|

|

|

|

|||||

|

|

|

Oklo Inc. (OKLO) has been one of the hottest names in the nuclear energy space, with shares soaring nearly 19% after unveiling a $1.68 billion private nuclear fuel recycling facility in Oak Ridge, TN. The project — announced on Sept. 4 and expected to create 800 jobs as the first-of-its-kind commercial recycling site in the United States — ties directly into America’s growing demand for secure fuel supply amid the energy-hungry rise of artificial intelligence (AI). The gains on the back of this Tennessee announcement have also taken Oklo’s one-year stock surge to more than 1200%.

A lot of the buzz around Oklo comes from its unique position at the meeting point of clean energy and AI. The data centers that power AI technology require huge amounts of reliable electricity. Oklo's advanced, small modular nuclear reactors (SMRs) are being promoted as a perfect solution to this massive energy need.

Nuclear energy stocks more broadly are heating up, and for a good reason. This year, President Donald Trump has put nuclear power firmly in the spotlight, while countries worldwide have pledged to triple nuclear capacity by 2050. Yet, even against this supportive backdrop, investors need to step back and assess whether Oklo’s fundamentals truly justify the hype.

Oklo’s story is built around scale and ambition. The company touts a 14 GW pipeline that could translate into nearly $5 billion in annual revenues by 2028. Its Aurora microreactors, designed to run on recycled fuel, target data centers, military bases and industrial hubs. Instead of selling reactors, Oklo aims to own and operate them, securing revenues through long-term power purchase agreements. Partnerships with names like Liberty Energy, Vertiv and Korea Hydro & Nuclear Power enhance its credibility. On paper, this integrated model looks promising and gives the company a strategic angle that competitors lack.

Despite the big headlines, Oklo is still a pre-revenue company. Its first commercial reactor isn’t expected online until 2027 or 2028 at the earliest, and the Tennessee recycling facility won’t begin operations until the early 2030s. Meanwhile, the annual cash burn is estimated between $65 million and $80 million, a figure that will demand ongoing capital raises. Regulatory challenges are another concern. Oklo’s initial application was rejected by the Nuclear Regulatory Commission in 2022, and even if resubmitted in late 2025, reviews could stretch two to three years. Such delays could easily push commercial revenues further out, leaving investors holding a highly speculative bet. The long timeline also exposes shareholders to greater volatility, especially if market enthusiasm for nuclear cools.

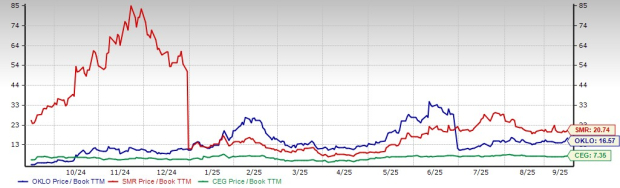

The financing structure only adds to investor risk. In June 2025, Oklo raised $440 million in equity, diluting existing shareholders. More raises appear inevitable given the capital intensity of nuclear projects. At a price-to-book multiple of 16.6, Oklo trades well above peers. NuScale Power (SMR), which already holds U.S. regulatory approval, trades at an even higher multiple, but at least has international deployment opportunities lined up. By contrast, Constellation Energy (CEG), the largest U.S. nuclear operator with decades of profitable operations and dividends, trades at a far more reasonable valuation and offers cash-backed stability. Against these benchmarks, Oklo’s market premium looks stretched and hard to defend in the absence of revenue.

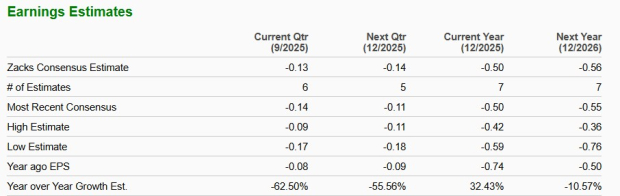

Oklo’s earnings outlook underlines the speculative nature of the stock. Consensus estimates point to EPS improving by 32% in 2025, but dropping by 11% in 2026, reflecting the absence of sustainable profits. Meanwhile, Constellation Energy continues to expand earnings through long-term power contracts with tech giants like Microsoft and Meta. NuScale, though unprofitable, benefits from global SMR adoption momentum and government-backed funding programs. In contrast, Oklo lacks revenue visibility, making it dependent on investor enthusiasm rather than financial fundamentals. This leaves its shares more prone to sharp swings in sentiment, rather than being guided by tangible earnings trends.

Oklo’s announcement of a recycling facility has undeniably added excitement to the nuclear revival narrative, and the short-term stock surge reflects that. But enthusiasm does not erase the risks. Years of regulatory hurdles, steep cash burn, and repeated dilution stand in stark contrast to the company’s lofty market valuation. Growth estimates show little near-term path to profitability, and analyst revisions point to a bumpy road ahead. In this context, while companies like Constellation Energy and NuScale already show more predictable earnings and project rollouts, Oklo is still mostly running on future promises rather than proven results. For now, OKLO is rated a Zacks Rank #4 (Sell) stock — a reminder that investors should tread carefully despite the buzz.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 |

SMR Stock Plunges 7% On Q4 Revenue Miss But What's Fueling Retail Dip Buyers?

SMR

New feeds test provider finance

|

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite