|

|

|

|

|||||

|

|

|

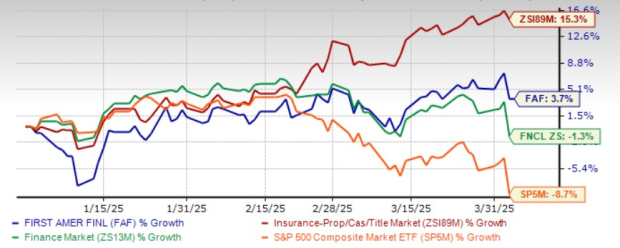

Shares of First American Financial Corporation FAF have gained 3.7% year to date, underperforming the industry’s growth of 15.3% but outperforming the Finance sector’s decrease of 1.3% and the Zacks S&P 500 composite’s decrease of 8.7%.

FAF shares are trading well above the 50-day moving average, indicating a bullish trend.

Increased demand among millennials for first-time home purchases, the expansion of valuation and data businesses and strength in commercial business and technological upgrades should help FAF perform solidly.

Based on short-term price targets offered by five analysts, the Zacks average price target is at $76.20 per share. The average suggests a potential 17.7% upside from the last closing price.

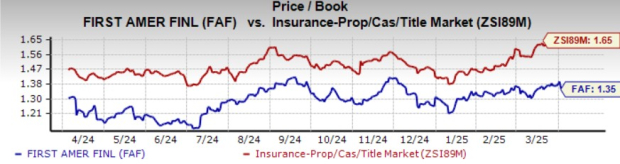

FAF shares are trading at a price-to-book multiple of 1.35, lower than the industry average of 1.65. Its pricing, at a discount to the industry average, gives a better entry point to investors. Also, it has a Value Score of B.

Shares of other insurers like Fidelity National Financial, Inc. FNF are trading at a multiple higher than the industry average, while shares of Old Republic International Corporation ORI are trading at a multiple lower than the industry average.

The Zacks Consensus Estimate for 2025 earnings has moved 1.3% south, while the same for 2026 has moved 2% north in the past 30 days.

The Zacks Consensus Estimate for 2025 implies a 19.3% year-over-year increase and the same for 2026 suggests a 17.1% increase.

First American stands to gain from increased demand for first-time home purchases among millennials. It expects housing demand, improving economy and labor markets to drive home price appreciation. Growing leadership in title data, courtesy of proprietary data extraction, sturdy distribution relationships, prudent underwriting and continued investments in technology poise FAF well for long-term growth.

FAF expects modest improvement in both residential purchase and refinance businesses for 2025. The company is witnessing early stabilization in the purchase market and thus expects housing demand, improving economy and labor markets to continue to drive home price appreciation.

Growing direct premiums, escrow fees and title agent premiums should continue to drive the top line.

The title insurer stays focused on strengthening its product offerings, enhancing core business and expanding valuation and data businesses. Also, the expansion of title plant assets and the upgrade of technology solutions drive increased efficiency.

Its cost-control initiative has been aiding margin expansion.

First American distributes wealth to shareholders via dividend hikes and share buybacks. Its dividend yield as well as payout ratio betters the industry average, making it an attractive pick for yield-seeking investors.

Despite the upside potential, there are a few factors that investors should keep an eye on.

The Federal Reserve cut rates thrice in 2024 and has hinted at two more cuts this year. Insurers are direct beneficiaries of a rising rate environment. Thus, investment income is likely to be affected.

First American Financial’s debt levels have been increasing in the past few years. Times interest earned has declined too. Both metrics compared unfavorably with the industry average.

Return on equity in the trailing 12 months was 9.3%, marginally above the industry average of 8.3%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders.

Return on invested capital (ROIC) reflects a company’s efficiency in utilizing funds to generate income. FAF’s ROIC in the trailing 12 months was 2.9%, lower than the industry average of 6.4%.

Increased demand among millennials for first-time home purchases and strength in commercial business should favor FAF’s results. The solid dividend yield is another positive. FAF’s near-term prospects look bright, given its VGM Score of B.

Despite an attractive valuation, it is better to adopt a wait-and-see approach for this Zacks Rank #3 (Hold) insurer, given mixed analyst sentiment, unfavorable leverage and times interest earned. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-16 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-03 | |

| Mar-02 | |

| Mar-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite