|

|

|

|

|||||

|

|

|

JD.com JD is reinforcing its leadership in China’s e-commerce market through a vertically integrated, supply chain-driven model that combines retail, logistics and marketplace services. JD Retail, the company’s core growth engine, leverages direct procurement, nationwide warehousing and last-mile delivery to serve key categories such as electronics, home appliances and general merchandise. This model emphasises reliability and product authenticity, supporting margin expansion and customer loyalty as China’s retail market shifts toward efficiency and value.

Retail remained the dominant growth driver in the second quarter of 2025, contributing nearly 87% of JD’s total revenue. Segment sales grew 21% year over year, to RMB 310.1 billion ($43.3 billion), reflecting broad-based strength across home appliances, general merchandise, and supermarket categories. The consistent expansion in profitability underscores the scalability of JD’s integrated model and its ability to sustain growth despite a competitive environment.

JD is well-positioned to capture growth from China’s expanding e-commerce market, which Mordor Intelligence estimates will reach 1.53 trillion in 2025 and expand to 2.52 trillion by 2030 at a CAGR of 10.42%. The company’s deep logistics infrastructure, direct-sourcing model and leadership in high-frequency categories enable it to serve rising consumer demand efficiently and profitably as online penetration accelerates across lower-tier cities. JD continues to focus on optimising procurement, improving category mix and driving user engagement. Its expanding ecosystem across logistics, marketplace, and on-demand retail further strengthens JD Retail by increasing purchase frequency and supporting sustained margin gains.

The Zacks Consensus Estimate for third-quarter 2025 revenues is pegged at $41.21 billion, up 11.06% year over year, with 2025 revenues pegged at $183.33 billion, indicating 14.04% growth. These forecasts reflect confidence in JD’s ability to extend its retail momentum and translate operational strength into consistent top-line expansion. With a disciplined execution framework and growing ecosystem synergies, JD’s retail-led model continues to validate a strengthening growth thesis.

Competition in China’s e-commerce market remains intense, with JD.com, PDD Holdings PDD, and Alibaba BABA pursuing distinct growth paths. PDD Holdings continues to expand aggressively in price-sensitive segments through its Temu platform, while Alibaba is refocusing on efficiency and profitability within its Taobao and Tmall businesses. JD differentiates itself through its supply chain depth and premium positioning in high-frequency categories. As PDD Holdings drives scale through value-based offerings and Alibaba rebalances operations post-restructuring, JD’s emphasis on logistics control and service reliability remains a key advantage in sustaining profitable market share growth.

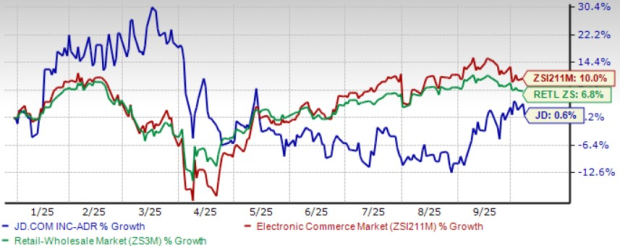

Shares of JD.com have increased 0.6% year to date, underperforming the Zacks Internet-Commerce industry and Zacks Retail-Wholesale sector’s return of 10% and 6.8%, respectively.

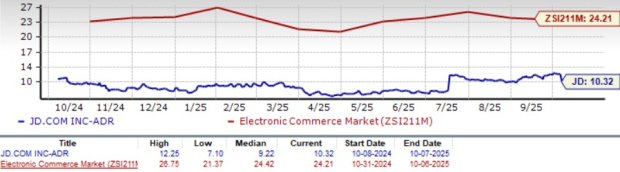

From a valuation standpoint, JD.com is trading at a forward 12-month price-to-earnings ratio of 10.32X, lower than the industry’s 24.21X. JD carries a Value Score of A.

The Zacks Consensus Estimate for JD’s third-quarter 2025 earnings is pegged at 44 cents per share, unchanged over the past 30 days. The earnings figure suggests a 64.52% decline year over year.

JD.com, Inc. price-consensus-chart | JD.com, Inc. Quote

JD.com currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-26 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite