|

|

|

|

|||||

|

|

|

Salesforce, Inc. CRM recently delivered another strong set of financial results, with revenues rising 10% year over year to $10.25 billion in the second quarter of fiscal 2026. One of the standout highlights for the reported quarter was the rapid growth of its Data Cloud business, which saw a 140% surge in customer count on a year-over-year basis. This robust growth underscores how important data integration has become for enterprises seeking to adopt artificial intelligence (AI) at scale.

Salesforce is making its Data Cloud platform a key part of its growth strategy. The Data Cloud platform brings together customer data from multiple sources and makes it usable across Salesforce products. More than half of the Fortune 500 already use Data Cloud, and the company is seeing customers expand usage as AI adoption accelerates.

Salesforce is also integrating the Data Cloud platform with its other tools like Agentforce, Tableau and Slack. These connections make it easier for enterprises to activate their data and apply AI across operations. This integration could drive higher contract values and deeper customer relationships for CRM.

Salesforce estimates that its data-related business is already generating around $7 billion annually. With a consumption-based pricing model, we believe that the revenue growth potential for the Data Cloud platform is significant.

We also believe that the Data Cloud platform has the potential to anchor Salesforce’s revenues, which are currently witnessing a decelerating growth trend. After years of consistent double-digit revenue increases, the momentum has faded. In the first and second quarters, total revenues rose 8% and 10%, respectively, year over year. The Zacks Consensus Estimate depicts that this trend will persist, with high single-digit growth expected for fiscal 2026 and 2027.

Salesforce faces intensified competition from Microsoft Corporation MSFT and Snowflake Inc. SNOW in the data cloud space.

Microsoft offers data services through its Azure Data platform. The company has already integrated the platform with its other productivity tools, including Power Platform, Dynamics 365 and Copilot AI, to enhance user experience and attract new clients. Many companies already use Microsoft’s cloud and productivity software, making it easy to add its data services.

Snowflake is another major competitor, known for its powerful cloud-based data warehouse. Unlike Salesforce, Snowflake focuses only on data, allowing companies to store, process and share large volumes easily. It also supports multiple clouds and has strong analytics tools.

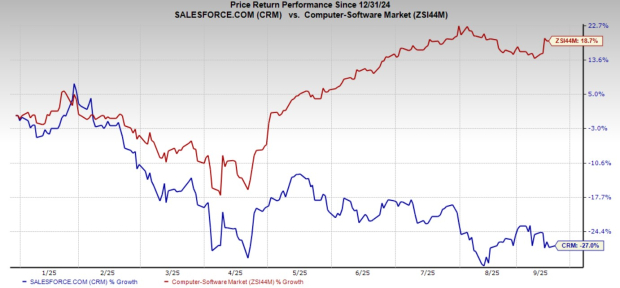

Shares of Salesforce have plunged 27% year to date against the Zacks Computer – Software industry’s growth of 18.7%.

From a valuation standpoint, CRM trades at a forward price-to-earnings ratio of 19.96, significantly below the industry’s average of 33.11.

The Zacks Consensus Estimate for Salesforce’s fiscal 2026 and 2027 earnings implies a year-over-year increase of approximately 11.2% and 11.7%, respectively. Estimates for fiscal 2026 and fiscal 2027 have been revised upward in the past 30 days.

Salesforce currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 10 hours | |

| 11 hours | |

| 15 hours | |

| 16 hours | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite