|

|

|

|

|||||

|

|

|

Seacoast Banking’s 23.4% return over the past six months has outpaced the S&P 500 by 7.9%, and its stock price has climbed to $31.35 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Seacoast Banking, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

We’re glad investors have benefited from the price increase, but we're cautious about Seacoast Banking. Here are three reasons there are better opportunities than SBCF and a stock we'd rather own.

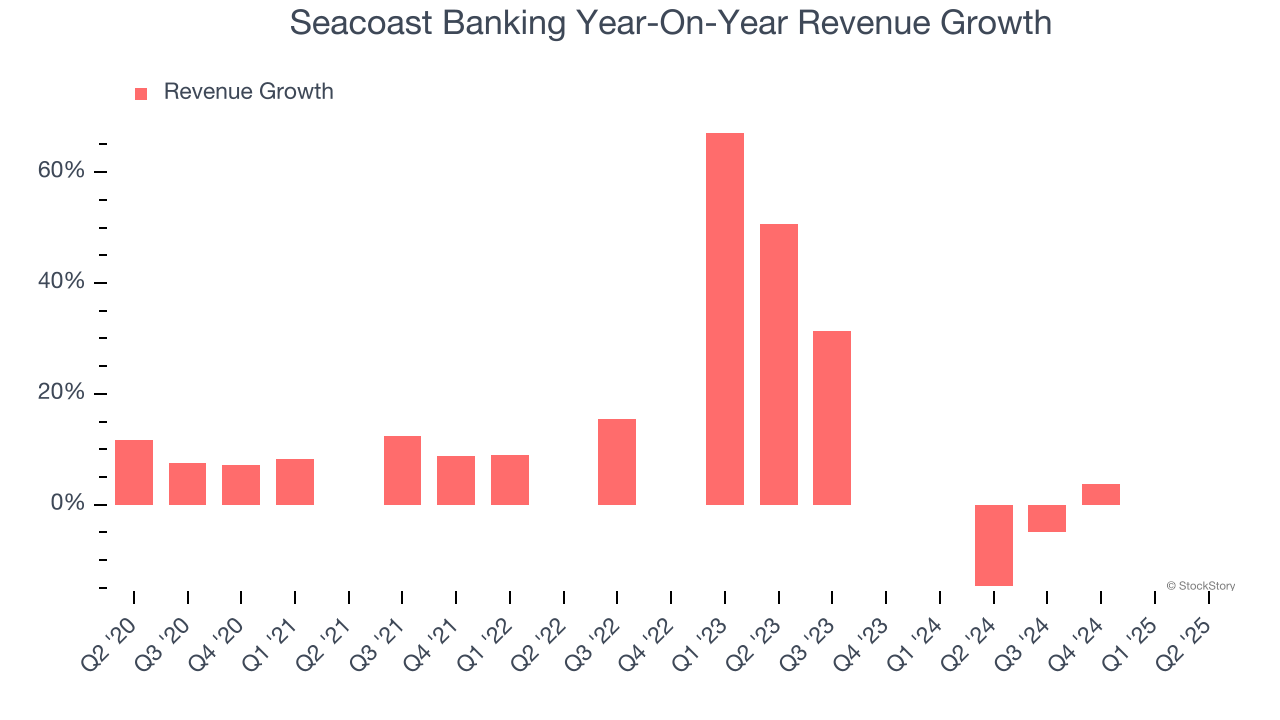

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Seacoast Banking’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 1% over the last two years was well below its five-year trend.

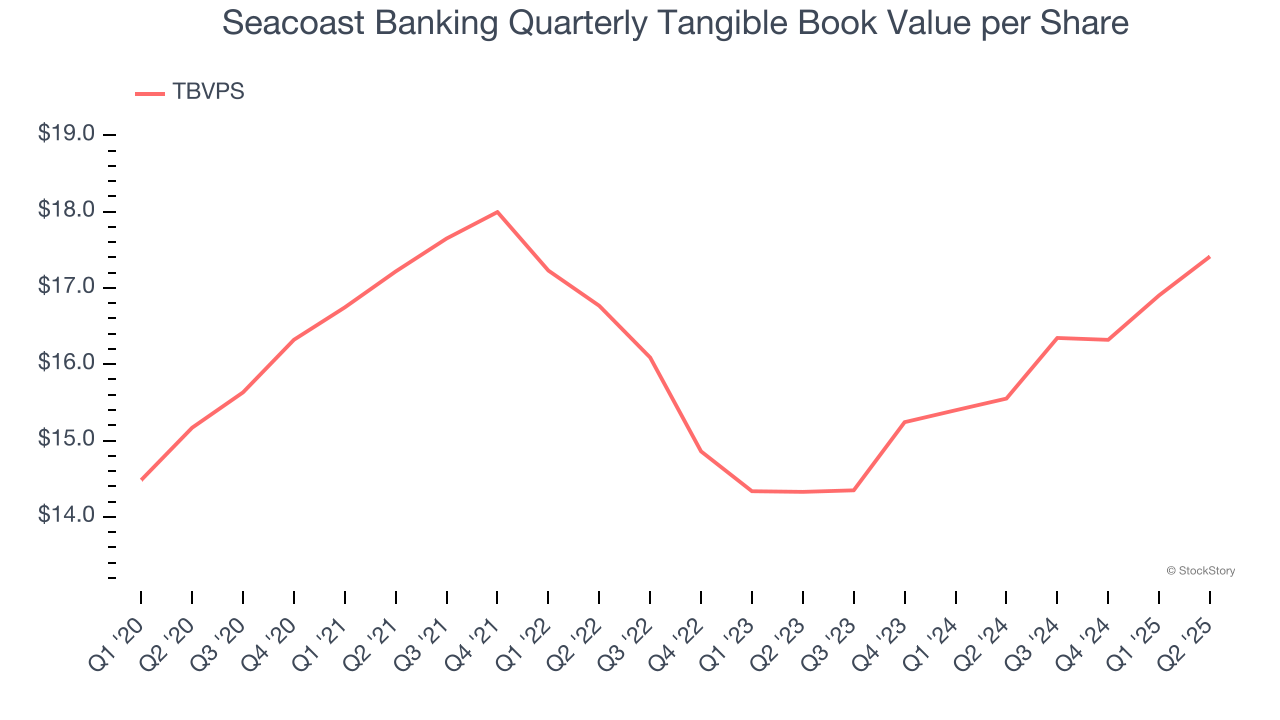

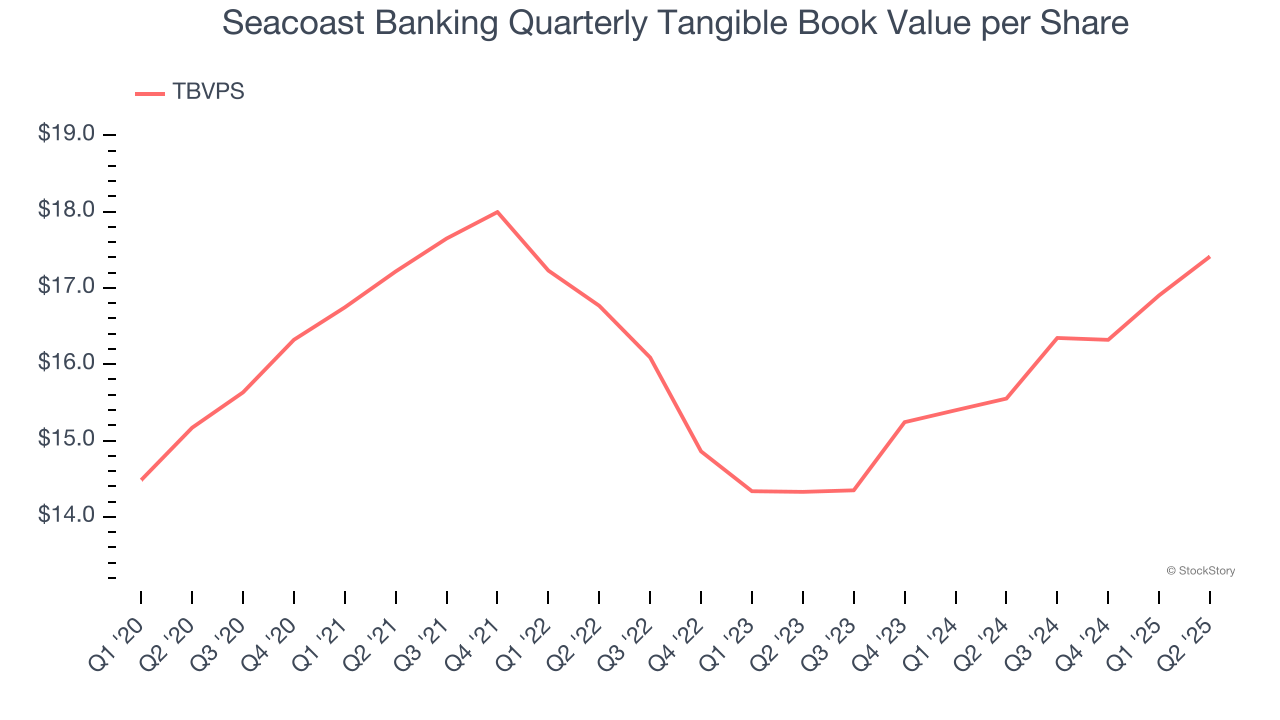

We consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation.

Although Seacoast Banking’s TBVPS increased by a meager 2.8% annually over the last five years, the good news is that its growth has recently accelerated as TBVPS grew at a decent 10.2% annual clip over the past two years (from $14.33 to $17.41 per share).

A bank’s tangible book value per share (TBVPS) increases when it generates higher net interest margins and keeps credit losses low, allowing it to compound shareholder value over time.

Over the next 12 months, Consensus estimates call for Seacoast Banking’s TBVPS to shrink by 7% to $16.20, a sour projection.

Seacoast Banking’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 1.1× forward P/B (or $31.35 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d recommend looking at the most dominant software business in the world.

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 | |

| Jul-06 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-27 | |

| Apr-23 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite