|

|

|

|

|||||

|

|

|

Altria Group, Inc. (MO) continues to advance its smoke-free strategy. The second quarter of 2025 highlights the steep climb ahead. Domestic cigarette shipments in the smokeable products segment fell 10.2% year over year. Marlboro’s retail share of the total cigarette category slipped 0.9 points to 41%, though the brand held its ground in the premium tier, edging up 0.2 points to 59.5% both year over year and sequentially.

In contrast, smoke-free offerings, particularly on! nicotine pouches showed solid momentum. Shipments rose 26.5% to 52.1 million cans in the second quarter. The brand captured 8.7% of the total U.S. oral tobacco category, while the segment overall delivered double-digit adjusted operating companies income (“OCI”) growth with margins of 68.7%. Broader consumer engagement, through both in-person events and digital campaigns, also appears to be driving higher awareness and trial.

Even so, combustibles remain Altria’s economic anchor. The smokeable products segment generated $2.9 billion in adjusted OCI in the second quarter, with margins at 64.5%. That scale underscores how far smoke-free products must climb before they can meaningfully offset cigarette declines.

Overall, the quarter illustrates a company in transition. Cigarettes are shrinking, but still highly profitable. Oral nicotine is expanding, but from a much smaller base. Altria’s vision of “Moving Beyond Smoking” is progressing, though the pace remains gradual, and the balance of decline versus growth will continue to define its journey.

Philip Morris International Inc. (PM) presents a sharper contrast in smoke-free progress. In the second quarter of 2025, Philip Morris generated 41% of net revenues from smoke-free products, with an 11.8% increase in shipment volumes. Philip Morris also reported nicotine pouch shipments rising more than 40% in the United States, underscoring faster category adoption and stronger traction in reduced-risk offerings.

Turning Point Brands, Inc. (TPB) is accelerating its shift to modern oral, with the second quarter of 2025 revenues up 25% to $116.6 million. Modern Oral contributed $30.1 million (26% of sales), with white pouch sales rising nearly eightfold year over year. While legacy Stoker’s brands stayed resilient, Turning Point Brands raised full-year Modern Oral sales guidance to $100-$110 million. Turning Point Brands’ strong pouch momentum highlights its growing role in the smoke-free transition.

Shares of Altria have gained 0.8% in the past month against the industry’s decline of 3.2%.

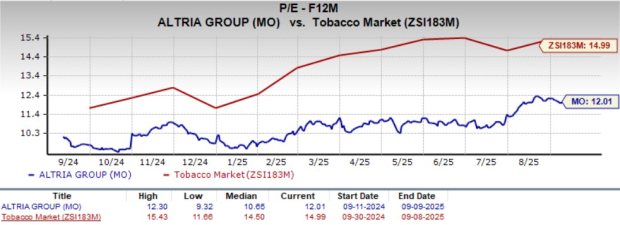

From a valuation standpoint, MO trades at a forward price-to-earnings ratio of 12.01X, down from the industry’s average of 14.99X.

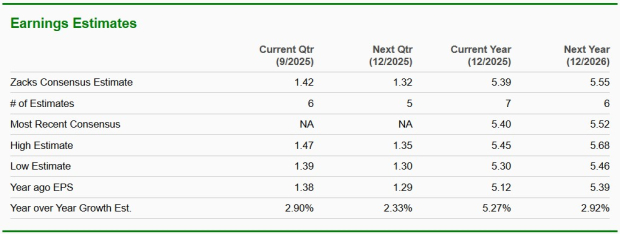

The Zacks Consensus Estimate for MO’s 2025 and 2026 earnings implies year-over-year growth of 5.3% and 2.9%, respectively.

Altria currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-03 | |

| Jul-03 | |

| Jul-02 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite