|

|

|

|

|||||

|

|

|

The United States’ homebuilding market has been experiencing choppy weather for the past few years, which is directly hampering the profitability scale for operating homebuilders, such as D.R. Horton, Inc. DHI. Due to the ongoing affordability concerns among homebuyers, the high mortgage rate scenario is pulling back the home delivery numbers and new home orders for the company. In the first nine months of fiscal 2025, DHI’s home closings were down year over year by 6.9% to 61,495 units, with net sales orders tumbling 6.2% to 63,345 units.

To counter the declining numbers, D.R. Horton has been offering several sales incentives to its customers. The major traffic driver incentive option is the 3.99% FHA (Federal Housing Administration) loan offered by the company’s affiliate lender, DHI Mortgage. Per the third quarter of fiscal 2025, DHI highlighted that, owing to this loan program, alongside other incentive offerings, customers’ confidence in their products is expected to have inched up. For the fourth quarter of fiscal 2025, the company expects home closings to be between 23,500 and 24,000 units compared with 23,647 units closed a year ago.

However, the increased incentive offerings are eroding the margin scale for D.R. Horton, which is expected to have an adverse impact in the long term if this trend continues. Moreover, even with increased incentive offerings, the sales volume is not moving up, but rather diminishing. It is because the housing market weakness and the newly added tariff uncertainties are weighing heavily on DHI’s in-house efforts. The company’s fiscal fourth quarter’s home sales gross margin outlook substantiates this scenario.

For the fourth quarter of fiscal 2025, D.R. Horton expects home sales gross margin to range between 21% and 21.5%, which is down 23.6% year over year and 21.8% sequentially. The company’s expectations reflect the current housing market scenario, which is far from reaching a normalization state any time soon.

The ongoing weakness in the U.S. housing market is not only hitting D.R. Horton but also other key homebuilders of the market, including PulteGroup, Inc. PHM and Toll Brothers, Inc. TOL. With mortgage rates hovering near multi-decade highs and affordability stretched, the demand for new homes has slowed, pressuring volumes and margins for PulteGroup, Toll Brothers and D.R. Horton.

PulteGroup, with a more balanced portfolio across price points, is seeing moderation in buyer traffic and cancellations, while its profitability remains under pressure from elevated incentives. Toll Brothers, more concentrated in the luxury segment, has benefited from higher-income buyers’ relative resilience, though even this cohort is showing signs of caution amid economic uncertainty.

Meanwhile, supply-chain normalization is helping all three manage costs, but slower absorption rates weigh on community growth plans. In this environment, D.R. Horton’s scale advantage remains a differentiator, while PulteGroup emphasizes operational discipline and Toll Brothers leans on its luxury niche.

Shares of this Texas-based homebuilder have trended upward 28.2% in the past three months, outperforming the Zacks Building Products - Home Builders industry, the broader Zacks Construction sector and the S&P 500 Index.

DHI stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 13.7, as evidenced by the chart below. The overvaluation of the stock compared with its industry peers indicates its strong potential in the market, given the favorable trends backing it up.

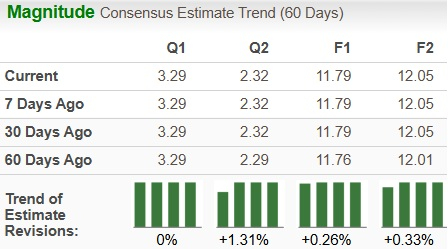

For fiscal 2025 and fiscal 2026, DHI’s earnings estimates have trended upward in the past 60 days. The revised estimated figure for fiscal 2025 implies a year-over-year decline of 17.8% but that of fiscal 2026 indicates 2.2% growth.

In the near term, the in-house efforts might not scale the bottom line, but the mid and long-term prospects seem to be improving, with analysts being optimistic about DHI’s potential.

D.R. Horton stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 10 hours | |

| 10 hours | |

| 12 hours | |

| 15 hours | |

| 16 hours | |

| 16 hours | |

| 16 hours | |

| 18 hours | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite