|

|

|

|

|||||

|

|

|

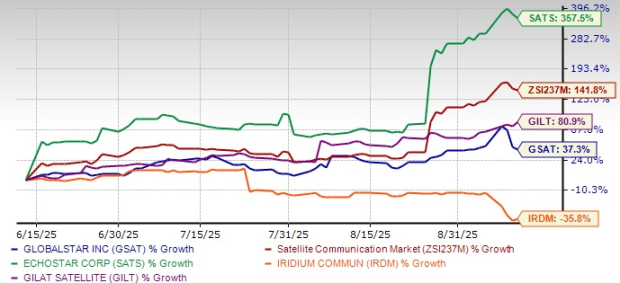

Globalstar, Inc. GSAT stock has been on a tear, gaining 37.3% in the past three months. While the gains are impressive, GSAT has underperformed the Satellite and Communication Industry, which is up a staggering 141.8%.

The stock was down 2.7% and closed the last session at $30.29, below its 52-week high of $41.10. Investors would be contemplating now whether GSAT’s momentum has the staying power, or they should book profits and exit.

Given the company’s strong second-quarter results, strategic developments and innovative product pipeline, Globalstar appears well-positioned for further upside.

Globalstar is benefiting from continued growth in wholesale capacity services and commercial IoT revenues. Second quarter revenues came in at $67.1 million, up 11% year over year, largely driven by a 10% increase in service revenues, with wholesale capacity services providing a strong tailwind. Commercial IoT is witnessing an increase in the average number of subscribers, underpinned by robust growth in gross activations in the trailing 12 months.

GSAT is also advancing new innovative platforms, such as the RM200 two-way module and XCOM RAN, which could drive the top line further. RM200M module is the first satellite module to feature integrated GNSS, Bluetooth, an accelerometer and an application processor, enabling advanced two-way communication. It is witnessing growing traction across verticals like oil & gas, defense and MVNOs, and has been tested by over 50 partners.

XCOM RAN platform is a software-defined end-to-end solution primarily for terrestrial wireless markets, designed to deliver lower latency, improved spectrum efficiency, and dynamic spectrum sharing. With XCOM RAN, GSAT is eyeing entry into terrestrial wireless markets, significantly broadening its total addressable market. The platform will also enable next-gen hybrid satellite-terrestrial network architectures, thereby further expanding business opportunities.

Globalstar is in the midst of a comprehensive infrastructure upgrade and recently launched its global ground infrastructure program for its next-generation Extended MSS Network, or the C-3 system. Under this program, it will add about 90 antennas across 35 ground stations in 25 countries, which will significantly boost network capacity and resiliency.

As a part of this expansion, it recently announced construction of another gateway infrastructure at its current ground station at OTE S.A.’s commercial teleport in Nemea, Greece. Last month, it announced the construction to expand its Singapore ground station. The facility, hosted by Singtel since 2008, will soon boast two additional 6-meter tracking antennas designed to support Globalstar’s third-generation C-3 system.

In June 2025, Globalstar signed a launch services agreement with SpaceX for the deployment of nine new satellites. These satellites, under construction by MDA, are scheduled for launch first in late 2025 and then in 2026 to replace the existing constellation and ensure service continuity.

Client roster expansion is another positive. GSAT is witnessing growing traction in the government, especially U.S. federal agencies and defense markets. It has teamed up with the U.S. Army for research and development efforts to test satellite-enabled edge processing solutions for autonomous and secure operations in challenging environments.

The company also completed a proof of concept with Parsons, demonstrating integration of its satellite network with Parsons’ software-defined communications platform across three European ground stations. It was followed by a capacity access agreement, moving the collaboration into the commercial phase.

Lastly, GSAT’s asset is its globally harmonized and licensed spectrum. Management highlighted that owning proprietary spectrum is the key differentiator in the satellite communications space as it provides a long-term competitive advantage. GSAT faces tough competition in this space from the likes of EchoStar SATS, Iridium Communications IRDM and Israel-based Gilat Satellite Networks GILT. Recently, EchoStar announced the sale of its AWS-4 and H-block spectrum licenses for approximately $17 billion to SpaceX, sending the stock soaring.

Given strength in strategic partnerships, innovative pipeline and robust infrastructure upgrade, Globalstar reiterated its 2025 revenue outlook of $260-$285 million and expects adjusted EBITDA margins around 50%. The confidence in guidance reflects the company’s strong execution and resilience in the face of potential tariff and cost headwinds.

GSAT stock is trading at a substantial premium, with a forward 12-month price/sales of 12.78X compared with the industry’s 1.37X.

In comparison, IRDM, SATS and GILT trade at multiples of 2.18X, 1.49X, and 1.3Xrespectively.

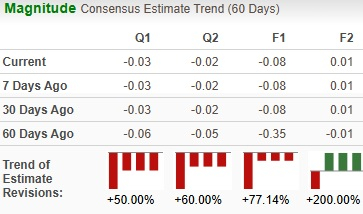

Analysts have significantly increased earnings estimates for the current year.

Iridium has declined 35.8%, while GILT and SATS shares have soared 37.3% and 357.5%, respectively, over the past three months.

At present, GSAT sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Given robust long-term drivers, robust guidance, and rising earnings estimates, GSAT remains a compelling opportunity even after its recent surge.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-09 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite