|

|

|

|

|||||

|

|

|

Alnylam Pharmaceuticals ALNY currently markets four approved drugs — Onpattro, Givlaari, Oxlumo, and Amvuttra — which together generated $1.14 billion in net product revenues, representing a 47% year-over-year increase in the first half of 2025. The company also benefits from collaboration agreements with partners like Regeneron, Roche, Novartis, and Sanofi, further contributing to its top line.

Alnylam and Regeneron are advancing cemdisiran in phase III studies, both in combination with pozelimab for myasthenia gravis and geographic atrophy, and as a monotherapy for paroxysmal nocturnal hemoglobinuria. The agreement regarding cemdisiran underwent a modification last year. Per the modified agreement, Alnylam granted exclusive rights to Regeneron to develop cemdisiran as monotherapy and in combination with anti-C5 antibodies for complement-mediated indications.

Alnylam, in collaboration with Roche, is developing investigational RNAi therapy zilebesiran in a mid-stage study (KARDIA-3) to treat hypertension. Recently, the companies reported encouraging Cohort A results, where a single 300 mg dose of zilebesiran achieved clinically meaningful and sustained reductions in office and ambulatory systolic blood pressure, as well as improvements in cardiovascular (CV) and renal biomarkers. While the results did not meet the pre-specified threshold for statistical significance, the data reinforce zilebesiran’s potential as a best-in-class therapy for patients with uncontrolled hypertension at high CV risk, supporting its use alongside standard antihypertensive treatments.

Building on positive phase II KARDIA data, Alnylam and Roche plan to launch the global phase III ZENITH CV outcomes study by late 2025, enrolling about 11,000 high-risk hypertension patients. The study will test whether twice-yearly 300 mg doses of zilebesiran can reduce the risk of major adverse cardiovascular events compared to placebo.

The successful advancement of cemdisiran and zilebesiran, alongside Alnylam’s marketed therapies, has the potential to significantly broaden its commercial portfolio.

Alnylam’s primary top-line driver is its newest drug, Amvuttra, which is approved for polyneuropathy of hereditary transthyretin-mediated (hATTR) amyloidosis and ATTR amyloidosis with cardiomyopathy in adults. The drug generated $801.9 million in global sales in the first half of 2025, representing a staggering 89% year-over-year growth, driven by patient demand.

Alnylam’s Amvuttra faces notable competition in the ATTR-CM market from Pfizer’s PFE Vyndaqel/Vyndamax (tafamidis) and BridgeBio’s BBIO Attruby (acoramidis), both of which are already approved for this indication. While Amvuttra is positioned with a differentiated clinical profile, Pfizer’s and BridgeBio’s therapies carry the advantage of oral administration and comparatively lower list prices in the United States.

Vyndaqel is one of the key in-line products that has driven improvement in Pfizer’s revenues in the first half of 2025. Global Vyndaqel family revenues of $3.1 billion rose 27% year over year in the first half of 2025, driven by continued demand growth due to increases in diagnosis and treatment rates, primarily in the United States and developed Europe. Pfizer’s Vyndaqel family includes global revenues from Vyndaqel as well as revenues for Vyndamax in the United States and Vynmac in Japan.

Approved in late 2024, Attruby is BridgeBio’s only marketed product. The drug generated sales worth $108.2 million in the first half of 2025, driven by solid uptake. BBIO reported that as of Aug. 1, 2025, 3,751 unique patient prescriptions for Attruby have been written by 1,074 unique healthcare providers since approval. BridgeBio is also currently evaluating acoramidis for the prevention of early-stage variant transthyretin amyloidosis in a late-stage study.

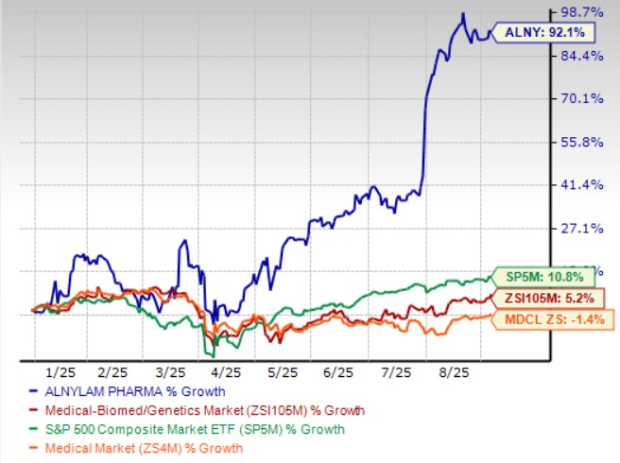

Shares of Alnylam have surged 92.1% so far this year compared with the industry’s 5.2% growth. The stock has also outperformed the sector and the S&P 500 index during the same time frame, as seen in the chart below.

From a valuation standpoint, Alnylam stock is expensive. Going by the price/sales ratio, the company’s shares currently trade at 23.98 trailing 12-month sales per share, much higher than 2.16 for the industry. The stock is also trading above its five-year mean of 20.97.

Estimates for Alnylam’s 2025 earnings have improved from $1.20 to $3.66 per share in the past 60 days, and estimates for 2026 earnings have improved from $4.07 to $9.28 over the same timeframe.

Alnylam currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite