|

|

|

|

|||||

|

|

|

Docusign's digital agreement software kept the business world moving during the pandemic's lockdowns and social distancing efforts.

Demand for its services slowed after 2021 as anti-COVID efforts relaxed, and the stock is currently trading 74% below its high.

Docusign's new agreement management platform is powered by AI, and it could reignite the company's growth.

Docusign (NASDAQ: DOCU) stock was a pandemic darling. Its stock price peaked at around $310 in 2021, a tenfold gain from its 2018 IPO price of $29. Lockdowns and social restrictions triggered by COVID-19 drove explosive demand for the company's digital contract management tools, which helped businesses close deals even when participants could not meet face to face.

But Docusign's growth slowed dramatically when social conditions returned to normal in 2022, which led to a sharp decline in its stock. Despite climbing by 40% over the past year, it remains 74% below its 2021 peak.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Fortunately for shareholders, the company's recovery looks set to continue thanks to strong demand for its new Intelligent Agreement Management (IAM) platform, which uses artificial intelligence (AI) to make contract management even simpler. Here's why investors might want to buy the stock while it's still trading at a steep discount to its all-time high.

Image source: Getty Images.

A study published earlier this year by global consulting firm Deloitte estimates that businesses combined are losing a whopping $2 trillion in economic value each year from poor contract management processes. Docusign's IAM platform aims to solve the "agreement trap" problem by using AI to help businesses draft, negotiate, and close deals more efficiently. But the platform doesn't stop there, because it also makes contract lifecycle management a breeze.

One of IAM's flagship features is a digital repository called Navigator, where businesses can store all of their agreements. It uses AI to automatically extract key details from each contract, and makes them discoverable via a search function, so employees no longer have to dig through individual documents for the information they need. Navigator also notifies managers of upcoming contract renewal dates, so deals don't expire unexpectedly.

In prepared remarks delivered last week in conjunction with the company's fiscal 2026 second-quarter report, CEO Allan Thygesen said the number of documents ingested by Navigator had soared by 150% compared to just six months ago. Businesses are now using it to process tens of millions of agreements every single month.

Docusign continues to roll out new IAM features, and the platform is likely to expand for the foreseeable future. For example, the company launched a new tool during fiscal Q2 called Agreement Preparation, which uses AI to detect the type of contract a business is trying to draft, and automatically create a template complete with the necessary fields (like areas for critical details and signatures). The larger an organization, the more potential time this tool could save it.

Docusign generated $800.6 million in revenue during fiscal Q2, which was comfortably above management's guidance range of $777 million to $781 million. That was a 9% increase from the year-ago period, and an acceleration from the 8% growth the company delivered in its fiscal first quarter.

Docusign was growing far more quickly at the height of the pandemic in 2021, mainly because it was investing aggressively in areas like marketing to attract new customers. This strategy worked well in the short term, but it was unsustainable and led to significant losses at the bottom line.

The new-look Docusign might be growing at a more modest pace, but it's highly profitable. It delivered generally accepted accounting principles (GAAP) net income of $135.1 million during the first two quarters of fiscal 2026, and adjusted (non-GAAP) net income of $385.9 million.

The non-GAAP metric is management's preferred measure of profitability because it excludes one-off and non-cash expenses like stock-based compensation, so it's a better reflection of how much actual money the business is generating.

Consistent profits give Docusign the flexibility to start funneling more money into growth-oriented expenses like marketing once again, which could fuel a further acceleration in revenue growth.

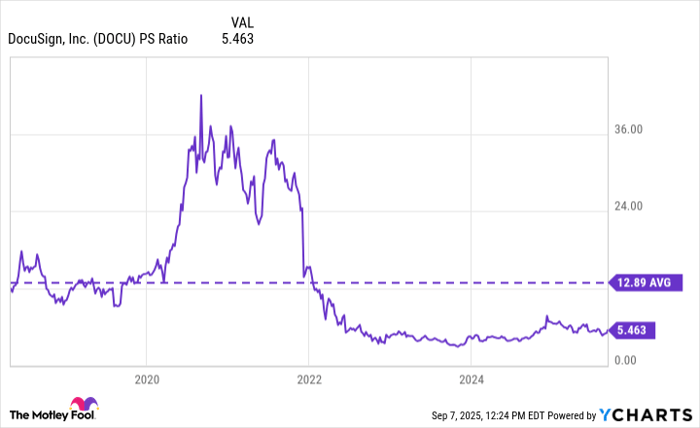

Docusign's price-to-sales (P/S) ratio peaked at above 40 during 2021 -- an unsustainable valuation. However, the 74% decline in the stock since then, combined with the company's consistent revenue growth, has pushed its P/S ratio down to a more reasonable 5.4. That is actually a steep discount to its average of 12.9, which dates back to its IPO in 2018.

Data by YCharts.

On that note, Docusign's strong fiscal Q2 revenue prompted management to increase its fiscal 2026 guidance for the second time this year. The company now expects to generate up to $3.201 billion in revenue, which is $60 million higher than the $3.141 billion top end of its original guidance range.

The momentum in Docusign's business is clear, which explains why its stock has climbed by more than 40% over the past year. The IAM platform could be the secret to unlocking further upside, so investors might want to take advantage of the stock's attractive valuation by buying it now.

Before you buy stock in Docusign, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Docusign wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $671,288!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,031,659!*

Now, it’s worth noting Stock Advisor’s total average return is 1,056% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 8, 2025

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Docusign. The Motley Fool has a disclosure policy.

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-16 | |

| Feb-14 | |

| Feb-13 | |

| Feb-12 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite