|

|

|

|

|||||

|

|

|

Shares of Arthur J. Gallagher & Co. AJG are trading at a discount compared with the Zacks Insurance - Brokerage industry. Its price-to-book value of 3.3X is lower than the industry average of 4.16X.

Shares of other insurers like Brown & Brown, Inc. BRO and Willis Towers Watson Public Limited Company WTW are also trading at lower multiples than the industry average, while Marsh & McLennan Companies, Inc. MMC is trading at a premium.

Shares of Arthur J. Gallagher have gained 5.1% year to date against the industry’s decline of 18.1%. The Finance sector and the Zacks S&P 500 Composite have rallied 17.6% and 16.9%, respectively, in the same time frame.

The insurer has a market capitalization of $76.1 billion. The average volume of shares traded in the last three months was 1.5 million.

The Zacks Consensus Estimate for 2025 revenues is pegged at $13.7 billion, implying a year-over-year improvement of 20.8%. The consensus estimate for AJG’s current-year earnings is pegged at $10.98 per share, suggesting an 8.8% rise from the year-ago reported figure. The consensus estimate for 2026 earnings per share and revenues indicates increases of 23.2% and 22.8%, respectively, from the 2025 estimates.

The Zacks Consensus Estimate for 2025 earnings has been flat over the past month while that of 2026 has moved up 0.2% in the past month.

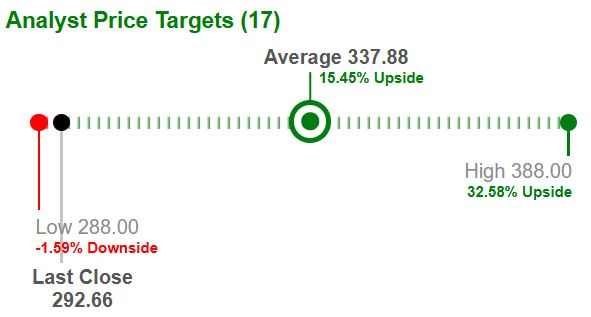

Based on short-term price targets offered by 17 analysts, the Zacks average price target is $337.88 per share. The average indicates a potential 15.5% upside from the last closing price.

Arthur J. Gallagher is steadily advancing its growth journey, supported by strong operations, high client retention and rising renewal premiums. These core strengths form the backbone of its organic momentum, ensuring consistent progress. Complementing this, AJG continues to make selective acquisitions that reinforce its long-term expansion.

Building on this foundation, growth in the Brokerage and Risk Management segments has been a key organic driver. Solid client retention, rising renewal premiums and stronger customer activity are contributing to steady momentum across geographies and product lines.

The Risk Management segment is benefiting from increased business activity and higher claim volumes, while the Brokerage arm continues to deliver consistent expansion. With these strengths in place, the company expects organic growth of 6-8% for 2025, backed by disciplined execution and resilient demand across its core businesses.

Alongside its organic momentum, the company continues to strengthen growth through acquisitions, completing nine deals in the second quarter of 2025 alone. These transactions are expected to contribute about $290 million to annualized revenues, highlighting the impacts of its strategic expansion. International operations already account for nearly one-third of total revenues, and the company expects this share to increase further as non-U.S. acquisitions gain scale.

Despite the solid growth drivers, escalating expenses have begun to put pressure on profitability. Higher compensation, depreciation, amortization and operating costs have been the key factors weighing on margins. As a result, in the second quarter of 2025, the net earnings margin (before reimbursements) slipped to 10.9% from 13.3% a year earlier.

Rising debt levels have also emerged as a headwind for the company. Total debt reached $13 billion as of June 30, 2025, leading to higher interest expenses. While the debt-to-capital ratio of 35.9% remains below the industry average of 50.1%, the times interest earned ratio of 5.07 trails the industry benchmark of 6.1.

In addition, the company’s returns indicate challenges in effectively managing shareholders’ funds. Return on invested capital stands at 7.34%, below the industry average of 8.49%, while return on equity is 13.17%, well under the industry average of 24.67%. These figures highlight the company’s inefficiency in utilizing shareholders’ funds.

AJG continues to emphasize shareholder value creation through steady capital returns. The company has increased its dividend five times over the past five years, resulting in a five-year annualized growth rate of 7.9%, with a current payout ratio of 25%. The company may also pursue share repurchases in 2025 if surplus cash is available after financing acquisition activities.

Overall, Arthur J. Gallagher benefits from strong organic growth, solid client retention and a steady contribution from strategic acquisitions, supporting consistent expansion. However, rising expenses, elevated debt and relatively low returns on capital highlight challenges that may weigh on profitability.

Ongoing headwinds limit meaningful upside for AJG. It is therefore wise to adopt a wait-and-see approach on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-27 | |

| Mar-24 | |

| Mar-24 | |

| Mar-23 | |

| Mar-23 | |

| Mar-22 | |

| Mar-20 | |

| Mar-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite