|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at DraftKings (NASDAQ:DKNG) and its peers.

Gaming solution companies operate in a dynamic and evolving market, and the digital transformation of the gaming industry presents significant opportunities for innovation and growth, whether it be immersive slot machine terminals or mobile sports betting. However, the gaming solution industry is not without its challenges. Regulatory compliance is a crucial consideration as companies must navigate a complex and often fragmented regulatory landscape across different jurisdictions. Changes in regulations can impact product offerings, operational practices, and market access, requiring companies to maintain flexibility and adaptability in their business strategies. Additionally, the competitive nature of the industry necessitates continuous investment in research and development to stay ahead of competitors and meet evolving consumer demands.

The 7 gaming solutions stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 2.2%.

While some gaming solutions stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.2% since the latest earnings results.

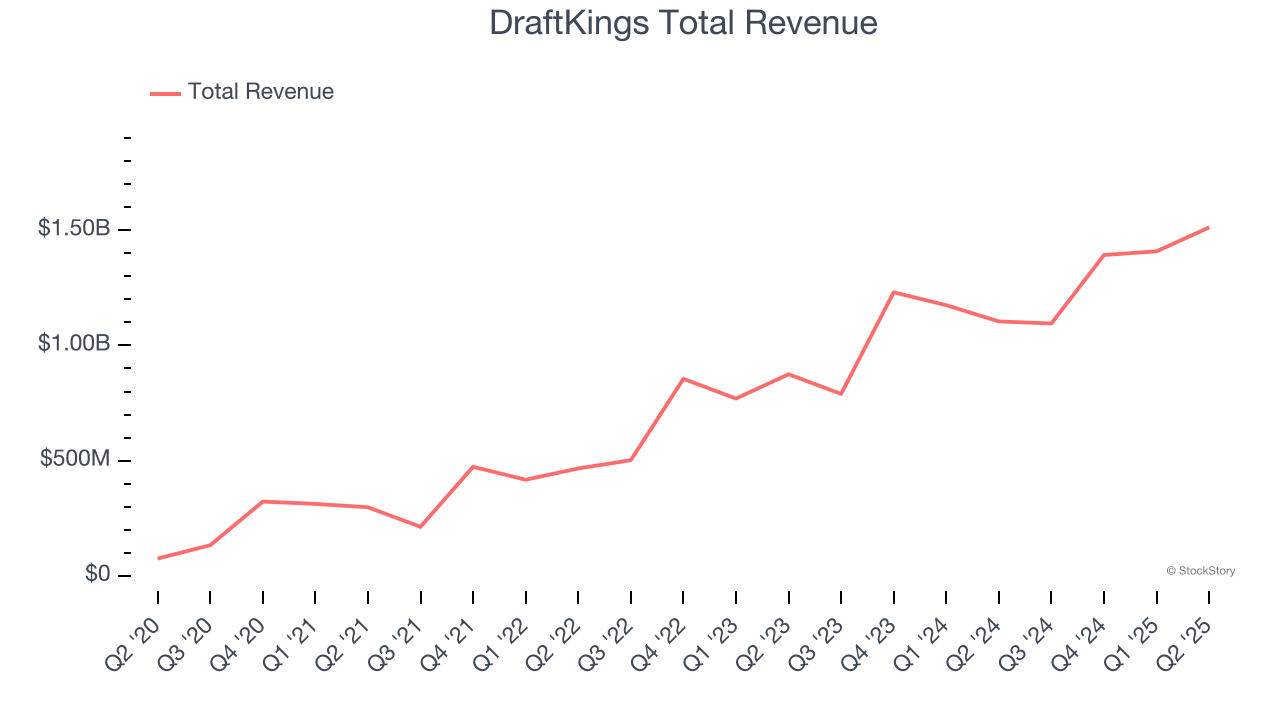

Getting its start in daily fantasy sports, DraftKings (NASDAQ:DKNG) is a digital sports entertainment and gaming company.

DraftKings reported revenues of $1.51 billion, up 36.9% year on year. This print exceeded analysts’ expectations by 5.9%. Overall, it was a strong quarter for the company with a solid beat of analysts’ adjusted operating income estimates.

“We set records for revenue, net income and Adjusted EBITDA in the second quarter, driven by an acceleration in revenue growth to 37% year-over-year,” said Jason Robins, DraftKings’ Chief Executive Officer and Co-founder.

DraftKings pulled off the fastest revenue growth but had the weakest full-year guidance update of the whole group. The company reported 3.3 million users, up 6.5% year on year. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 6.6% since reporting and currently trades at $42.37.

Is now the time to buy DraftKings? Access our full analysis of the earnings results here, it’s free.

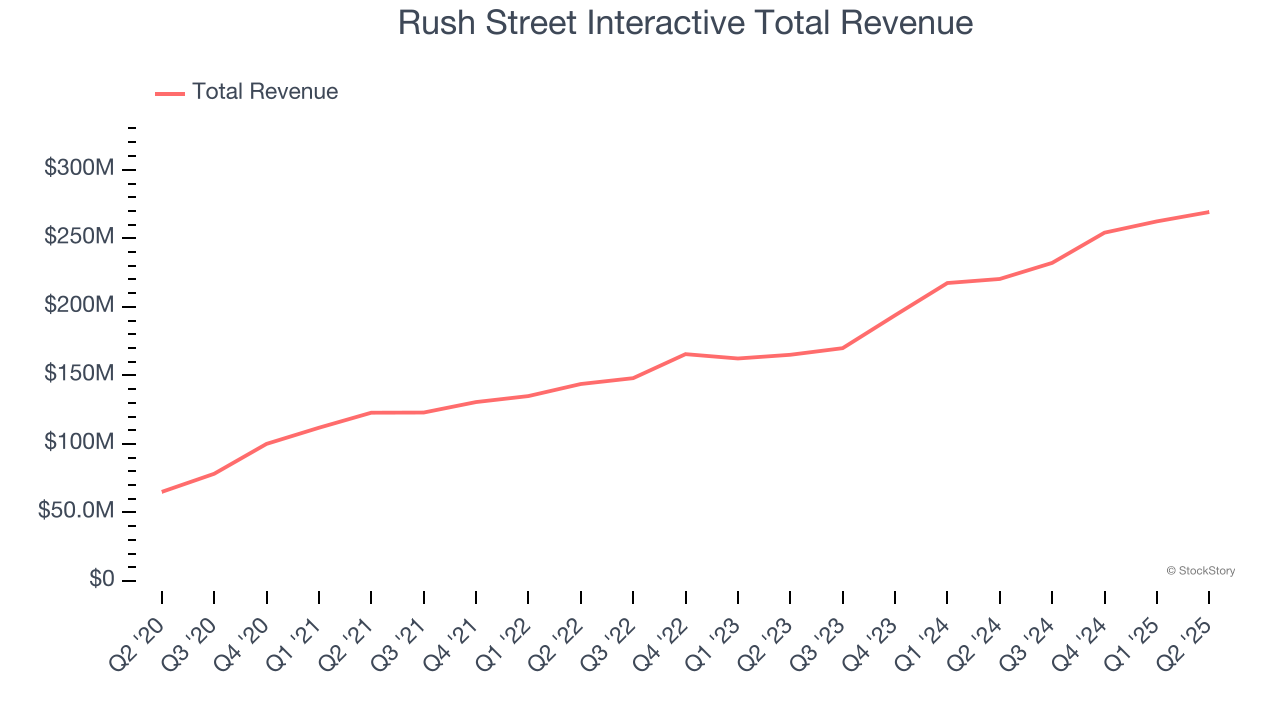

Specializing in online casino gaming and sports betting, Rush Street Interactive (NYSE:RSI) is an operator of digital gaming platforms.

Rush Street Interactive reported revenues of $269.2 million, up 22.2% year on year, outperforming analysts’ expectations by 7.6%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

Rush Street Interactive scored the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 33.9% since reporting. It currently trades at $21.48.

Is now the time to buy Rush Street Interactive? Access our full analysis of the earnings results here, it’s free.

With names as crazy as Ultimate Fire Link Power 4 for its products, Light & Wonder (NASDAQ:LNW) is a gaming company supplying the casino industry with slot machines, table games, and digital games.

Light & Wonder reported revenues of $809 million, down 1.1% year on year, falling short of analysts’ expectations by 4.4%. It was a softer quarter as it posted a miss of analysts' sales estimates.

Light & Wonder delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 6.6% since the results and currently trades at $84.96.

Read our full analysis of Light & Wonder’s results here.

Established in Illinois, Accel Entertainment (NYSE:ACEL) is a provider of electronic gaming machines and interactive amusement terminals to bars and entertainment venues.

Accel Entertainment reported revenues of $335.9 million, up 8.6% year on year. This result surpassed analysts’ expectations by 1%. More broadly, it was a satisfactory quarter as it also produced a beat of analysts’ EPS estimates but a miss of analysts’ adjusted operating income estimates.

The stock is down 8.2% since reporting and currently trades at $11.37.

Read our full, actionable report on Accel Entertainment here, it’s free.

Famous for hosting the Kentucky Derby, Churchill Downs (NASDAQ:CHDN) operates a horse racing, online wagering, and gaming entertainment business in the United States.

Churchill Downs reported revenues of $934.4 million, up 4.9% year on year. This number beat analysts’ expectations by 1.4%. Taking a step back, it was a strong quarter for the company as it also recorded a beat of analysts' sales and earnings estimates.

The stock is down 12.1% since reporting and currently trades at $96.

Read our full, actionable report on Churchill Downs here, it’s free.

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Feb-20 |

Cathie Wood Sells More DraftKings. Goldman Cuts Robinhood Target Due To These Metrics.

DKNG

Investor's Business Daily

|

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite