|

|

|

|

|||||

|

|

|

Super Micro Computer SMCI and Hewlett Packard Enterprise HPE are both leading the server market, enabling organizations with server-based capabilities and serving their high computing power requirements.

Per a report by Grand View Research, the Global Server market is expected to witness a CAGR of 9.8% from 2024 to 2030. Strong adoption of servers across industries like healthcare, retail, BFSI, manufacturing, education and others will drive the server space.

With this strong industry growth forecast, the question remains: Which stock has more upside potential? Let’s break down their fundamentals, growth prospects, market challenges and valuation to determine which offers a more compelling investment case.

Super Micro Computer’s growth is driven by the need for artificial intelligence (AI) workloads. As a growing number of data centers are proliferating and existing ones are expanding their capacity, the need for SMCI’s high-performance and energy-efficient servers is rising.

SMCI’s next-generation air-cooled and liquid-cooled GPU and AI platforms used in servers are experiencing massive growth in traction, leading to more than 70% contribution to its top line in the fourth quarter of fiscal 2025. Both the enterprise and cloud service providers are adopting SMCI’s cooling technology.

Despite the massive potential of SMCI’s server offerings, the company is facing some near-term challenges, including delayed purchasing decisions from customers as they are evaluating the adoption of next-generation AI platforms.

SMCI is also facing margin contraction due to the growing price competition and price adjustments as companies are second-guessing their shift from older to newer platforms like Blackwell. In the last reported quarter, SMCI also incurred a one-time inventory write-down on older-generation GPUs and related components, further affecting its margins.

SMCI’s near-term margin outlook is dim. The Zacks Consensus Estimate for SMCI’s first and second quarters of fiscal 2026 show a decline of 37% and 5% respectively. The Zacks Consensus Estimate for fiscal 2026 and 2027 EPS has also been revised downward in the past 60 days.

HPE’s server business grew 16.1% in the third quarter of fiscal 2025, reaching an all-time high, driven by large artificial intelligence (AI) deals and growth in AI systems. HPE’s AI systems revenues touched $1.6 billion, which was also an all-time high, as HPE was able to deliver a large GB 200 system, as reported in its earnings.

HPE’s AI server business is driven by enterprises deploying compute-heavy infrastructure and AI factory proliferation, resulting in a 100% quarter-over-quarter increase in orders. HPE reported in its third-quarter earnings call that its Server operating margin improved sequentially due to the reforms it made in pricing and discounting early in the year.

HPE’s newly introduced ProLiant Gen 12 server platform, focused on performance improvement, security enhancement and direct liquid cooling technology, is a massive upgrade over its predecessors, making it capable of strengthening HPE’s competitive position in the server market.

These factors have led the company to raise the estimates of its non-GAAP net earnings per share to $1.88-$1.92, up from $1.78-$1.90. The Zacks Consensus Estimate for fiscal 2025 has been revised upward in the past 30 days, and fiscal 2026 EPS has also been revised upward in the past seven days.

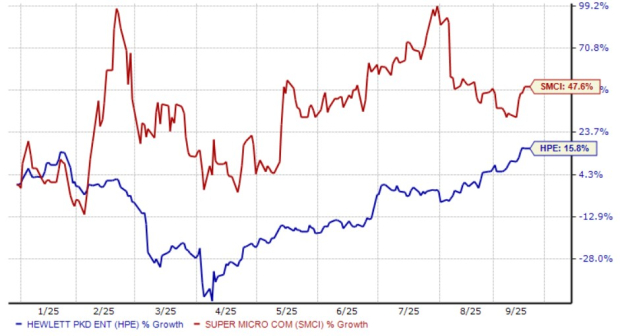

Year to date, the shares of SMCI and HPE have gained 47.6% and 15.8%, respectively.

SMCI is trading at a forward 12-month ratio of 0.84X, which is higher than its median of 0.82X, while HPE is trading at a forward sales multiple of 0.83X, above its median of 0.82X.

HPE is comparatively cheaper and has brighter prospects in the server market as it is strongly driven by its deep server portfolio and GreenLake offerings. In the meantime, SMCI is facing near-term challenges stemming from delayed purchasing decisions from customers and margin contraction from pricing pressure.

Furthermore, HPE carries a Zacks Rank #2 (Buy) at present, making the stock a stronger pick compared with SMCI, which has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 |

Top Trump antitrust official leaves post following disputes over big mergers

HPE -6.76%

Associated Press Finance

|

| Feb-12 |

Cisco Memory Chip Warning Sends Down Dell, HPE, Arista, NetApp Shares

HPE -6.76%

Investor's Business Daily

|

| Feb-12 |

Cisco Profit Margin Outlook Sends Down Dell, HPE, Arista, NetApp Shares

HPE -6.76%

Investor's Business Daily

|

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite