|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

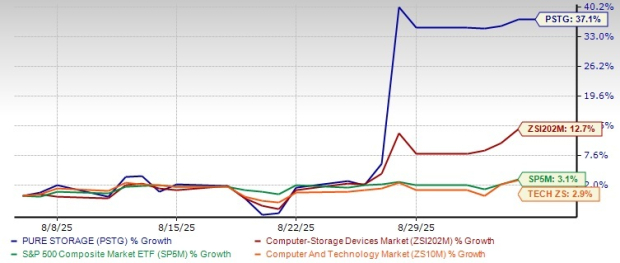

Pure Storage, Inc’s PSTG shares have been performing well on the trading front, with a gain of 37.1% in the past month. Since announcing strong quarterly numbers on Aug. 27, the stock has gained 29.4%.

The stock has outperformed its Computer-Storage Devices industry, the Zacks Computer and Technology sector and the S&P 500 composite’s growth of 12.7%, 2.9% and 3.1%, respectively.

Closing at $78.73, the stock is near its 52-week high level of $80.68, reached on Aug. 28, 2025. Does this signal time to exit or stay invested?

Let us dive into PSTG’s prospects and determine the best course of action for your portfolio.

PSTG is witnessing strong demand from large enterprises, ongoing momentum in FlashBlade, particularly FlashBlade//E, and accelerating adoption of its core software and services offerings, including Evergreen//One, Cloud Block Store and Portworx.

Accelerating recurring revenues & subscriptions is another catalyst. In the last reported quarter, Subscription services revenues (48.2%) of $414.7 million rose 14.8%. Subscription annual recurring revenues ("ARR") amounted to nearly $1.8 billion, up 18% on a year-over-year basis.

During the fiscal second quarter, PSTG expanded its Flash portfolio with a suite of next-gen storage systems, designed for performance, scale and versatility. These are FlashArray//XL R5, FlashArray//ST and FlashBlade//EXA designed to address high-performance and scalable workloads. By broadening its product portfolio, Pure Storage is strengthening its foothold across industries, ranging from financial services and healthcare to AI-driven startups and large-scale cloud providers.

A key highlight of the fiscal second quarter was the introduction of the Enterprise Data Cloud (“EDC”), a new architectural paradigm for data and storage management. Enhanced with Fusion v2, Purity enables customers to build their own EDC, automating storage and delivering software-defined data management.

Pure Storage’s strategic tie-up with Meta Platforms has moved to first volume deployment, with revenues being recognized in the fiscal second quarter. PSTG also highlighted that other hyperscalers are also evaluating DirectFlash to replace HDD/SSD, given significant gains in performance and cooling efficiency. Management reiterated that it remains confident of deploying 1-2 exabytes of DirectFlash technology by fiscal 2026 and “possibly more.”

Pure Storage has a strong balance sheet and an ample liquidity position. It exited the fiscal second quarter, which ended on Aug. 3, with cash and cash equivalents and marketable securities of $1.5 billion. Cash flow from operations amounted to $212.2 million and free cash flow was $150.1 million in the fiscal second quarter.

In the fiscal second quarter, the company returned $42 million to its shareholders by repurchasing 0.8 million shares. Pure Storage has $109 million left under its current authorization plan.

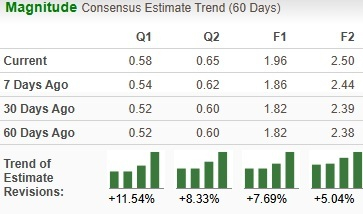

For fiscal 2026, it now expects revenues in the range of $3.6 billion to $3.63 billion, indicating 14% year-over-year growth at the midpoint. This is 300 basis points higher than the earlier guided 11% growth to $3.515 billion.

Following the outlook revision, analysts seem bullish about the stock, as implied by the upward revision in earnings estimates.

Despite a strong quarterly performance, Pure Storage is not immune to economic pressures. On the last earnings call, management explicitly acknowledged that “global macro environment remains as variable and as uncertain as ever.” If macro uncertainty intensifies, enterprises may delay cloud migrations, containerization, or AI-related storage projects, creating downside to PSTG’s revenue growth.

Pure Storage faces intensifying competition in the flash-based storage market from both new and incumbent players who are also vying aggressively for cloud and AI storage opportunities.

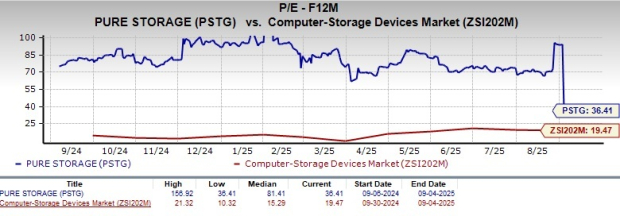

PSTG stock is trading at a premium with a forward 12-month Price/Earnings of 36.41X compared with the industry’s 19.47X.

PSTG witnessed a strong second quarter, backed by strong subscription momentum, enterprise adoption and AI-driven product expansion. Its balance sheet strength, strategic Meta partnership and raised fiscal 2026 guidance reinforce long-term growth prospects.

However, the stock’s premium valuation, competitive pressures and macro uncertainties could limit near-term upside.

PSTG carries a Zacks Rank #3 (Hold) at present. We believe new investors should wait for a better entry point and existing investors should retain PSTG stock.

Some better-ranked stocks from the broader technology space are Western Digital Corporation WDC, Netlist NLST and Hewlett Packard HPE. While WDC sports a Zacks Rank #1 (Strong Buy), NLST and HPE carry a Zacks Rank #2 (Buy) each at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for WDC’s fiscal 2026 EPS is pegged at $6.50, unchanged in the past seven days. WDC’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 6.77%. Its shares have increased 49% in the past year.

The Zacks Consensus Estimate for NLST’s 2025 earnings is pegged at a loss of 7 cents per share, unchanged in the past seven days. NLST’s earnings beat the Zacks Consensus Estimate in one of the trailing four quarters, while missing twice and matching in the remaining quarter, with the average surprise being negative 24.17%. The share price has declined 32% in the past year.

The Zacks Consensus Estimate for HPE’s fiscal 2025 EPS is pegged at $1.92. HPE’s earnings beat the Zacks Consensus Estimate in three of the trailing four quarters, while missing once, with the average surprise being 4.39%. Its shares have surged 32.2% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 13 hours | |

| 13 hours | |

| 13 hours | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite