|

|

|

|

|||||

|

|

|

Executional challenges have weighed on the shares of this AI software company this year.

A sharp decline in its revenue and an organizational overhaul make this company a risky bet right now.

However, the generative AI software market is in its early phases of growth, and this company's solid balance sheet could come in handy in its bid to steady the ship.

Artificial intelligence (AI) turned out to be a massive growth driver in the past few years. Organizations and governments have been spending huge amounts of money on setting up AI infrastructure and integrating AI applications and tools into their business processes and operations to unlock the productivity gains that this technology can deliver.

However, not all companies have been able to make the most of the proliferation of AI. C3.ai (NYSE: AI) is one such name. Despite being in the business of selling enterprise AI software for quite some time now, C3.ai's business failed to take off.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Let's see why that is the case.

Image source: Getty Images.

Founded in 2009, C3.ai has undergone several pivots. From providing analytics and software solutions to energy companies, then expanding into the market for Internet of Things applications in enterprises and utilities, to finally rebranding as a provider of AI software solutions, it seems that C3.ai management has found it difficult to remain consistent over the years.

The company now offers generative AI software solutions, including an agentic AI platform and several industry-specific applications. It also allows its customers to develop custom applications. C3.ai has partnered with cloud computing giants Microsoft, Alphabet's Google, and Amazon to offer its solutions through their cloud computing platforms.

It gets a nice chunk of its business from these partners. For example, 40 of the 46 agreements it closed in the previous quarter were through the partner channel. Moreover, C3.ai management points out that it built a solid customer base that spans both commercial and federal customers. But these positives haven't really translated into solid growth for the company.

Its revenue in the first quarter of fiscal 2026 (which ended on July 31) dropped almost 20% year over year to $70.3 million. Uncharacteristically, C3.ai didn't provide full-year guidance. Moreover, its fiscal Q2 revenue guidance of $76 million points toward another year-over-year drop of 19%. C3.ai founder Thomas Siebel attributes the poor performance to a reorganization of the company's sales and service personnel.

Additionally, Siebel claims that his health issues kept him from participating actively in the sales process, and that may have had a negative impact on the company's performance. However, this is not the first time that C3.ai faced a disruption in its business.

It changed its business model from subscription-based to consumption-based three years ago. That pivot negatively impacted the company's growth trajectory. What's more, C3.ai expected to become profitable on a non-GAAP basis a couple of fiscal years ago, but it withdrew that guidance citing an increase in marketing-related spending and product development initiatives.

And now, C3.ai's decision to overhaul its sales and service operations and hire a new CEO suggests that it still struggles for consistency in its operations after all these years. So, despite operating in the booming AI software market (that's reportedly growing at an annual pace of almost 41%, according to IDC), C3.ai is failing to gain any traction.

Of course, management notes that the restructuring is now complete, but its outlook for the current quarter clearly indicates that it still needs time to get back on its feet.

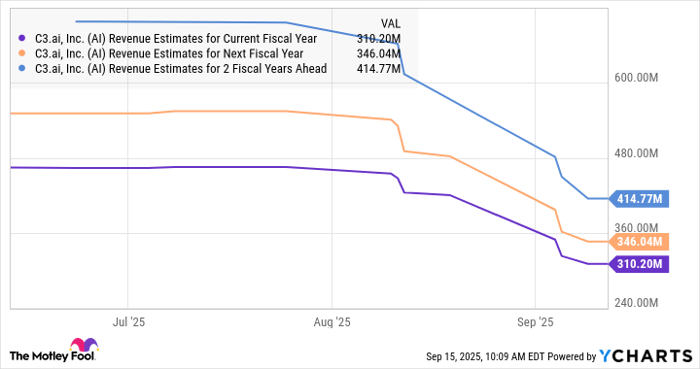

The story above suggests that C3.ai hasn't been able to build a cohesive growth strategy in all these years. Its financial performance is set to take a big beating this year, and not surprisingly, analysts have been forced to significantly reduce their growth expectations.

AI Revenue Estimates for Current Fiscal Year data by YCharts

As such, buying C3.ai stock right now doesn't look like a smart thing to do considering the troubled times that the company is facing. But at the same time, investors can consider adding the AI stock to their watch lists. That's because C3.ai's net cash position of around $650 million means that it has enough firepower to go on a marketing blitz, make an acquisition, or spend more on product development.

The generative AI software market is in its early phases of growth, so there is enough time for C3.ai to course correct and steady its ship. Investors would do well to keep an eye on this troubled stock considering the solid growth potential of the industry it operates in.

Before you buy stock in C3.ai, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and C3.ai wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $648,369!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,089,583!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 15, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, and Microsoft. The Motley Fool recommends C3.ai and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-09 | |

| Feb-08 | |

| Feb-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite