|

|

|

|

|||||

|

|

|

Caleres, Inc. (CAL) reported second-quarter fiscal 2025 results, with the top line beating the Zacks Consensus Estimate while the bottom line missing the same. Both metrics showed a year-over-year decline.

Despite market headwinds, the company delivered a resilient performance, with sequentially improving sales trends, market share gains in women’s fashion footwear and shoe chains, and strength in Lead Brands, direct-to-consumer channels, international and Famous Footwear. Management completed $15 million in structural cost savings initiatives and finalized the acquisition of Stuart Weitzman, enhancing its premium, direct-to-consumer and international focus.

The company posted adjusted earnings of 35 cents per share, which missed the Zacks Consensus Estimate of 51 cents. Also, the bottom line decreased from 85 cents reported in the same quarter a year ago.

Caleres, Inc. price-consensus-eps-surprise-chart | Caleres, Inc. Quote

Consolidated net sales of $658.5 million dipped 3.6% year over year, due to soft sales in both segments of business. However, the metric beat the consensus mark of $651 million.

Gross profit fell 8.1% year over year to $285.8 million with the gross margin contracting 210 basis points (bps) to 43.4%. This decline was due to tariff-related expenses, selective promotions and increased provisions for inventory markdowns, partially offset by growth in higher-margin direct-to-consumer channels within the Brand Portfolio.

SG&A expenses increased 0.5% year over year to $269.7 million in the quarter. As a percentage of net sales, the figure increased 170 bps year over year to 41%, due to deleverage from reduced sales.

Caleres reported an adjusted EBITDA of $32.1 million, down 44% from the prior-year quarter. The adjusted EBITDA margin decreased 350 bps to 4.9%.

Famous Footwear segment’s net sales declined 4.9% to $399.6 million, which beat the consensus estimate of $395 million. The comparable sales of the segment were down 3.4%. The brand gained market share in shoe chains and the kids’ category during the quarter. Consistent with recent trends, the Famous consumer showed strong engagement during peak shopping periods.

Gross profit, as a percentage of Famous Footwear revenues, decreased 130 bps year over year to 43.7%. This decline was due to increased promotional days, deeper promotional offers and an unfavorable channel mix. This year, the company leaned more heavily on BOGO promotion compared with last year’s Buy More, Save More program and also offered more BOGO clearance during the quarter.

Brand Portfolio’s sales decreased 3.5% to $275.6 million, which surpassed the consensus estimate of $271 million. Moreover, comparable sales for the segment were up 3.9%. The Brand Portfolio gained market share in women’s fashion footwear during the quarter.

Gross profit, as a percentage of Brand Portfolio revenues, decreased 240 bps to 40.3%, due to higher tariff-related costs and increased markdown reserves on excess spring product, partially offset by a favorable channel mix and other factors.

Direct-to-consumer sales accounted for roughly 75% of the overall quarterly sales.

Caleres concluded the quarter with $191.5 million in cash and cash equivalents and $387.5 million in borrowings under its revolving credit agreement. Total shareholders’ equity was $621.9 million, including non-controlling interests of $8.6 million. Cash generated from operating activities was $41.6 million during the 26 weeks ended Aug. 2, 2025.

Amid ongoing uncertainty, the company will continue to withhold annual guidance. Gross margin pressure in Brand Portfolio from tariffs is expected to persist through year-end. For the third quarter, Brand Portfolio gross margin (excluding Stuart Weitzman) is estimated to decline at a pace similar to the second quarter, with improvement anticipated in the fourth quarter as mitigation efforts gain traction.

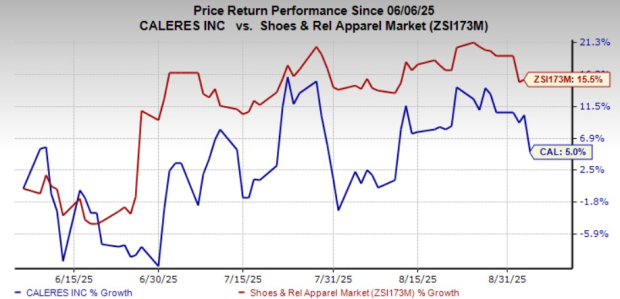

This Zacks Rank #5 (Strong Sell) stock has gained 5% in the past three months compared with the industry’s growth of 15.5%.

Levi Strauss & Co. (LEVI) designs, markets and sells apparel and related accessories for men, women and children in the United States and internationally. It flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Levi’s current fiscal-year earnings indicates growth of 4% from the year-ago actual. LEVI delivered a trailing four-quarter average earnings surprise of 25.9%.

Wolverine World Wide, Inc. (WWW) designs, manufactures, sources, markets, licenses and distributes footwear, apparel and accessories. It currently sports a Zacks Rank of 1. WWW delivered a trailing four-quarter average earnings surprise of 39.1%.

The Zacks Consensus Estimate for Wolverine’s current fiscal-year earnings and sales indicates growth of 46.2% and 6.5%, respectively, from the year-ago actuals.

Skechers U.S.A., Inc. (SKX) designs, develops and markets footwear, apparel and accessories worldwide. It currently flaunts a Zacks Rank of 1. SKX delivered a trailing four-quarter average earnings surprise of 12%.

The Zacks Consensus Estimate for Skechers’ current fiscal-year sales indicates growth of 8.2%, from the year-ago actuals.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 13 hours | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-28 | |

| Jul-28 | |

| Jul-16 | |

| Jul-16 | |

| Jul-13 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite