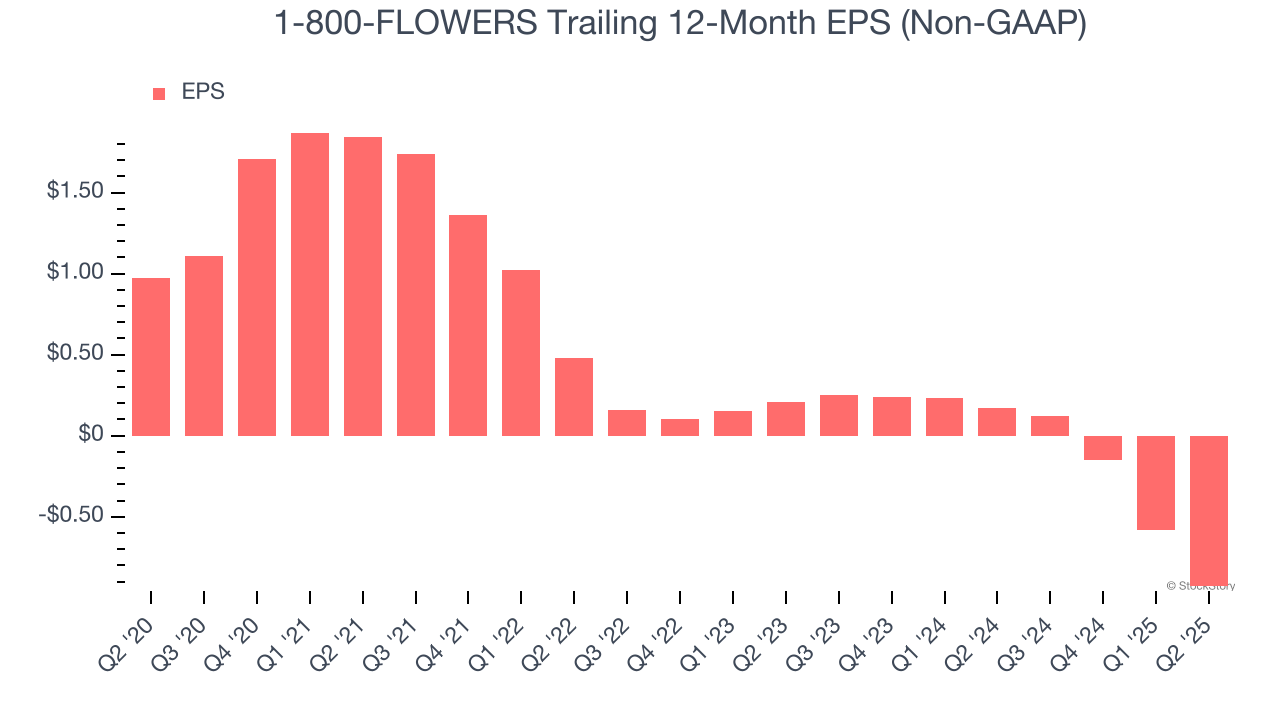

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for 1-800-FLOWERS, its EPS declined by 24.2% annually over the last five years while its revenue grew by 2.5%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q2, 1-800-FLOWERS reported adjusted EPS of negative $0.69, down from negative $0.34 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects 1-800-FLOWERS to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.93 will advance to negative $0.55.

It was encouraging to see 1-800-FLOWERS beat analysts’ revenue expectations this quarter. On the other hand, its EPS missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $5.33 immediately after reporting.

1-800-FLOWERS’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| May-08 | |

| May-07 | |

| May-06 | |

| Apr-23 | |

| Apr-15 | |

| Mar-10 | |

| Feb-27 | |

| Feb-26 | |

| Feb-13 | |

| Feb-09 | |

| Feb-05 | |

| Jan-30 | |

| Jan-29 | |

| Jan-29 | |

| Jan-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite