|

|

|

|

|||||

|

|

|

Guess?, Inc. GES reported fourth-quarter fiscal 2025 results, wherein the top and bottom lines beat the Zacks Consensus Estimate. While net sales increased, earnings decreased from the year-ago period. Sales growth was primarily driven by the acquisition of rag & bone (concluded in April 2024), alongside modest gains in GES’ core operations.

The company is optimistic about growth opportunities across its core Guess brand, the newly launched Guess Jeans line and the acquisition of rag & bone. GES plans to improve overall profitability by sharpening its global direct-to-consumer strategy and streamlining business portfolio. These strategic moves are expected to contribute to a $30 million boost in operating profit by fiscal 2027.

GES posted adjusted quarterly earnings of $1.48 per share, surpassing the Zacks Consensus Estimate of $1.41. However, the bottom line declined 26.4% from $2.01 reported in the prior-year period.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Guess?, Inc. price-consensus-eps-surprise-chart | Guess?, Inc. Quote

Net revenues were $932.3 million, rising 4.6% year over year and surpassing the consensus mark of $899 million. On a constant-currency (cc) basis, net revenues rose 9%. The strong performance was driven by the rag & bone acquisition and positive momentum in the wholesale businesses across Europe and the Americas, and higher licensing revenues. All operating segments contributed to revenue growth, with the exception of the Asia segment, which saw a decline.

Gross margin contracted to 44.1% from 45.4% reported in the year-ago quarter. As a percentage of sales, SG&A expenses increased to 32.8% from 29.1% in the prior-year quarter.

Adjusted earnings from operations were $106.5 million, down 18.2% from $130.2 million reported in the year-ago quarter. The adjusted operating margin was 11.4%, down from 14.6% reported in the same quarter last year. This downtick was mainly caused by increased expenses, higher advertising and store-related costs, as well as the impact of newly acquired businesses. These pressures were partially offset by lower performance-based compensation.

Revenues in the Americas Retail segment rose 4% in U.S. dollars and 6% at cc. However, retail comparable sales, including e-commerce, declined 14% in U.S. dollars and 11% at cc. The operating margin in the segment was 8.9%, down 6.1% year over year. This decline was caused by the adverse effects of negative comparable sales, higher expenses and increased markdowns.

Americas Wholesale revenues soared 63% on a reported basis and 69% at cc. The segment’s operating margin fell to 12.8%, down 15.7% year over year due to the impact of newly acquired businesses and lower product margin.

The Europe segment’s revenues increased 2% on a reported basis and 7% at cc. Retail comp sales (including e-commerce) remained relatively flat on a reported basis and increased 5% at cc. The segmental operating margin was 15.4%, down 2.6% year over year, due to higher expenses and the impact of newly acquired businesses. This was partially offset by lower markdowns.

Asia revenues decreased 15% on a reported basis and 11% at cc. Retail comp sales (including e-commerce) dropped 16% and 11% on a reported basis and at cc, respectively. The operating margin in the segment was 1.3%, down 3.5% year over year. This downside was primarily due to lower product margins and reduced revenues.

Licensing revenues increased 18% on a reported basis and at cc. Segmental operating margin was 94.8% compared with 92.7% in the year-ago quarter, mainly driven by lower expenses.

The company exited the quarter with cash and cash equivalents of $187.7 million and long-term debt and finance lease obligations of nearly $150.7 million. Stockholders’ equity was around $505 million.

Net cash provided by operating activities for the fiscal year ended Feb. 1, 2025, was $121.7 million. Free cash flow for the same period amounted to $29.8 million. For fiscal 2026, free cash flow is expected to be $55 million.

GES announced a quarterly dividend of 30 cents per share, payable on May 2, 2025, to its shareholders on record as of April 16.

The company repurchased about 2.6 million shares for $60.3 million during fiscal 2025.

For fiscal 2026, Guess? anticipates revenues to grow of 3.9-6.2%.

The adjusted operating margin is expected to be 4.5-5.4%. The GAAP operating margin is likely to be 4.3-5.2%.

Management expects adjusted earnings per share (EPS) of $1.32-$1.76 in fiscal 2026 compared with the $1.96 recorded in fiscal 2025. On a GAAP basis, EPS is envisioned in the range of $1.03-$1.37 compared with the 77 cents reported in fiscal 2025.

For the first quarter of fiscal 2026, management expects revenue growth of 5.8-7.5%. On an adjusted basis, Guess? expects to post a loss of 74-65 cents per share. On a GAAP basis, it expects to deliver a loss in the range of 75-66 cents per share.

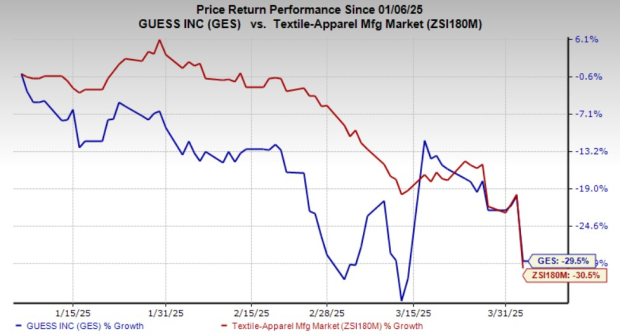

Shares of this Zacks Rank #4 (Sell) company have lost 29.5% in the past three months compared with the industry’s 30.5% decline.

V.F. Corporation VFC engages in the design, procurement, marketing and distribution of branded lifestyle apparel, footwear and accessories for men, women and children in the Americas, Europe and the Asia-Pacific. It sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for V.F. Corp’s current-quarter EPS indicates growth of 53.1% from the year-ago levels. VFC delivered an earnings surprise of 82.4% in the last reported quarter.

Ralph Lauren Corporation RL designs, markets and distributes lifestyle products in North America, Europe, Asia and internationally. It currently flaunts a Zacks Rank #1. RL delivered a trailing four-quarter average earnings surprise of 6.5%.

The Zacks Consensus Estimate for Ralph Lauren’s current fiscal-year sales and earnings indicates growth of 5.8% and 16.5%, respectively, from the year-ago actuals.

Gildan Activewear Inc. GIL manufactures and sells various apparel products. It carries a Zacks Rank of 2 (Buy) at present. GIL delivered a trailing four-quarter earnings surprise of 5.3%, on average.

The consensus estimate for Gildan Activewear’s current fiscal-year sales and earnings indicates growth of 4.4% and 16%, respectively, from the year-ago actuals.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-01 | |

| Apr-01 | |

| Mar-26 | |

| Mar-24 | |

| Mar-24 | |

| Mar-18 | |

| Mar-17 | |

| Mar-13 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-08 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite