|

|

|

|

|||||

|

|

|

Chewy shares sank after earnings, as investors didn't like the higher expenses the company had in the quarter.

The company, however, saw strong revenue growth and improving margins.

The stock looks attractively valued compared to retail peers.

Share prices of Chewy (NYSE: CHWY) plunged after earnings came out last week, despite sales that topped analyst expectations and the company raising its full-year revenue outlook. While some media outlets and pundits pointed to the drop in GAAP earnings as the reason for the fall, professional investors generally pay little attention to this metric, and Chewy saw a big one-time tax benefit a year ago that explains the drop.

The real reason for what is now a 10.3% decline appears to be that the pet products e-commerce company had a larger-than-expected increase in operating expenses, which led to its earnings before interest, taxes, depreciation, and amortization (EBITDA) coming in slightly below expectations. Chewy has always had a business model with high fixed costs, and investors want to see more operating leverage out of the company. However, this is generally an easy issue to fix, and the sell-off looks overdone.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

Although revenue growth stagnated in the first half of last year, Chewy's sales growth has been strong in recent quarters. This continued into its fiscal second quarter (which ended Aug. 3), with revenue jumping nearly 9% year over year to $3.1 billion. That was just ahead of the company's earlier forecast for sales of between $3.06 billion and $3.09 billion.

Chewy has a very steady business, with the bulk of its sales coming from consumables, such as dog food and pet medication. On top of that, more than 80% of its sales come from autoship customers who have their orders scheduled to be delivered regularly. Autoship sales climbed nearly 15% year over year to $2.6 billion, and provided 83% of total revenue. Net sales per active customer (NSPAC) continued to increase, rising 5% on the year to $591. Chewy also added 150,000 active customers in the quarter compared to fiscal Q1.

Operating leverage, which is affected by gross margin and operating expenses, has been a big focus for investors. Chewy has had solid improvement in gross margin, and that continued in Q2, as it ticked up 90 basis points year over year and 80 basis points sequentially. Chewy credited this strength to its sponsored ads business, and more sales coming from higher-margin categories.

However, while gross margin was strong, operating expenses rose more than 7% year over year, with selling, general, and administration (SG&A) costs climbing 8%. Although it had 30 basis points of SG&A deleveraging, investors wanted to see more (changes in SG&A magnify revenue's impact on operating profit. High SG&A leverage can see large profit increases with a small sales increase, but also faces significant losses during downturns). Management said it still expects to deliver modest SG&A leverage this year, and that SG&A expense growth will moderate in the back half of the year.

Adjusted earnings per share (EPS), meanwhile, climbed nearly 38% year over year from $0.24 to $0.33, falling in line with guidance for $0.30 to $0.35. Adjusted EBITDA climbed 27% year over year to $183.2 million.

Chewy continues to generate solid free cash flow, coming in at $106 million for the quarter. It used that to help buy back $125 million in stock in the period. It ended the quarter with $591.8 million in cash and marketable securities, and no debt.

Looking ahead, Chewy forecasts fiscal Q3 revenue to grow by 7% to 8%, to $3.07 billion to $3.1 billion, with adjusted EPS of $0.28 to $0.33. It posted adjusted EPS of $0.20 a year ago. For the full year, the company upped its revenue guidance from between $12.3 billion and $12.45 billion to a new range of $12.5 billion to $12.6 billion. It kept its adjusted EBITDA margin guidance of 5.4% to 5.7%.

Despite the stock's reaction, Chewy is actually enjoying some really positive developments. Sales are growing nicely, and the autoship business continues to be a larger and larger part of its overall revenue pie. At the same time, it continues to grow its gross margin. Like Amazon and Walmart, it's experiencing nice growth in its high-margin sponsored ads business. It's also pushing a paid membership program that offers perks like free shipping and discounts, which both Amazon and Walmart have successfully used.

Like Costco Wholesale -- one retailer that has done really well with private brands -- Chewy is also moving further into private brands, which carry higher margins; it recently launched a new "healthy fresh dog food" brand called Get Real.

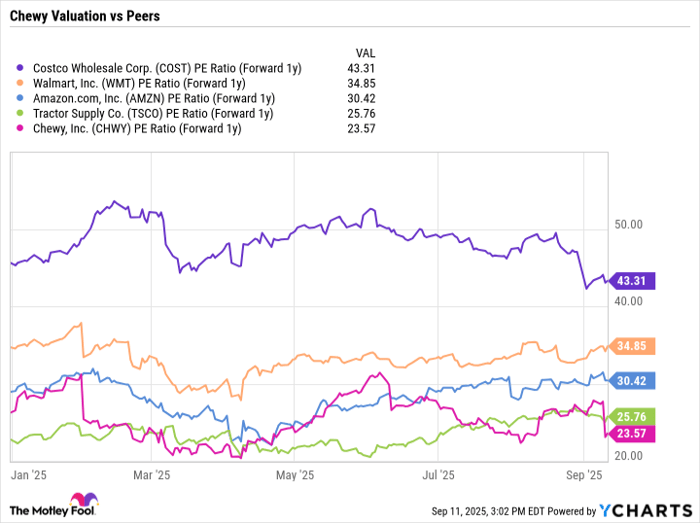

From a valuation perspective, Chewy stock currently trades at a forward price-to-earnings (P/E) ratio of around 23.5 based on next-year analyst estimates. That's a discount to other recession-resistant retailers such as Costco, Walmart, and Tractor Supply, as well as e-commerce giant Amazon:

Data by YCharts.

Overall, I don't think slightly elevated SG&A expenses should have caused the huge sell-off in Chewy's stock, given all the company's positives. In fact, cutting costs tends to be the easy part when running a business. The stock's valuation is attractive, as is the opportunity ahead. I think the recent price drop is a good buying opportunity, and that investors buying the dip will be rewarded.

Before you buy stock in Chewy, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Chewy wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $648,369!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,089,583!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 15, 2025

Geoffrey Seiler has positions in Chewy. The Motley Fool has positions in and recommends Amazon, Chewy, Costco Wholesale, Tractor Supply, and Walmart. The Motley Fool recommends the following options: short October 2025 $60 calls on Tractor Supply. The Motley Fool has a disclosure policy.

| Mar-27 | |

| Mar-27 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-24 | |

| Mar-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite