|

|

|

|

|||||

|

|

|

The best dividend stocks don't just pay a regular income. They can build a fortune over time.

Two dividend stocks flying under the radar have the potential to generate big returns.

Both companies are going all out on growth and want to hike dividends every year.

The biggest mistake investors make when picking dividend stocks is focusing solely on yields. While a high yield is preferable, it doesn't automatically make the stock worth a bet. At least, not by itself.

The best dividend socks are those that pay a regular dividend and increase it over time by growing cash flows. Such stocks are often the most bankable dividend stocks, offering decent yields and having the potential to generate significant returns over time thanks to steady dividend growth. Here are two such incredible dividend stocks worth doubling up on now.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

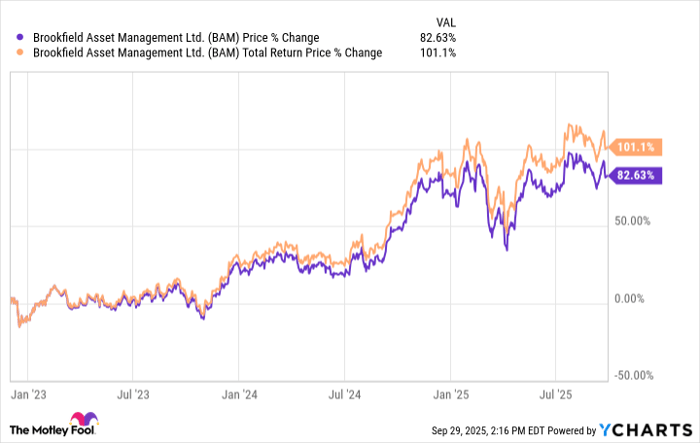

Brookfield Asset Management (NYSE: BAM) is one of the most underrated dividend stocks out there. If you've never looked at it for dividends, what I tell you next will make you change your perspective.

Brookfield Asset Management's primary goal is to "generate increasing cash flows" and distribute that cash to its shareholders by way of dividends or share repurchases. That's what the company has done so far. Since its formation in 2022 after getting spun off from Brookfield Corporation, Brookfield Asset Management has increased its dividend every year. With dividends reinvested, the stock has doubled since.

Brookfield's dividend strength stems from its business model. It is one of the largest alternative asset managers in the world, with more than $1 trillion of assets under management (AUM) in over 50 countries focused on alternative investments like infrastructure, renewable power, real estate, private equity, and credit. Most importantly, almost $560 billion of its AUM is fee-based capital, generating stable and recurring long-term fees. This steady fee income underpins Brookfield's confident dividend growth goals.

Here's the real deal if you double up on the stock now: Brookfield Asset Management plans to more than double its fee-bearing capital to $1.2 trillion by 2030. This also implies a projected 2x growth in distributable earnings per share (EPS) -- the portion of earnings typically available for distribution as dividends.

So, here's a company generating substantial fee-based earnings with plans to double them over the next five years. That should also mean big dividend hikes coming your way every year. Brookfield Asset yields 3% and increased its dividend per share by a solid 15% in 2024.

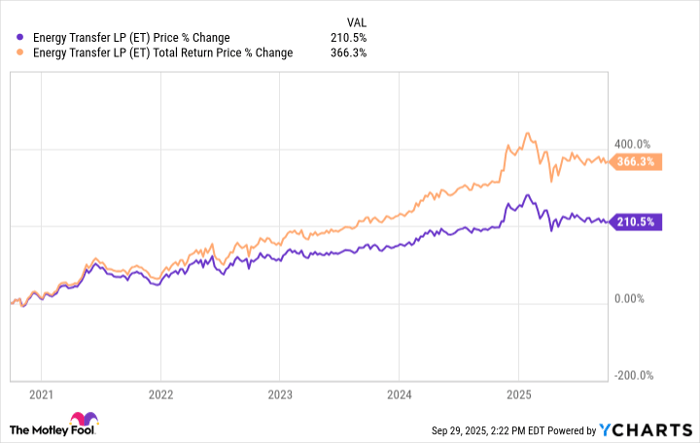

Among the many dividend-paying oil and gas stocks, Energy Transfer (NYSE: ET) stands out as the one you could double up on right now. The stock yields a hefty 7.5%, aims to grow annual dividend by 3% to 5%, and is investing in high-growth areas to back bigger dividends.

With demand for natural gas expected with rising demand for stable power from fast-growing markets like data centers, Energy Transfer is all set to capitalize on the opportunity. It already moves around 30%of the natural gas produced in the U.S., linking major production basins with end users and export getaways. Earlier this year, Energy Transfer signed a multiyear deal with CloudBurst to supply natural gas to its data centers for up to 1.2 gigawatts of power. In its latest investor presentation, Energy Transfer also revealed that it has "requests" to connect nearly 200 data centers across its network.

Energy Transfer is pumping $5 billion this year alone on expansions. Major projects include expansion in the Permian Basin, the Hugh Branson pipeline that can capitalize on the data center boom in Texas, and the Nederland Flexport NGL terminal, which is the world's second-largest natural gas liquids export facility.

With all the growth opportunities ahead and a huge project backlog, Energy Transfer should be able to meet its dividend growth target and generate meaningful returns for its shareholders like it has in the past. It's a top dividend stock to buy.

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $650,607!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,114,716!*

Now, it’s worth noting Stock Advisor’s total average return is 1,068% — a market-crushing outperformance compared to 190% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 29, 2025

Neha Chamaria has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Brookfield and Brookfield Corporation. The Motley Fool recommends Brookfield Asset Management. The Motley Fool has a disclosure policy.

| 2 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite