|

|

|

|

|||||

|

|

|

Over the past six months, Snap’s stock price fell to $8.61. Shareholders have lost 9.7% of their capital, which is disappointing considering the S&P 500 has climbed by 16.2%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Snap, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Despite the more favorable entry price, we're swiping left on Snap for now. Here are three reasons there are better opportunities than SNAP and a stock we'd rather own.

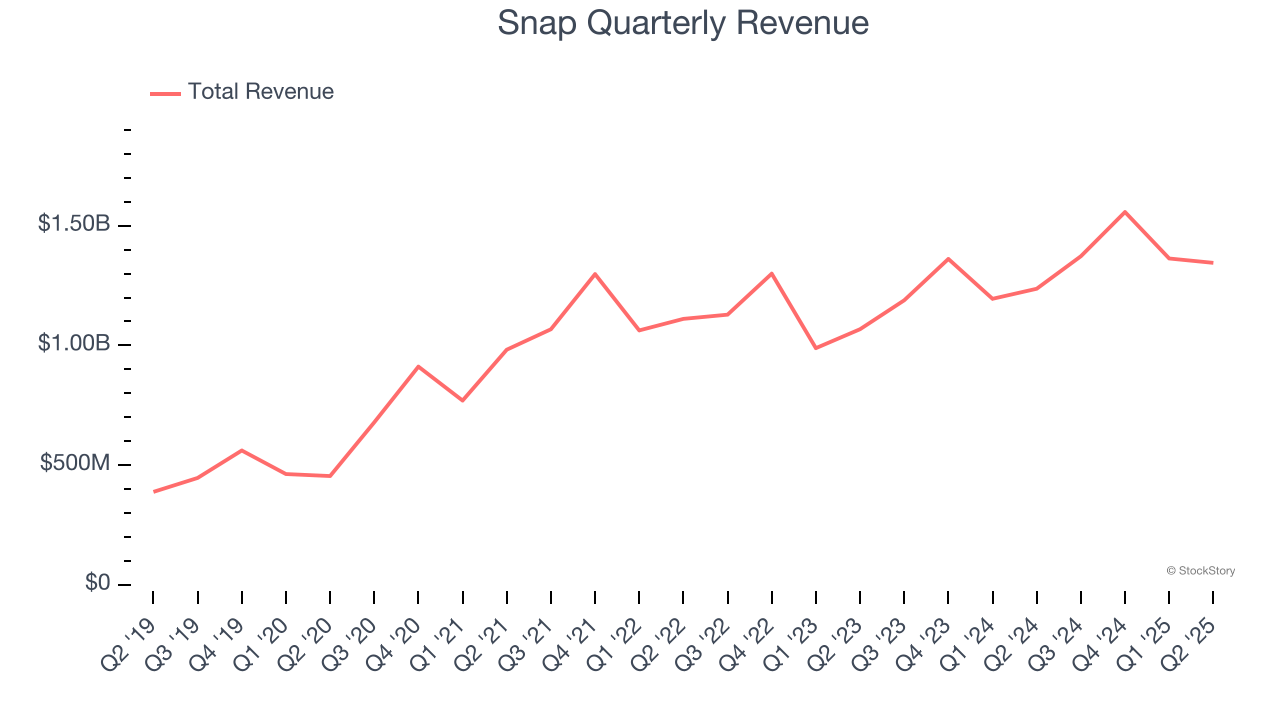

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Snap grew its sales at a tepid 7.5% compounded annual growth rate. This fell short of our benchmark for the consumer internet sector.

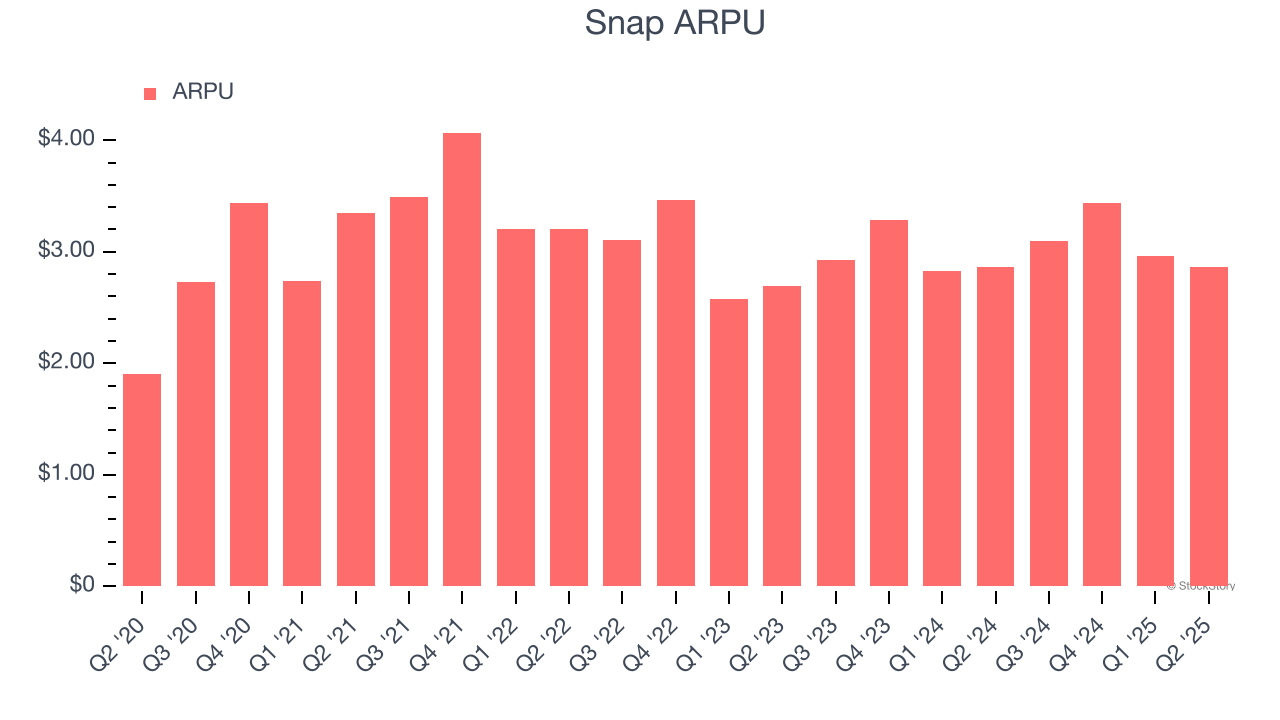

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Snap’s audience and its ad-targeting capabilities.

Snap’s ARPU growth has been subpar over the last two years, averaging 2.6%. This isn’t great, but the increase in daily active users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Snap tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

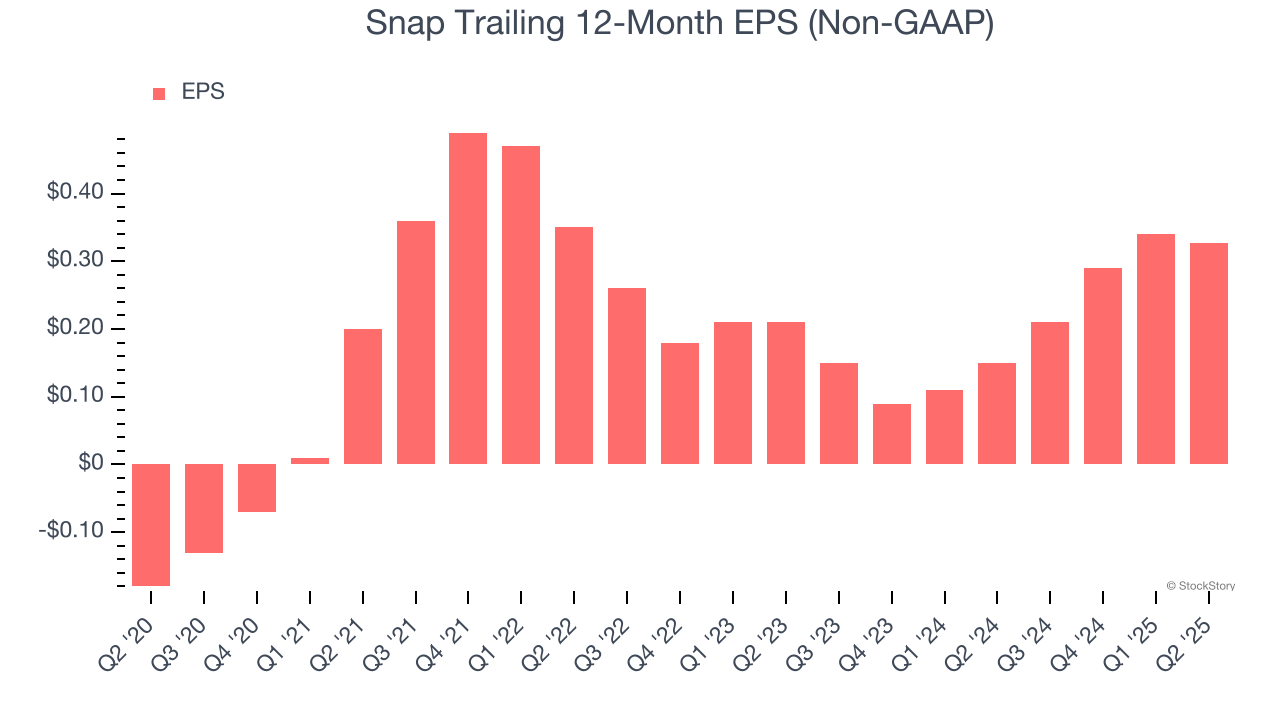

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Snap, its EPS declined by 2.3% annually over the last three years while its revenue grew by 7.5%. This tells us the company became less profitable on a per-share basis as it expanded.

Snap isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 22.9× forward EV/EBITDA (or $8.61 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d suggest looking at the most entrenched endpoint security platform on the market.

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 1 hour | |

| 1 hour | |

| 3 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours | |

| 11 hours | |

| 11 hours | |

| 15 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite