|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Lamb Weston Holdings, Inc. LW posted results for the third quarter of fiscal 2025, with the top and the bottom lines surpassing the Zacks Consensus Estimate. Quarterly earnings declined year over year while sales increased from the year-ago quarter’s level. The company reported improved volume trends while gaining from cost efficiencies and operational improvements.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

LW’s bottom line came in at $1.10 per share, surpassing the Zacks Consensus Estimate of 87 cents. The metric declined 8% due to a drop in adjusted gross profit, influenced by a higher effective tax rate and increased interest expenses. However, these impacts were partially offset by a reduction in adjusted SG&A expenses.

Net sales amounted to $1,520.5 million, surpassing the Zacks Consensus Estimate of $1,500.1 million. The top line increased 4% year over year.

The company continues to achieve savings from its Restructuring Plan while navigating challenges from soft restaurant traffic. Management reaffirmed its fiscal 2025 outlook and remains focused on cost optimization and strategic investments. The company is working with AlixPartners, a leading global business advisory firm, to aid in evaluating opportunities for near- and long-term value creation and cost savings.

Lamb Weston price-consensus-eps-surprise-chart | Lamb Weston Quote

Lamb Weston’s fiscal third-quarter volume rose 9% compared to the same quarter last year, successfully replacing the lost volume from regional, small and retail customers driven by its transition to a new ERP system. In addition, the company secured new customer contracts across various channels and geographic regions, balancing out volume losses stemming from weak global restaurant traffic trends. Our model suggested a volume increase of 8.6% in the quarter.

However, the price/mix dipped 5% due to strategic pricing adjustments aimed at staying competitive in both North America and international markets. We expected the price/mix to decline 2.9% in the quarter.

The adjusted gross profit decreased by $6.6 million, reaching $420.4 million. This decline was mainly caused by a negative price/mix, increased transportation and warehousing costs resulting from higher warehouse inventories, and a $16.2 million rise in depreciation expenses related to recent capacity expansions across the Netherlands and the United States. However, the impact was partially offset by increased sales volumes and reduced manufacturing costs per pound.

Adjusted selling, general and administrative (SG&A) expenses fell $7.2 million year over year, totaling $157.2 million, associated with the lapping of increased expenses related to the ERP transition in the prior-year quarter and cost savings from the Restructuring Plan and other management initiatives to reduce costs. These were somewhat offset by timing of compensation and benefit accruals.

Adjusted EBITDA rose by $20.2 million year over year, reaching $363.8 million. This growth was driven by increased net sales and reduced Adjusted SG&A expenses, partially offset by a decline in Adjusted Gross Profit.

Net sales for the North America segment, which covers customers in the United States, Canada and Mexico, grew by 4%, reaching $986.3 million compared to the prior-year quarter. Sales volume rose 8% as the company successfully replaced lost regional, small and retail customer volume from the previous year’s ERP transition. In addition, new customer contract wins across multiple channels helped drive growth. The price/mix fell by 4% due to strategic price and trade investments, partially offset by a favorable channel and product mix. The North America segment’s Adjusted EBITDA rose by $14.8 million to $300.7 million.

Net sales for the International segment, which includes all customers outside North America, grew 5% to $534.2 million. Despite weak restaurant traffic, volume rose 12%, driven by key chain customer contract wins in international markets, among other reasons. However, these gains were partially offset by the impact of the company’s strategic decision to exit lower-priced, lower-margin business in Europe to optimize its customer and product mix. The price/mix declined by 7% due to competitive pricing adjustments in key international markets and unfavorable foreign currency fluctuations. International segment Adjusted EBITDA fell by $8.5 million to $93.2 million.

The company ended the quarter with cash and cash equivalents of $67.5 million, long-term debt and financing obligations (excluding the current portion) of $3,680.6 million and total shareholders’ equity of $1,633.6 million.

The company generated $485.3 million as net cash from operating activities for the 39 weeks ending Feb. 23, 2025, wherein capital expenditures amounted to $563.1 million.

In the third quarter of fiscal 2025, Lamb Weston returned $151.4 million to its shareholders through cash dividends and share repurchases. This includes $51.4 million in cash dividends and $100 million in share repurchases, with 1,559,369 shares repurchased under the company’s buyback program.

In addition, the company increased the share repurchase authorization by $250 million, bringing the total authorization to $750 million, with almost $458 million worth of shares available for repurchases.

Lamb Weston also declared a quarterly dividend of 37 cents per share, payable on May 30, 2025, to its stockholders of record as of May 2, 2025.

The company still expects its annual net sales target range to be $6.35-$6.45 billion. Lamb Weston envisions an adjusted EBITDA target range from $1.17 billion to $1.21 billion. The company still expects its adjusted net income guidance to be $440-$460 million, with adjusted earnings per share (EPS) anticipated to be in the range of $3.05-$3.20.

Lamb Weston now anticipates adjusted SG&A to be in the range of $665 million to $675 million, down from $680 million to $690 million expected earlier. Depreciation and amortization expenses are expected to be around $375 million, with an effective tax rate of approximately 28% for fiscal 2025.

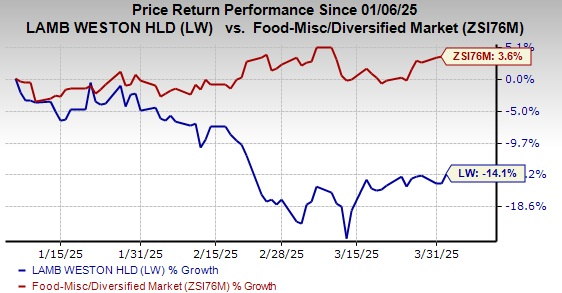

Shares of this Zacks Rank #4 (Sell) company have lost 14.1% in the past three months against the industry’s 3.6% growth.

Pilgrim’s Pride PPC, which produces, processes, markets and distributes fresh, frozen and value-added chicken and pork products, currently carries a Zacks Rank of 2 (Buy). PPC delivered a positive earnings surprise of 25.7% in the trailing four quarters, on average. You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

The Zacks Consensus Estimate for Pilgrim’s Pride’s current financial-year earnings indicates a decline of 2.6% from the prior-year reported level.

Utz Brands UTZ, which has a diverse portfolio of salty snacks, currently carries a Zacks Rank of 2. UTZ has a trailing four-quarter earnings surprise of 8.8%, on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year sales and earnings indicates growth of 1.2% and 10.4%, respectively, from the year-ago numbers.

United Natural Foods, Inc. UNFI distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. It currently carries a Zacks Rank of 2. UNFI delivered a trailing four-quarter earnings surprise of 408.7%, on average.

The consensus estimate for United Natural Foods’ current financial-year sales and earnings implies growth of 1.9% and 485.7%, respectively, from the year-ago figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-15 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite