|

|

|

|

|||||

|

|

|

CommScope Holding Company, Inc. COMM is benefiting from healthy traction in the Access Network Solutions (“ANS”) segment. The company generated $322 million in revenues from ANS, up 65% year over year, beating the Zacks Consensus Estimate of $251.2 million. Adjusted EBITDA increased a staggering 132% year over year during the quarter.

The growth is primarily driven by the strong deployment of DOCSIS 4.0 amplifier and node products. Moreover, higher license sales also drove the top line. Growing usage of high data-intensive use cases such as cloud gaming, video conferencing and remote work is driving demand for high-capacity networks. Enterprises are rushing to upgrade their infrastructure from legacy DOCSIS 3.1 to advanced DOCSIS 4. CommScope is benefiting from this DOCSIS upgrade lifecycle.

In the DOCSIS amplifier business, the company benefited from Full Duplex deployment with Comcast. Extended Spectrum DOCSIS also secured several customer wins in the second quarter, including with Charter Communications.

The company’s virtual cable modem termination systems (“CMTS”) have also gained multiple customers in the second quarter. Management expects the healthy demand for its virtual CMTS to continue for the remainder of the year.

CommScope’s ANS segment faces competition from Cisco Systems Inc. CSCO and Harmonic Inc. HLIT. In the July quarter, Cisco’s networking revenues rose 12% year over year to $7.6 billion. Double-digit growth is driven by strength in webscale infrastructure, switching, enterprise routing, industrial IoT and servers. Network modernization and automation initiatives for the deployment of AI agents and applications are driving demand for Cisco’s solutions.

Harmonic ended the second quarter with $504.5 million of backlog and deferred revenues. Industry’s transition to DOCSIS 4 is expected to be a major growth driver for the company. Recently, GCI, Alaska’s largest telecommunication company, has selected Harmonic to upgrade its DOCSIS network infrastructure. HLIT’s growing traction in this vertical can pose a threat to CommScope’s competitive edge.

CommScope’s shares have gained 188.1% in the past year compared with the industry’s growth of 93.6%.

From a valuation standpoint, the company’s shares currently trade at 0.63 forward sales, lower than 0.94 for the industry.

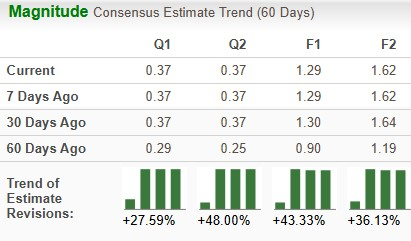

Earnings estimates for 2025 and 2026 have improved over the past 60 days.

COMM currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-01 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite