|

|

|

|

|||||

|

|

|

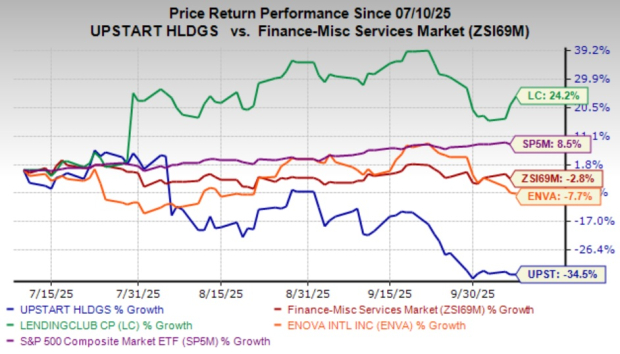

Upstart Holdings UPST has been on a wild ride once again. After a strong first half of 2025, when optimism around its AI-powered lending model reignited investor enthusiasm, the stock has tumbled roughly 34.5% over the past three months. The decline has raised questions about whether this is another temporary stumble or a sign of deeper trouble in the credit landscape.

Upstart’s steep decline was driven by softer credit conditions and fallout from distress in the used car lending market. Although not directly related to the company, the bankruptcy of Tricolor Holdings, which catered to borrowers with limited credit history, amplified worries about credit quality. Given Upstart’s AI-driven lending model’s sensitivity to credit cycles, investor sentiment weakened sharply, pressuring the stock further.

Upstart underperformed the Zacks Financial – Miscellaneous Services industry as well as the S&P 500 composite. Comparatively, its peers, LendingClub LC and Enova International ENVA, put up a better performance in terms of share price during this period.

Lost in the market turbulence is the fact that Upstart’s fundamentals have actually improved meaningfully in 2025. The company’s second-quarter results marked its strongest performance in years. Revenues more than doubled year over year to $257 million, while loan originations surged to $2.8 billion, marking the highest volume in three years.

Equally important, Upstart achieved GAAP profitability a quarter earlier than expected, posting $5.6 million in net income compared to a $54.5 million loss a year ago. Contribution profit rose 85% to $141 million, maintaining a healthy 58% margin. Conversion rates improved to nearly 24%, underscoring both efficiency and demand for its lending platform.

Management also guided for full-year 2025 revenues of around $1.05 billion and net income of $35 million, signaling that profitability is not a one-quarter blip but part of a longer-term turnaround.

Upstart’s efforts to expand beyond personal lending are starting to pay off. Auto loan originations jumped more than sixfold over the past year, while its Home segment grew nearly ninefold. Together with small-dollar loans, these verticals now contribute more than 10% of the total volume, diversifying its revenue base.

Credit union partnerships in recent times, such as those with Cornerstone Community Financial Credit Union and ABNB Federal Credit Union, also reflect growing confidence among lenders in Upstart’s AI platform. These partnerships not only provide stable funding sources but also extend the company’s reach into community-based lending networks.

What continues to set Upstart apart is its use of artificial intelligence in credit underwriting. The company’s latest model, called Model 22, uses neural networks at the “meta” layer of its credit model. This resulted in a 17 percentage-point boost in separation accuracy compared to the benchmark textbook credit model, allowing for higher conversion rates and lower acquisition costs.

Moreover, Upstart’s automation advantage remains significant, with 92% of loans in the second quarter being fully automated, requiring no human intervention. This operational efficiency allows lenders to approve more loans faster and often at lower interest rates, making the platform appealing to both borrowers and financial institutions.

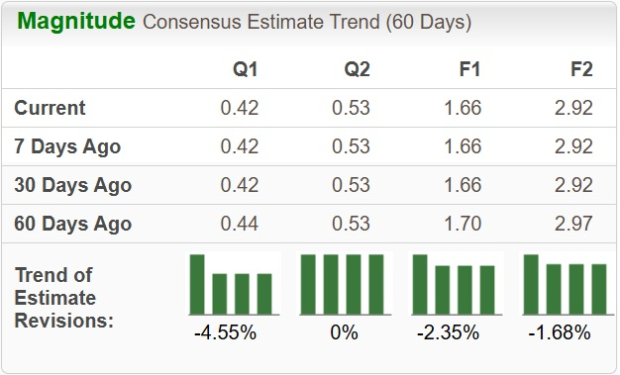

The recent estimate revision trends also echo similar sentiments. While the full-year 2025 and 2026 Zacks Consensus Estimates for EPS have been revised downward over the past two months, the figures suggest a significant increase year over year.

From a valuation perspective, we note that Upstart shares are currently overvalued, as suggested by the Value Score of F.

In terms of forward 12-month Price/Sales (P/S), despite the decline in the share price, Upstart is currently trading at 4.08X, which is at a premium to the industry average of 3.91X. Moreover, compared with fintech rivals, the stock trades at a premium to LendingClub and Enova International. At present, LendingClub and Enova International have P/S multiples of 1.69 and 0.76, respectively.

There’s no denying that the near-term outlook for Upstart is murky. The company’s heavy exposure to credit-sensitive borrowers means its stock is likely to remain volatile as economic conditions fluctuate. The recent decline reflects these risks rather than any fundamental collapse in its business model.

Still, Upstart’s rebound in revenues, return to profitability and continued expansion into new lending categories suggest the company is far better positioned today. Its AI-driven platform continues to attract lender partnerships, offering a scalable and differentiated approach to credit underwriting.

While the sell-off has created an attractive entry point for long-term investors, caution is warranted, given the uncertain credit environment. For now, Upstart looks best suited as a hold — a stock worth watching closely rather than rushing to buy or sell amid short-term market turbulence.

Currently, Upstart carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-10 | |

| Jul-09 | |

| Jul-08 | |

| Jul-06 | |

| Jul-06 | |

| Jun-25 | |

| Jun-24 | |

| Jun-10 | |

| Jun-03 | |

| Jun-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite