|

|

|

|

|||||

|

|

|

It appears Figma's growth rate is going to decelerate in each quarter of 2025, which isn't what investors want to see.

IPO stocks can be volatile in their early months of trading and Figma stock was particularly volatile for one simple reason.

At the end of July, design software company Figma (NYSE: FIG) went public in one of the most celebrated initial public offerings (IPOs) in years. But the stock plunged about 20% on Sept. 4 after its first quarterly financial report as a publicly traded company.

Investors are rushing for the exits for one reason: a sharp deceleration in Figma's growth rate.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

For the second quarter of 2025, Figma reported revenue of $250 million, which was a 41% year-over-year increase. To be sure, that's one of the better growth rates among publicly traded companies.

Figma also reported Q2 net income of $28 million. There is seemingly no end to cash-burning software companies on the stock market. Therefore, seeing a company with real profits is refreshing.

However, Figma stock is down nevertheless because of the brisk slowdown in growth. It's clearly not something that investors had expected.

Figma's software allows its customers to design websites and apps. And it's used by many top-tier companies, including Netflix and Duolingo. But there's fear that improvements in generative artificial intelligence (AI) could take business away from Figma. After all, why pay for Figma's services when generative AI could potentially do it cheaper?

Figma's growth, however, appeared resilient to any potential competitive threats from generative AI or elsewhere. In 2024, its revenue jumped by 48% compared to 2023. And in the first quarter of 2025, it was up 46%. Those are really strong numbers.

Figma's Q2 growth of 41% is strong as well. But it represents a more troubling drop-off in the growth rate. And if that wasn't enough, management guided for third-quarter revenue of about $265 million, which is only 33% growth.

In short, Figma's growth is sliding fast, going from a 46% rate in Q1 to a projected 33% rate in the upcoming Q3. And reading between the lines of its full-year guidance, management expects fourth-quarter revenue to drop down to just 30% growth.

It's not clear why Figma's growth rate is dropping so fast. It could be competitive pressures, but it might not be. But since investors are already nervous, it didn't take much of a nudge to send them running for the exits after the Q2 report.

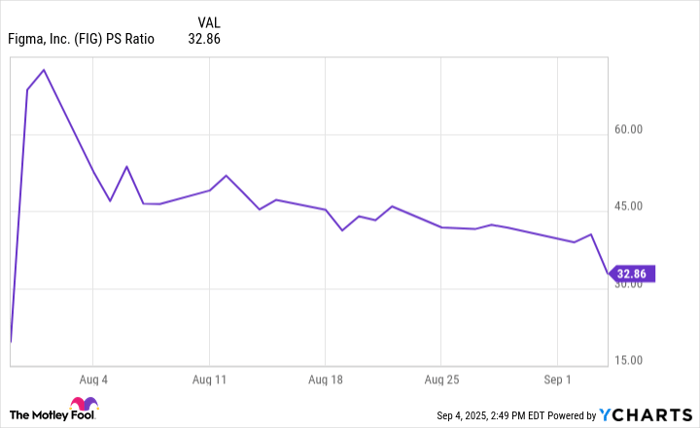

At the time of this writing, Figma stock is now down more than 50% from the high it reached last month. And yet the stock still trades at a valuation of more than 30 times sales, as the chart below shows.

FIG PS Ratio data by YCharts

Even if investors value Figma based on its expectations for 2025, it's still trading at around 27 times sales. Software stocks often have valuations between 10 and 20 times sales, if growth and margins are good enough. But 27 times sales is lofty. And Figma's growth is slowing, leaving investors to wonder how long the deceleration will continue, calling its valuation into question.

Some might wonder why Figma's valuation reached such heights in the first place. There's actually a fairly simple explanation: There were over 487 million outstanding shares of Figma after its IPO. But the company and selling stockholders only offered about 37 million, or about 8%.

After a couple of years of a dry IPO market, investors were hungry to get their hands on shares of Figma. But there were relatively few available. This imbalance sent shares skyrocketing. Investors should remember that the IPO's original price was $33 per share. Even after the 50% pullback, it's still up more than 60% from where it started.

This is why many seasoned investors choose to wait to buy IPO stocks, no matter how attractive they are. IPO stocks can be volatile in the early months of trading.

Hopefully those who bought shares of Figma are long-term investors and have a long-term investment thesis -- an explanation of how it will create value in coming years. Even the best companies have periods of slowing growth. And stocks can routinely pull back significantly before climbing to new highs.

Figma's management has gone on record saying that it will create shareholder value by taking "big swings." This could be in the form of an acquisition, investment in cryptocurrency, or something else. Anyone who invested in Figma stock hopefully took this into account. And given that it's only been public for a month, there hasn't been enough time to let management take those swings. Patience, therefore, is necessary.

Personally, I wouldn't want to invest in a company on the basis of some unknown swing in the future -- I'd rather invest in a growing market opportunity and the ongoing upside of the business. And I'd want to invest at a reasonable price. Figma didn't check those boxes for me.

Investors might not have liked Figma's Q2 report and guidance for the rest of 2025. But while there are concerns, it's premature for shareholders to already give up on this company.

Before you buy stock in Figma, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Figma wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $661,268!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,045,818!*

Now, it’s worth noting Stock Advisor’s total average return is 1,047% — a market-crushing outperformance compared to 184% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Netflix. The Motley Fool recommends Duolingo. The Motley Fool has a disclosure policy.

| Jul-16 | |

| Jul-15 | |

| Jul-10 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jun-27 | |

| Jun-26 | |

| Jun-25 | |

| Jun-25 | |

| Jun-24 | |

| Jun-22 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite