|

|

|

|

|||||

|

|

|

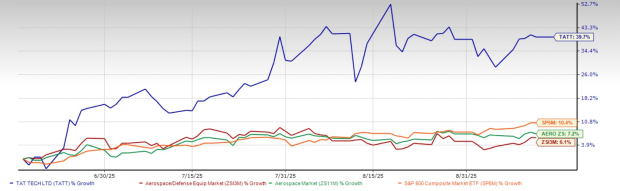

Shares of TAT Technologies Ltd. TATT have gained 39.7% in the past three months, outperforming the 6.1% growth of the Zacks Aerospace-Defense Equipment industry. It also beat the Zacks Aerospace sector’s growth of 7.2% and the S&P 500’s rise of 10.4%.

Other aerospace-defense equipment stocks, such as AAR Corporation AIR and Rocket Lab USA, Inc. RKLB, have also outperformed the industry in the past three months. Share of AIR have gained 9.2%, while shares of RKLB surged 100.9%.

While TATT’s recent stock performance may encourage some investors to jump in quickly to add this stock to their portfolio, it is essential to examine the factors driving this rise. The critical consideration is whether the company can maintain this momentum or if potential risks could hinder future growth. Taking this approach allows investors to make a more informed decision.

TAT Technologies’ share gains over the past three months appear to be driven by its strong quarterly results and new contract wins.

In August, TATT reported its second-quarter adjusted earnings of 30 cents per share, which increased 20% year over year, backed by strong profit. The company’s net sales of $43.1 million also registered solid year-over-year growth of 18%. Such impressive quarterly results are indicative of the solid demand that TATT’s OEM and MRO products enjoy in the broader market.

In August, the company signed a $12 million agreement to provide MRO services for the GTCP331-500 Auxiliary Power Unit (APU) on Boeing 777 aircraft. This contract underscores TAT’s expanding role in the global APU market and strengthens its position as a trusted partner for commercial carriers.

TAT Technologies offers solid growth prospects, backed by a strong balance sheet. At the end of the second quarter of 2025, the company reported $43 million in cash and cash equivalents compared with only $2 million in current debt and $10 million in long-term debt. This demonstrates TATT’s healthy solvency position, which should provide it with the flexibility to support its future growth plans, including potential accretive acquisitions.

Moreover, since July 2025, TAT Technologies has been experiencing a rebound in MRO intake, which, combined with recent contract wins, is expected to boost its MRO revenues by late 2025 or the first half of 2026.

Impressively, in the second quarter, its backlog rose by $85 million to reach $524 million. Such backlog growth provides visibility into future revenue growth across both OEM and MRO services, over the long run.

With rising MRO intake and new program wins, such as the Boeing 777 APU contract, the company appears well-positioned to deliver consistent growth and create long-term value for shareholders.

Let’s take a sneak peek at TATT’s near-term estimates to check if they reflect a similar growth story.

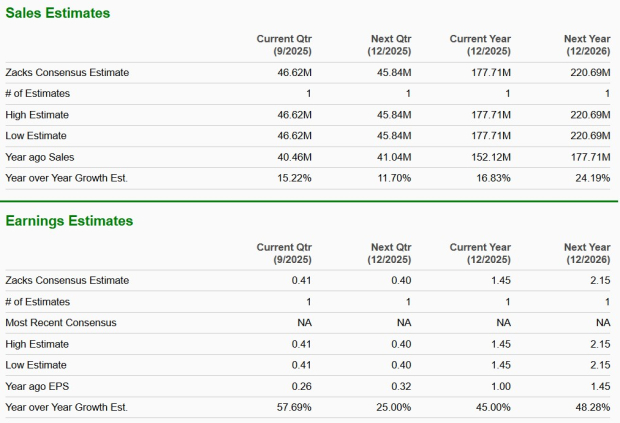

The Zacks Consensus Estimate for TATT’s 2025 revenues indicates a solid improvement of 16.8% from the prior-year level. The estimate for its earnings also indicates an improvement of 45% from the prior-year level.

The Zacks Consensus Estimate for TATT’s 2026 revenues and earnings also indicates a similar improvement.

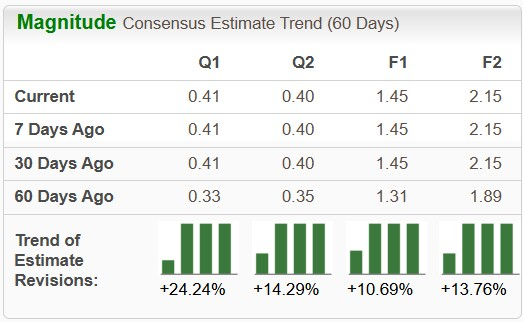

Further, the upward revision in its near-term earnings estimate over the past 60 days suggests investors’ increasing confidence in this stock’s earnings generation capabilities.

Despite its solid prospects, TAT Technologies faces a few industry-specific challenges. In particular, as persistent supply-chain disruptions and higher raw material costs continue to affect the aerospace industry, it might affect TATT’s ability to deliver on time and at optimal margins. These pressures are further complicated by inflation and labor costs, which could limit profitability if they persist over a long run.

Geopolitical risks also remain a concern, given the company’s operations in Israel. Regional conflicts create uncertainty for operations and logistics and any escalation could disrupt TATT’s business activity or delay customer projects.

TATT shares are trading at a discount, with its trailing 12-month Price/Book (P/B TTM) being 2.78X compared with its industry’s average of 16.41X.

On the contrary, TATT’s industry peer, AIR is trading at a P/B TTM of 2.20X, while another RKLB is trading at a P/B TTM of 37.14X.

Return on Equity (ROE) measures how effectively a company uses shareholders’ equity to generate profits. TATT currently has an ROE of 10.90, which is above the industry average of 9.31. This indicates that, compared with its industry, the company is generating higher returns on its equity.

TAT Technologies remains well-positioned for long-term growth, supported by rising earnings, strong cash reserves, a growing backlog and recent contract wins boosting its aerospace MRO and defense roles. Despite near-term challenges from supply-chain disruptions and geopolitical risks linked to its Israel-based operations, TATT's robust ROE, rising earnings estimates and discounted valuation make it an attractive opportunity for investors seeking exposure in the aerospace-defense equipment industry, especially given its recent outperformance at the bourses.

TATT currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 20 min | |

| 23 min | |

| 29 min | |

| 31 min | |

| 33 min | |

| 1 hour |

Rocket Lab Reports Earnings Tonight: What Do Prediction Markets Say About Neutron Launches in 2026?

RKLB

Benzinga Prediction Markets

|

| 2 hours | |

| 2 hours | |

| 5 hours | |

| 5 hours |

SpaceX Rivals Rocket Lab, AST SpaceMobile About To Report Earnings. What To Expect.

RKLB

Investor's Business Daily

|

| 12 hours | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

SpaceX Stock Lands Upgrade, Rocket Lab Surges After Electron Mission

RKLB +9.46%

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite