|

|

|

|

|||||

|

|

|

Even though DistributionNOW (currently trading at $15.95 per share) has gained 7.4% over the last six months, it has lagged the S&P 500’s 15.5% return during that period. This may have investors wondering how to approach the situation.

Is now the time to buy DistributionNOW, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We're swiping left on DistributionNOW for now. Here are three reasons you should be careful with DNOW and a stock we'd rather own.

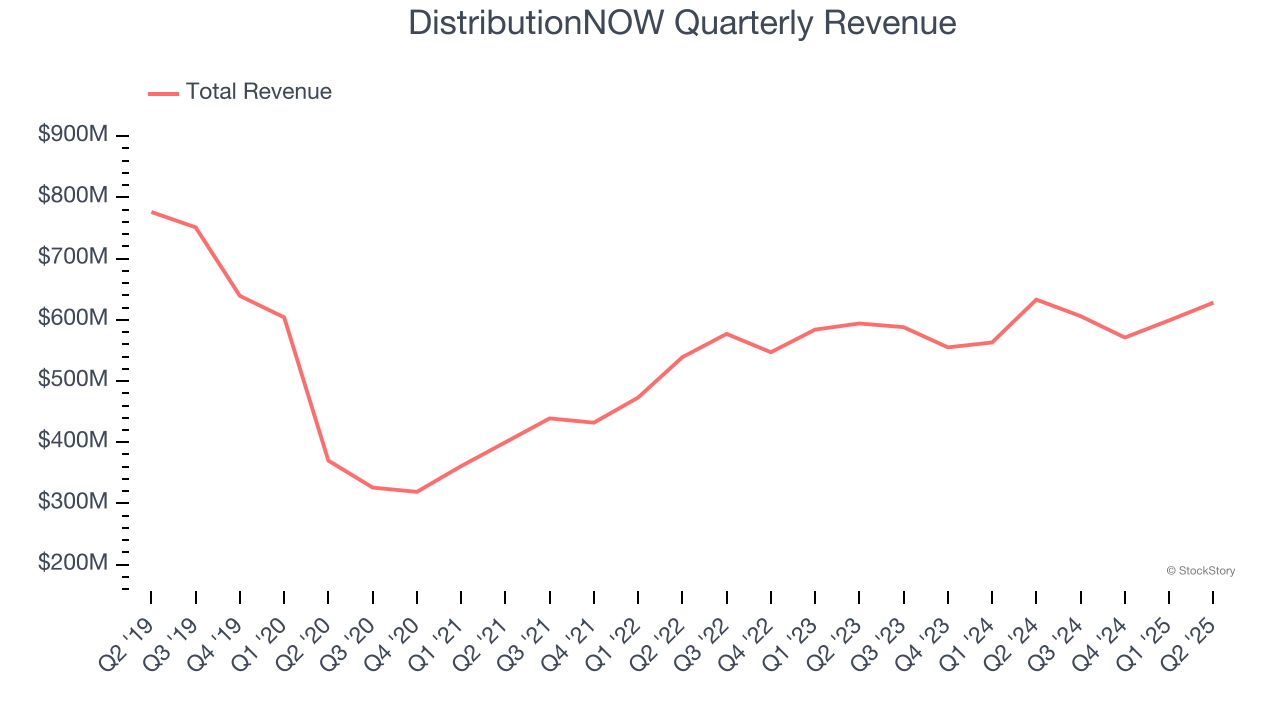

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, DistributionNOW struggled to consistently increase demand as its $2.40 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and signals it’s a low quality business.

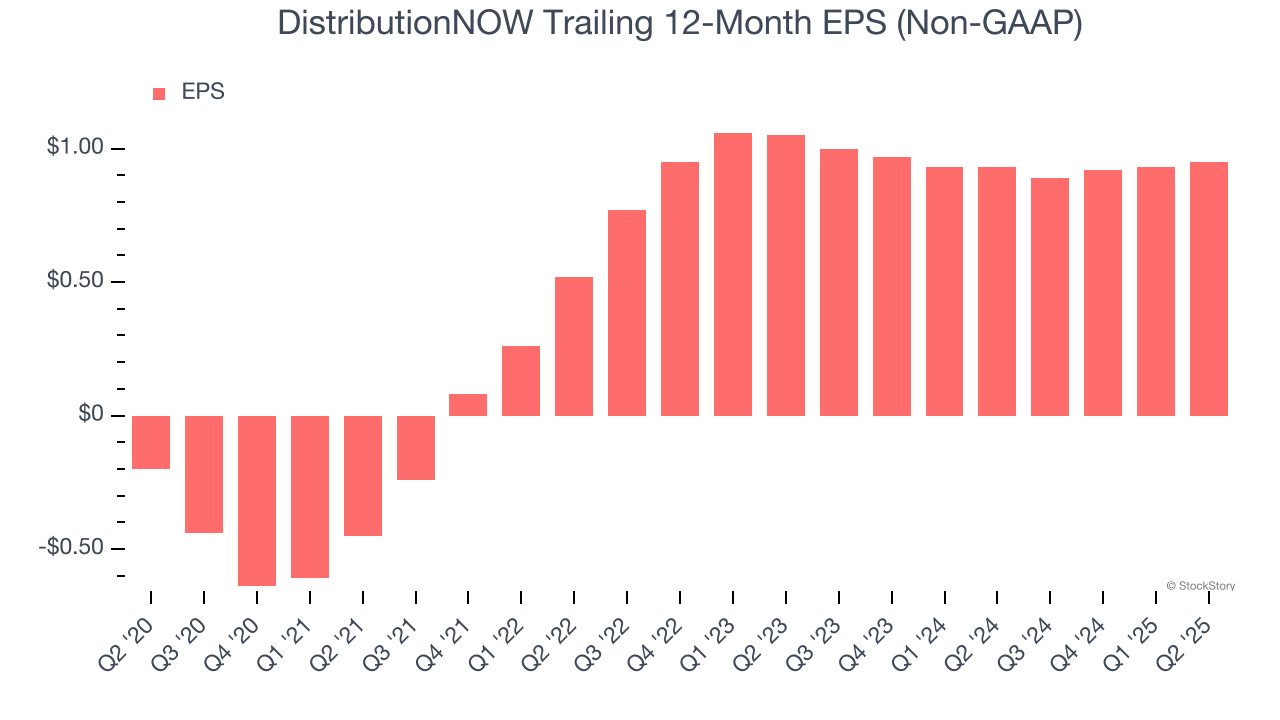

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for DistributionNOW, its EPS declined by 4.9% annually over the last two years while its revenue grew by 2.2%. This tells us the company became less profitable on a per-share basis as it expanded.

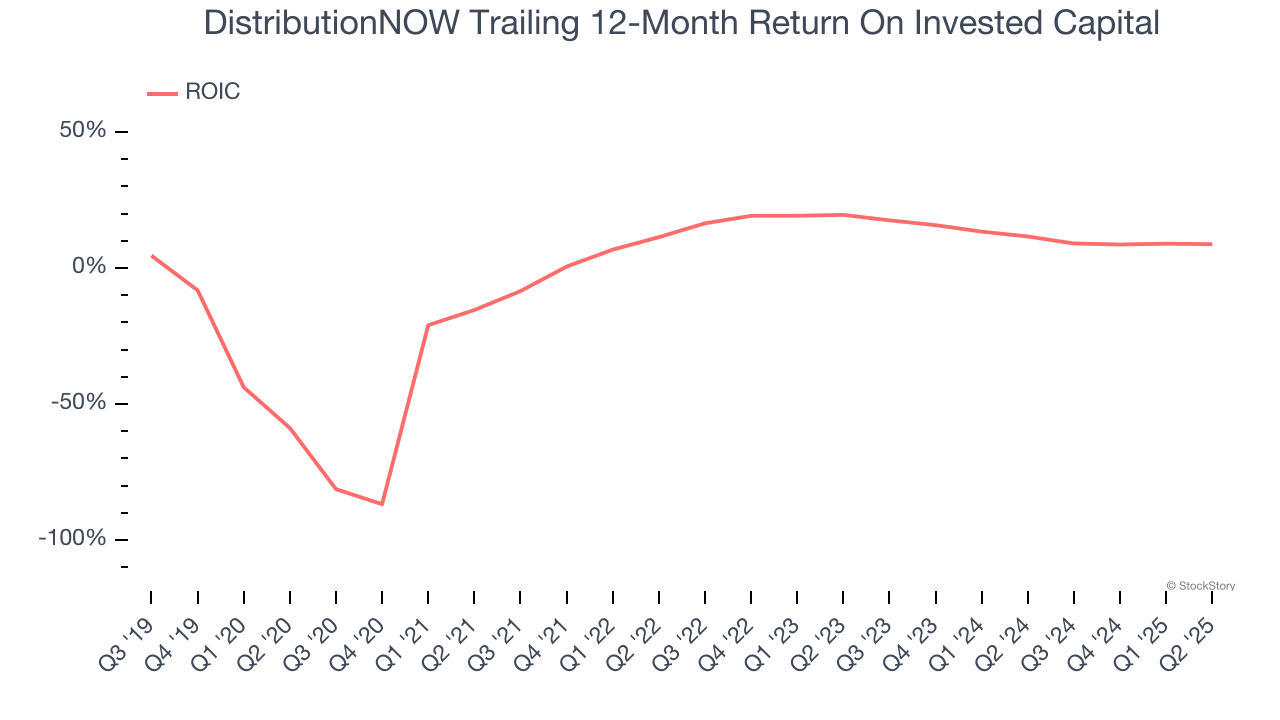

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

DistributionNOW historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.1%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We cheer for all companies making their customers lives easier, but in the case of DistributionNOW, we’ll be cheering from the sidelines. With its shares lagging the market recently, the stock trades at 19× forward EV-to-EBITDA (or $15.95 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. Let us point you toward an all-weather company that owns household favorite Taco Bell.

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 8 hours | |

| 8 hours | |

| Jul-31 | |

| Jul-30 | |

| Jul-23 | |

| Jul-08 | |

| May-21 | |

| May-08 | |

| May-07 | |

| May-07 | |

| May-04 | |

| Apr-21 | |

| Mar-03 | |

| Mar-02 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite