|

|

|

|

|||||

|

|

|

Sweetgreen and Figma are both underperforming the broader stock market.

Sweetgreen is facing steep, same-store sales declines amid a tough economic backdrop.

Figma is growing briskly, but the stock's valuation is sky-high.

While the major stock indices are carving out new, all-time highs, some stocks are struggling. Salad chain Sweetgreen (NYSE: SG) and software company Figma (NYSE: FIG) have both tumbled recently. The former is facing serious growth challenges, while the latter is saddled with an extreme valuation. While some investors may view these steep declines as buying opportunities, both stocks look risky and could continue to head lower.

Image source: Getty Images.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Consumers have a lot of choices when it comes to fast-casual lunch options. Sweetgreen, a purveyor of pricey salads, seems to be losing out to the competition.

Sweetgreen grew revenue during the second quarter, but just barely, and only because it continues to open new restaurants. Same-store sales plunged 7.6% year over year, driven by a 10.1% decline in traffic. Menu price increases could be partly to blame in addition to the macroeconomic environment.

For the full year, Sweetgreen now expects same-store sales to drop by 4% to 6%. Previously, the company had guided for flat same-store sales in 2025. Sweetgreen will still open at least 40 new restaurants, which will help offset the same-store sales decline to a degree. Full-year revenue is now expected in a range of $700 million to $715 million, down from previous guidance of $740 million to $760 million.

Sweetgreen stock has plummeted nearly 80% from its 52-week high. Even after that decline, the valuation isn't all that attractive. Sweetgreen is still valued at around $1.05 billion, which works out to be roughly 1.5 times the company's revenue guidance. Sweetgreen isn't profitable, reporting net loss of $23 million in Q2, and restaurant-level profitability is crashing amid slumping sales.

Sweetgreen is unlikely to be the kind of restaurant chain that does well in a deteriorating economy marked by inflation worries, sinking consumer sentiment, and a rough jobs market. There are too many similar options, and many of them offer better value than the salad chain. While Sweetgreen stock has already been put through the wringer, the rout may not be over as the restaurant chain struggles with tumbling sales.

Recent software IPO Figma initially surged after going public, but the stock has since cooled off considerably. From its peak, shares of Figma have dropped more than 50%.

Figma's results have been solid. The company, which specializes in design software, reported 41% year-over-year revenue growth in Q2. The net dollar retention rate, which measures how quickly existing customers are expanding spending, was an impressive 129% for customers spending at least $10,000 annually. Figma is also already profitable on a generally accepted accounting principles (GAAP) basis, with a positive operating income in Q2.

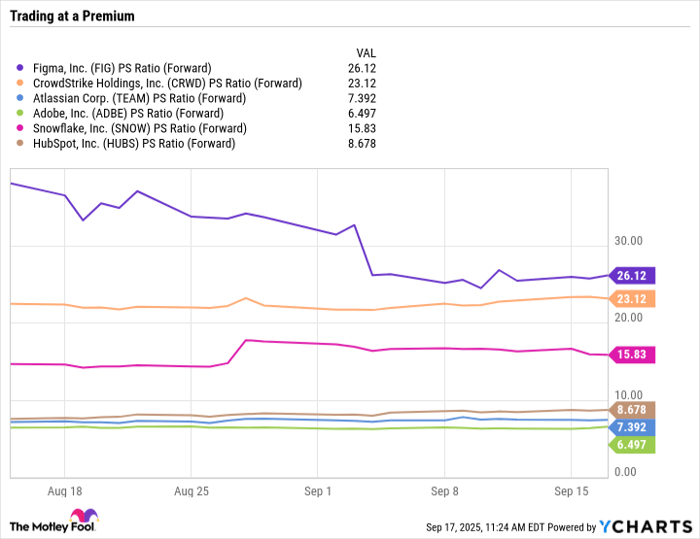

What makes Figma stock risky even after its steep decline is the valuation. Figma expects to generate as much as $1.025 billion in revenue for the full year, which puts the price-to-sales ratio above 25. That's down from the astronomical levels touched soon after the initial public offering (IPO), but it's still in nosebleed territory, and it's pricier than many other software-as-a-service stocks.

FIG PS Ratio (Forward) data by YCharts.

Figma expects strong revenue growth to continue for the rest of the year, but given the uncertain economic environment, growth could deteriorate if businesses pull back on non-essential spending. Any slowdown could send shares of Figma tumbling and bring the valuation back to earth.

Before you buy stock in Sweetgreen, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sweetgreen wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $647,425!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,071,739!*

Now, it’s worth noting Stock Advisor’s total average return is 1,056% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 15, 2025

Annie Dean, a Vice President at Atlassian, is a member of The Motley Fool's board of directors. Timothy Green has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe, Atlassian, CrowdStrike, HubSpot, and Snowflake. The Motley Fool recommends Sweetgreen. The Motley Fool has a disclosure policy.

| 8 hours | |

| 9 hours | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-06 | |

| Feb-06 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite