|

|

|

|

|||||

|

|

|

Mortgage rates continue to ease, with the average 30-year fixed rate sliding to 6.26% in the week ended Sept. 18, 2025, according to the data from FreddieMac's report. This is the lowest rate since the same week in October 2024, when it was 6.32%. The drop reflects a decline in long-term U.S. Treasury yields and the Federal Reserve's 25-basis-point rate cut.

With the decline in mortgage rates, origination volume and refinancing activity are increasing. Per the MBA report, mortgage loan application volume increased 43% last week from the prior week, while the refinancing index jumped 58% last week.

These favorable trends create a constructive backdrop for mortgage REIT (mREIT) investors. Stocks such as Ellington Financial EFC, Annaly Capital Management NLY and Orchid Island Capital ORC stand out as potential beneficiaries of rising origination and refinancing volumes.

With the Fed signaling two additional rate cuts by the end of 2025, mortgage rates are expected to decline further. This favorable backdrop is poised to benefit mREITs, as tighter spreads in the Agency market should lift asset prices and drive book value growth in the near term. Lower rates will also help ease operational and funding pressures, boosting gain-on-sale margins and supporting new investment activity.

As net interest spreads expand, mREITs like EFC, ORC and NLY can see stronger profitability and improved capacity to increase dividend payouts, making them especially attractive to income-focused investors.

Ellington Financial invests in a diverse array of financial assets. These include residential and commercial mortgage loans and mortgage-backed securities, consumer loans and asset-backed securities.

EFC is well-positioned to weather volatility in the mortgage market, supported by its diversified exposure across residential and commercial mortgage loan portfolios and strong momentum in its securitization platform. The company’s loan originations, especially in commercial mortgage bridge loans, proprietary reverse mortgages, and closed-end second lien loans, continue to contribute to stable growth and income.

To navigate market uncertainty, Ellington Financial is actively leveraging dynamic hedging strategies, maintaining a broad and balanced portfolio, securing multiple sources of financing, and operating with low leverage. These measures reflect a disciplined approach to risk management and a commitment to preserving book value while adapting to shifting market conditions.

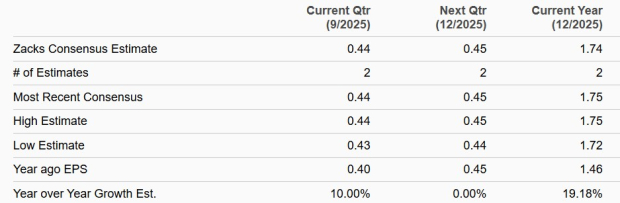

The company’s 2025 earnings estimates have been unchanged at $1.74 per share over the past month, indicating year-over-year growth of 19.2%. EFC sports a Zacks Rank of #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Earnings Estimates

Annaly’s strength lies in its diversified investment strategy, spanning residential credit, mortgage servicing rights (MSRs) and Agency mortgage-backed securities (MBS). This approach helps reduce volatility and interest rate sensitivity while targeting attractive risk-adjusted returns.

As of June 30, 2025, NLY managed an $89.5-billion portfolio, with $79.5 billion in liquid Agency assets. The company is also expanding its MSR business, which serves as a hedge against rising rates by gaining value when prepayments slow. By balancing Agency MBS with MSRs, it enhances yield, mitigates risks and positions itself for more stable long-term performance across rate cycles.

Given relatively lower mortgage rates, in the first half of 2025, the company’s NII increased to $493.2 million from $47.1 million in the same period a year ago. With improving purchase originations and refinancing, Annaly is positioned for book value gains as tighter Agency spreads lift asset prices. A wider net interest spread should also enhance portfolio yields, supporting stronger financial performance ahead.

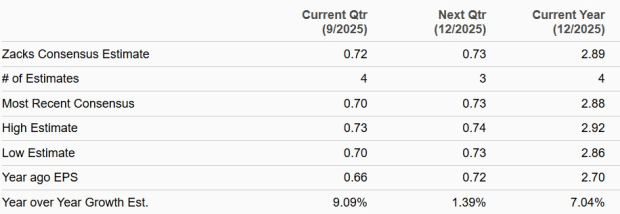

The company’s 2025 earnings estimates have been unchanged at $2.89 per share over the past month, indicating year-over-year growth of 7%. NLY has a Zacks Rank of #3 (Hold) at present.

Earnings Estimates

Orchid has maintained its focus on Agency residential mortgage-backed securities (RMBS), an investment strategy that has positioned it as one of the strong players in this specialized market segment.

ORC is doubling down on its core strategy of investing in Agency RMBS, targeting two key segments: traditional pass-through Agency RMBS—including mortgage pass-through certificates and collateralized mortgage obligations backed by Fannie Mae, Freddie Mac, or Ginnie Mae—and structured Agency RMBS.

Moreover, Agency RMBS will continue to offer a compelling return opportunity for the company. Although the market is highly competitive, Orchid's focus on Agency RMBS puts it in a position to profit from favorable trends, while execution will be crucial to achieving these.

In the first half of 2025, Orchid’s NII rose to $42.9 million against net interest expenses of $3.2 million in the year-ago period. Given a favorable mortgage rate environment, the company’s NII is likely to improve further in the upcoming period.

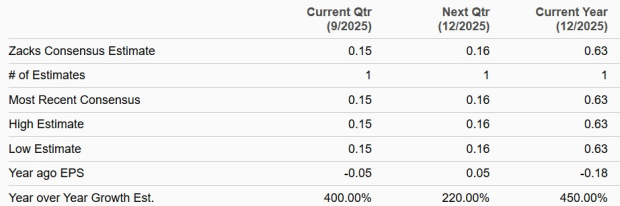

The company’s 2025 earnings estimates have been unchanged at 63 cents per share over the past month, indicating a year-over-year upsurge of 450%. ORC has a Zacks Rank of #3 at present.

Earnings Estimates

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite