|

|

|

|

|||||

|

|

|

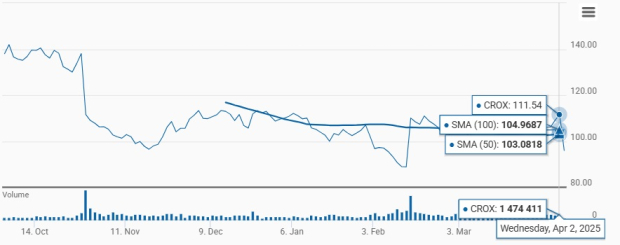

Crocs, Inc. CROX has demonstrated strong upward momentum, trading above its 50- and 100-day simple moving averages (SMAs). SMA is a key indicator of price stability and long-term bullish trends.

CROX ended yesterday’s trading session at $111.54, above its 50- and 100-day SMAs of $103.08 and $104.97, respectively, highlighting a continued uptrend. This technical strength, combined with consistent momentum, reflects positive market sentiment and investor confidence in the company’s financial stability and growth potential.

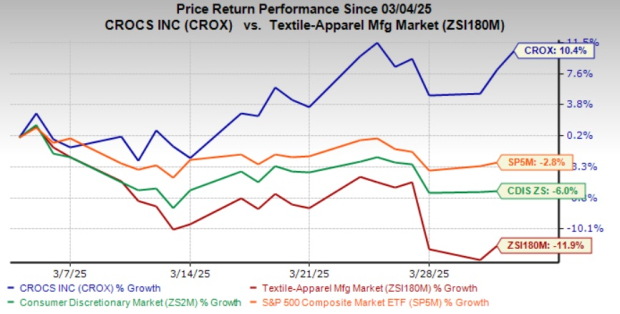

CROX’s shares have seen an impressive 10.4% increase against the industry’s decline of 11.9% in the past month. The company’s enhanced operational efficiency and growth initiatives have also helped it outperform the broader Consumer Discretionary sector and the S&P 500 index’s decline of 6% and 2.8%, respectively, in the same period.

Crocs is gaining from strong consumer demand for its core brand, effective pricing strategies and lower fulfillment costs. The company continues to benefit from solid consumer demand across its brand portfolio, supported by higher volumes, which have led to consistent growth over time. Key contributors to this success include its iconic clogs and sandals, with the Classic Clog leading fourth-quarter 2024 performance.

The company's HEYDUDE brand is undergoing a transformation as it works to address challenges and build a profitable growth trajectory. Crocs has adopted a multi-faceted strategy to enhance HEYDUDE's long-term perception and strength. This includes reducing excess stock across channels, closing more than 50% of its retail accounts to focus on a more premium presence and raising the average selling price to better reflect the brand’s value and improved margins.

HEYDUDE is focusing on three main goals: connecting with young women to build a strong community, improving popular products like Wally and Wendy, and strengthening its business in North America. The brand has made progress with efforts like partnering with actress Sydney Sweeney as a global ambassador, which has brought in record-breaking engagement. The launch of TikTok Shop has also helped HEYDUDE attract younger customers, even making it the top global account on some launch days. Such efforts are likely to bolster the brand’s growth.

Crocs is on track with its long-term strategy and key initiatives to deliver sustainable growth, as announced in September 2021. Its growth strategy is focused on three key initiatives. First, igniting icons across both brands to enhance awareness and relevance for customers. Second, investing strategically in Tier 1 markets to boost market share gains via talent, marketing, digital and retail. And third, diversifying the product range to attract more consumers.

The company’s long-term targets under the plan included generating revenues of more than $5 billion, representing a five-year compounded annual growth rate of more than 17% by 2026. Management expects four times the revenue growth in sandals by 2026. The company sees long-term opportunities in Asia, primarily in China.

Despite positive momentum, Crocs faces potential headwinds from upcoming tariff increases, which are expected to impact its financial performance in 2025. In 2025, approximately 15% of enterprise imports are projected to come from China, with Crocs at 10% and HEYDUDE at 27%. Exposure to Mexico remains low at under 4%, solely for the Crocs brand. These tariffs are expected to reduce gross profit by about $11 million, lowering gross margins by around 25 basis points.

For the first quarter of 2025, Crocs expects a 3.5% year-over-year revenue decline, with foreign currency impacting revenues by approximately $19 million. At constant currency, enterprise revenues are projected to fall by about 1.5%. The Crocs brand is expected to show a slight decline of 1% to flat year over year, with growth in international markets offsetting losses. In contrast, HEYDUDE's revenues are expected to drop 14-16%, mainly due to a reduction in wholesale.

Management anticipates a mid-single-digit decline in North American business, impacted by the Easter shift, and projects adjusted earnings per share to be between $2.38 and $2.52, with an adjusted operating margin of 21.5%, factoring in the adverse effects of tariffs and foreign currency.

Crocs continues to demonstrate strong brand momentum, benefiting from solid consumer demand, effective pricing strategies and lower fulfillment costs. The company is well-positioned for long-term growth through its strategic initiatives, particularly with its core brand and the ongoing transformation of HEYDUDE.

However, the tariff increases and foreign currency impacts pose potential headwinds, with declines expected in revenues and margins in the near term. The projected revenue decline for the first quarter of 2025, coupled with macroeconomic uncertainties, warrants a cautious stance. CROX currently carries a Zacks Rank #3 (Hold).

We have highlighted three top-ranked stocks, namely, V.F. Corporation VFC, Gildan Activewear GIL and G-III Apparel Group, Ltd. GIII.

V.F. Corp engages in the design, procurement, marketing and distribution of branded lifestyle apparel, footwear and accessories for men, women and children in the Americas, Europe and the Asia-Pacific. It carries a Zacks Rank #2 (Buy) at present. VFC delivered an earnings surprise of 82.4% in the last reported quarter. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The consensus estimate for V.F. Corp’s current-quarter EPS indicates growth of 53.1% from the year-ago levels.

Gildan Activewear, a manufacturer of premium-quality branded basic activewear, carries a Zacks Rank of 2 at present. GIL has a trailing four-quarter earnings surprise of 5.3%, on average.

The consensus estimate for Gildan Activewear’s current financial-year EPS indicates growth of 16% from the year-ago figure.

G-III Apparel is a manufacturer, designer and distributor of apparel and accessories under licensed brands, owned brands and private label brands. It carries a Zacks Rank #2 at present.

The Zacks Consensus Estimate for GIII’s fiscal 2025 earnings and revenues implies declines of 4.5% and 1.2%, respectively, from the year-ago actuals. GIII delivered a trailing four-quarter average earnings surprise of 117.8%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 12 hours | |

| 15 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite