|

|

|

|

|||||

|

|

|

Even though Barrett (currently trading at $45.35 per share) has gained 9.1% over the last six months, it has lagged the S&P 500’s 15.5% return during that period. This might have investors contemplating their next move.

Is there a buying opportunity in Barrett, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We're swiping left on Barrett for now. Here are three reasons why BBSI doesn't excite us and a stock we'd rather own.

With $1.20 billion in revenue over the past 12 months, Barrett is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

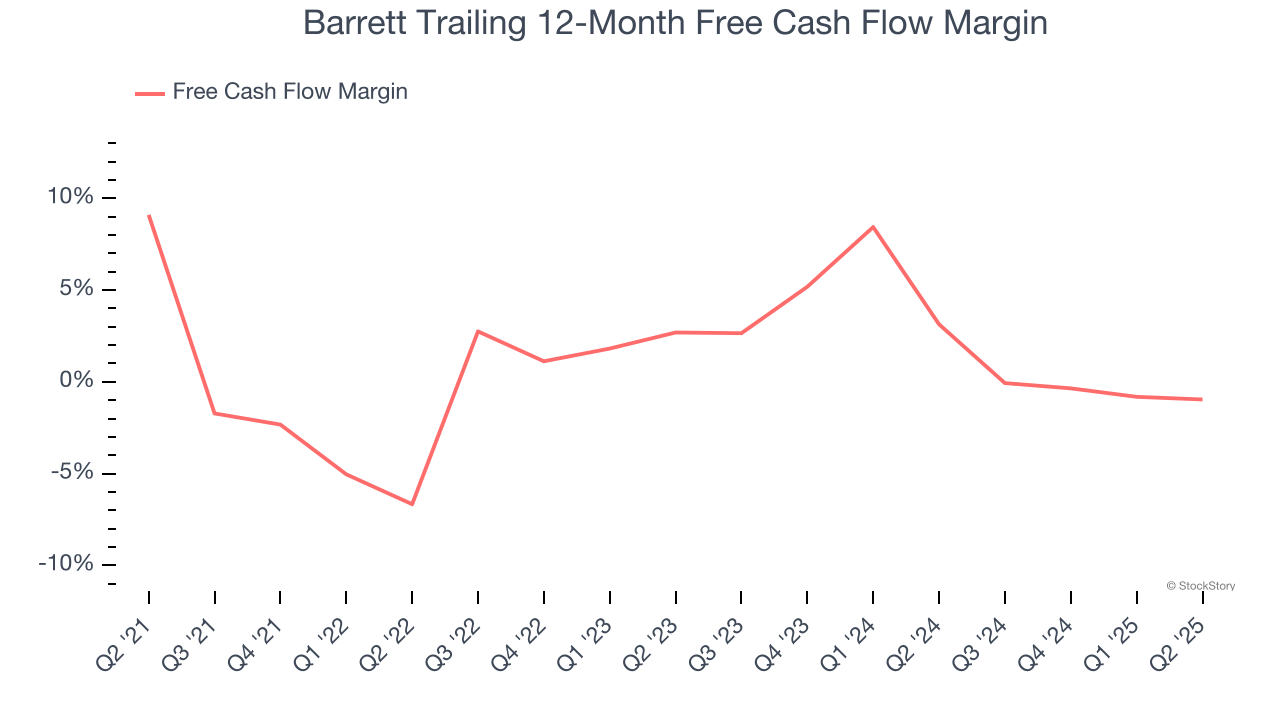

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Barrett’s margin dropped by 10.1 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business. Barrett’s free cash flow margin for the trailing 12 months was breakeven.

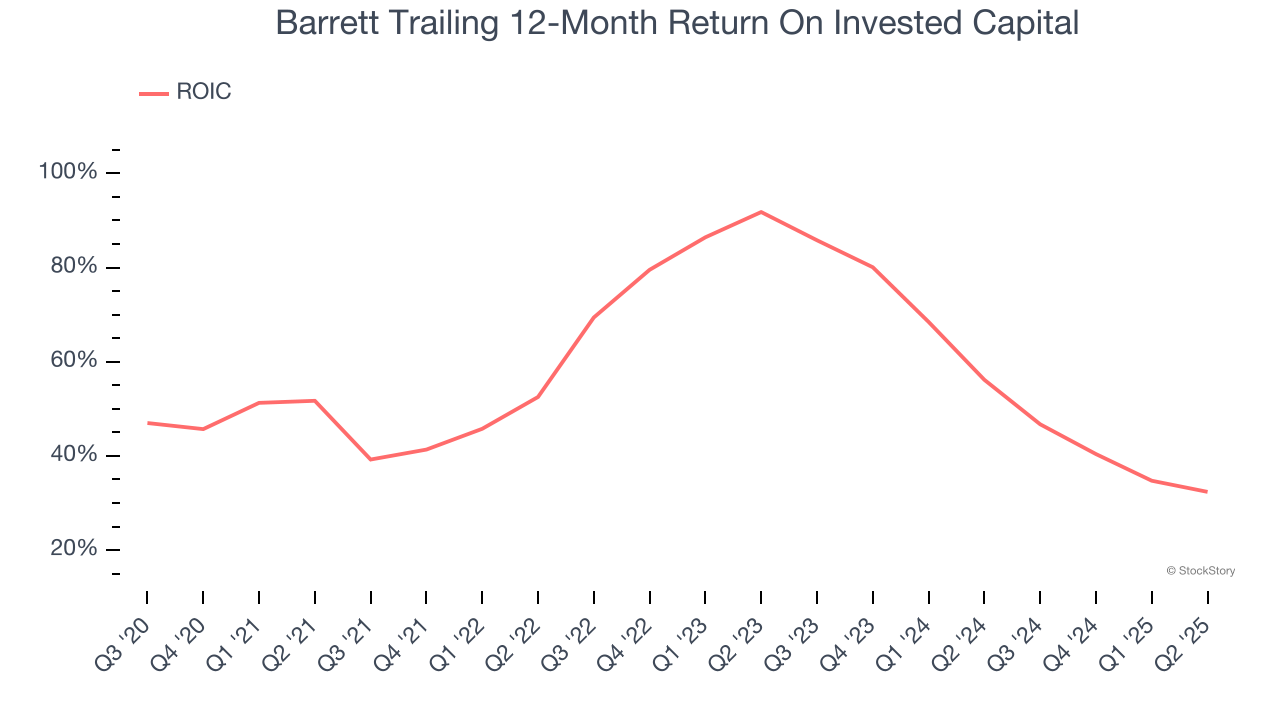

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Barrett’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Barrett isn’t a terrible business, but it isn’t one of our picks. With its shares underperforming the market lately, the stock trades at 19.6× forward P/E (or $45.35 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Jul-22 | |

| May-06 | |

| May-06 | |

| Apr-28 | |

| Apr-22 | |

| Mar-11 | |

| Mar-03 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite