|

|

|

|

|||||

|

|

|

Shares of Comerica Incorporated CMA have gained 21.8% in the past three months, outperforming the industry’s growth of 13.9%. The company also outperformed its closed peers such as BankUnited, Inc. BKU and Northern Trust Corporation NTRS over the same time frame.

After such a strong rally, investors are left wondering whether CMA stock is worth considering now. Let’s find out.

Fed Rate Cuts to Aid NII: On Sept. 17, 2025, the Federal Reserve reduced its benchmark interest rate by 25 basis points to 4.00%–4.25% and indicated the possibility of two more cuts before year-end. The lower interest rates typically ease deposit and funding costs, supporting net interest income (NII) and margins for banks such as Comerica, BankUnited, and Northern Trust.

Comerica’s NII has improved steadily, registering a five-year compound annual growth rate (CAGR) of 2.8% (ended 2024). Further, net interest margin (NIM) also expanded consistently till 2023 before moderating in 2024. Encouragingly, both NII and NIM increased in the first half of 2025.

The company’s NII is expected to continue expanding given relatively lower rates. Management anticipates full-year 2025 NII to rise 5–7% from 2024 levels.

Loan Growth: The company has shown steady loan growth over the past few years. Its total loans witnessed a five-year CAGR of nearly 1% (ended 2024). As of June 30, 2025, loans stood at $51.2 billion.

Though the trend reversed in the first half of 2025, comparatively lower interest rates, along with a robust loan pipeline, are expected to support growth in the coming quarters. For the third quarter of 2025, management expects average loans to edge higher from the $50.7 billion reported in the second quarter.

Solid Liquidity Profile: CMA remains well-positioned with strong liquidity levels and favorable debt capacity. As of June 30, 2025, total debt (including short-term borrowings and medium- to long-term debt) stood at $8.7 billion, while total liquidity capacity was $40.5 billion.

The company also had a remaining borrowing capacity of $17.4 billion under the discount window. Thus, decent cash levels, favorable borrowing capacity and a staggered debt maturity profile offer it decent financial flexibility, making the debt repayments seem manageable.

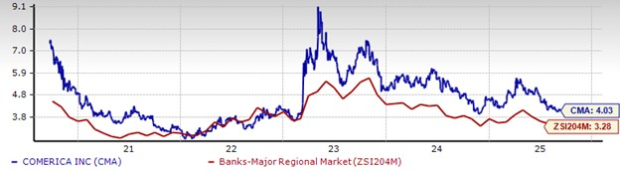

Impressive Capital Distribution Plan: Comerica has been enhancing shareholder value by paying steady dividends and actively repurchasing shares. The company has raised its dividend once in the past five years, with a payout ratio of about 54% of earnings. It has a dividend yield of 4.03% higher than the industry’s average of 3.28%. Notably, the dividend yield of its competitors, BankUnited and Northern Trust, is 3.18% and 2.43%, respectively.

Apart from dividends, Comerica has an active share repurchase program in place. Since launching its share repurchase program in 2010, the bank has been authorized to repurchase 97.2 million shares. In November 2024, it approved an additional authorization of about 10 million shares, bringing the cumulative total to 107.2 million shares, with no expiration date. As of June 30, 2025, 10.9 million shares remained available for repurchase. Management has outlined plans to buy back 1.5 million shares in the third quarter of 2025. Supported by decent earnings strength, capital strength and solid liquidity levels, capital distribution activities seem sustainable.

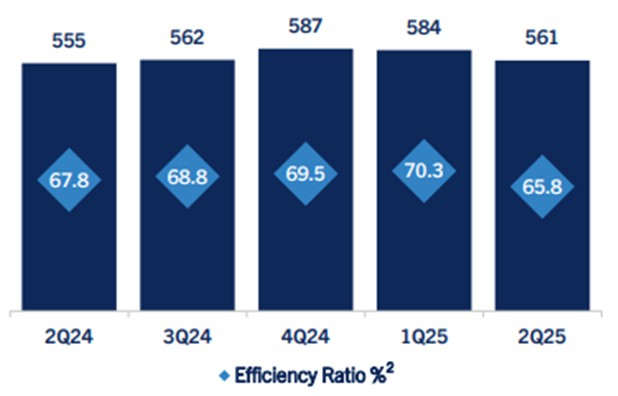

Operational Efficiency Measures: The company continues to take steps to streamline operations and improve efficiency, which will support long-term profitability. Comerica has focused on improving efficiency by closing banking centers, realigning facilities, streamlining managerial layers, and eliminating positions. Its efficiency ratio improved to 65.8% in the second quarter of 2025 from 67.8% in the prior-year quarter, reflecting better cost control and higher profitability.

The company is also investing in product enhancements, customer analytics and training to boost its revenues. These initiatives are expected to lower costs over time and enhance return on equity.

Elevated Expenses: Comerica’s non-interest expenses have been on the rise, recording a CAGR of 5.3% over the last five years (2019–2024).

While expenses declined in the first half of 2025, management expects third-quarter expenses to rise due to higher compensation and benefits. This is likely to hurt bottom-line growth in the near term.

Lack of Loan Portfolio Diversification: Heavy exposure to commercial and real estate loans leaves the bank vulnerable to concentration risks. As of June 30, 2025, commercial and commercial mortgage loans accounted for 81.2% of total loans.

This high concentration exposes the company to risks from the rapidly changing macroeconomic backdrop and weakness in commercial lending.

Comerica’s solid liquidity position, steady NII growth and strong capital return policy are expected to support its financial performance in the coming quarters. Ongoing efficiency initiatives, together with reinvestments in consumer analytics and product enhancements, are expected to support long-term profitability.

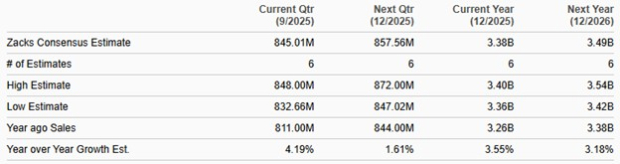

The Zacks Consensus Estimate for Comerica’s 2025 and 2026 sales implies year-over-year growth of 3.55% and 3.18%, respectively.

However, elevated expenses and heavy exposure to commercial lending remain near-term challenges.

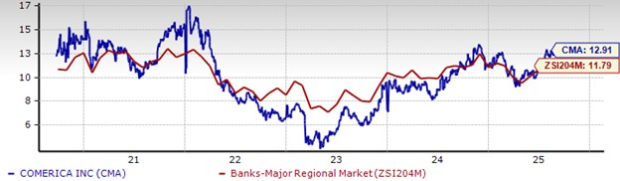

Additionally, from a valuation standpoint, the company appears to be expensive relative to the industry. It is currently trading at a premium with a forward 12-month price-to-earnings (P/E) multiple of 12.91X, above the industry average of 11.79X. Meanwhile, the P/E ratios of its peers, BankUnited and Northern Trust, are 11.47 and 14.47, respectively.

Given these factors, new investors should avoid initiating positions at current prices and wait for a more attractive entry point. The company currently carries a Zacks Rank #3 (Hold). You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-13 | |

| Jul-13 | |

| Jul-07 | |

| Jul-06 | |

| Jun-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite