|

|

|

|

|||||

|

|

|

The demand for CoreWeave's dedicated AI data centers is showing no signs of slowing down.

Nvidia recently gave CoreWeave a contract that guarantees the usage of its capacity for the next few years, and this was followed by a new multibillion-dollar contract from OpenAI.

CoreWeave's valuation and growth prospects indicate that this AI stock is capable of soaring higher.

CoreWeave (NASDAQ: CRWV), a neocloud company that rents out its specialized data centers focused on running artificial intelligence (AI) workloads, has turned into one of the hottest stocks on the market in 2025. Its share price has more than tripled in just over six months since its initial public offering (IPO) toward the end of March. Importantly, recent developments at CoreWeave suggest that the stock's red-hot rally is sustainable.

Given that the stock has already seen so much appreciation in such a short time, is it still worth buying at this point?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

Neocloud providers such as CoreWeave build and deploy dedicated AI data centers. These data centers are equipped with powerful graphics processing units (GPUs), usually with the latest chips from popular chip designers like Nvidia. The AI-optimized nature of these data centers makes them ideal for running and deploying AI applications in the cloud.

Customers simply rent the required data center capacity from CoreWeave instead of purchasing expensive hardware and incurring additional overhead related to managing the infrastructure.

Not surprisingly, CoreWeave's business model has been a massive success. The company has been offering access to flagship AI compute hardware from Nvidia, including its latest-generation Blackwell chips, along with data storage and networking tools.

Additionally, CoreWeave provides access to managed services on which its customers can build, train, and deploy AI applications. The demand for this GPU-as-a-service business model is so strong that CoreWeave has been landing new business at an eye-popping rate. AI giant OpenAI, for instance, expanded its existing relationship with CoreWeave by offering the latter a $6.5 billion contract.

OpenAI is buying capacity from CoreWeave to "power the training of its most advanced next-generation models." In fact, OpenAI has been regularly buying up CoreWeave's data center capacity since the beginning of the year. It's now sitting on $22.4 billion worth of contract value from the ChatGPT maker, following the latest award.

CoreWeave's growing relationship with OpenAI is good news, as CoreWeave has been reliant on Meta Platforms and Microsoft for a major chunk of its revenue. Another thing worth noting is that the company received a $6.3 billion contract from Nvidia recently, with the graphics card giant willing to buy any unsold data center capacity that CoreWeave is left with through April 2032.

These new contracts should have ideally led to a big bump in CoreWeave's order book. The company reported that it was sitting on a $30.1 billion revenue backlog at the end of Q2, with the metric jumping by 86% from the year-ago period. The two new contracts from OpenAI and Nvidia should have added nearly $13 billion to that figure in Q3, minus any of the contracts that CoreWeave fulfilled in this period.

As a result, there's a solid chance that CoreWeave will further boost its 2025 revenue guidance. It expects $5.25 billion in revenue this year, which is already going to be a big increase over its 2024 top line of $1.9 billion. But now that CoreWeave is getting even more business, it has the incentive to bring online more data center capacity at a faster pace so that it can convert more of its massive backlog into revenue.

That's precisely what analysts and investors would want to see from the company. A potential acceleration in CoreWeave's growth on account of its huge backlog can continue to be a tailwind for the stock, especially considering its valuation.

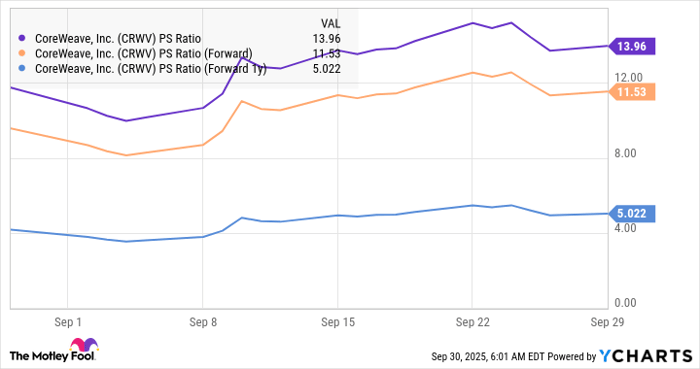

CoreWeave's price-to-sales ratio (P/S) of 14 is definitely not cheap when you consider that the tech-laden Nasdaq Composite index has an average sales multiple of 5. But CoreWeave is on track to more than double its revenue in 2025, followed by big jumps in the next couple of years, and that justifies its sales multiple.

Data by YCharts.

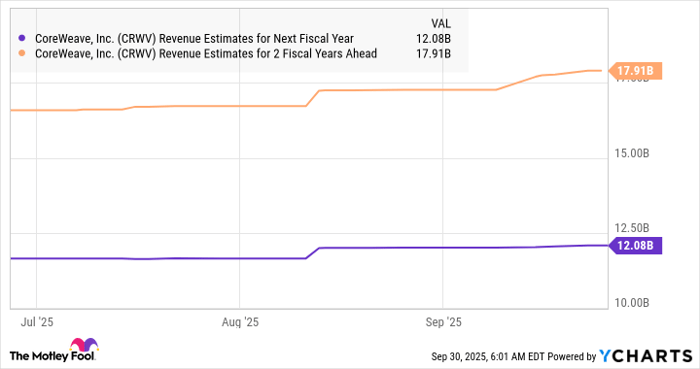

Moreover, the fact that CoreWeave's backlog is bigger than the revenue that it's expected to generate in the next couple of years suggests that it's capable of growing at a faster pace. This explains why CoreWeave's forward sales multiples are way more attractive.

Data by YCharts.

If CoreWeave trades at 5x sales after a couple of years (as per the chart above and in line with the Nasdaq Composite index) and achieves even $18 billion in revenue (as seen in the first chart of this section), its market cap could jump to $90 billion. That points toward a potential increase of 50% in its market cap from current levels, though don't be surprised to see this AI stock delivering bigger gains as it has the ability to outpace consensus estimates, thanks to the points discussed above.

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $621,976!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,150,085!*

Now, it’s worth noting Stock Advisor’s total average return is 1,058% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 29, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 17 min | |

| Feb-15 | |

| Feb-15 | |

| Feb-14 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite