|

|

|

|

|||||

|

|

|

Arm Holdings ARM continues to command attention with its sky-high valuation, trading at a price-to-earnings (P/E) ratio of 173.72 and a forward P/E of 84.25, significantly higher than the semiconductor industry average of approximately 37.61. While such figures underscore strong investor confidence in the company’s long-term prospects, they also leave minimal margin for error.

The British chip designer’s increased R&D spending, coupled with rising competition from China’s growing focus on RISC-V chip architecture, adds further pressure. Additionally, potential friction with existing partners could emerge if ARM ventures deeper into CPU manufacturing, an area traditionally served by its licensees.

Still, the company’s fundamentals remain robust. ARM maintains an impressive 99% share in mobile chip design and is steadily strengthening its presence in AI data centers, a critical growth frontier. Its strong gross margins and healthy $2.9 billion cash position provide a financial cushion to support innovation and expansion.

However, despite these positives, analysts are signaling caution in the near term. The stock’s rich valuation, combined with execution risks and competitive uncertainties, makes it less appealing for short-term investors seeking immediate upside. For those with a long-term horizon, ARM’s dominance in mobile and its growing role in AI infrastructure still paint a promising picture, but patience and a careful entry point may be key.

In short, ARM’s story remains compelling, yet its current valuation demands disciplined optimism rather than aggressive buying.

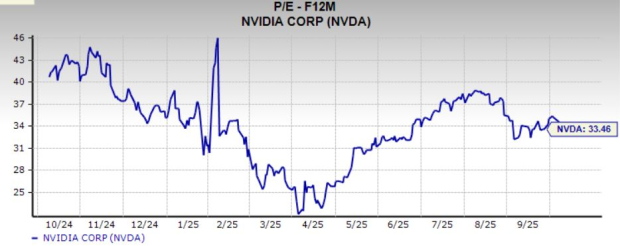

While ARM’s valuation may prompt caution, investors looking for semiconductor exposure with clearer financial traction might consider NVIDIA NVDA and Qualcomm QCOM. NVIDIA, with a forward 12-month P/E of 33.46, continues to dominate the AI accelerator space, driven by strong revenue and earnings growth, fueled by surging demand for its GPUs. The company’s leadership in AI infrastructure makes NVIDIA a favorite among growth-oriented investors.

Meanwhile, Qualcomm, trading at just 14.12x forward earnings, offers a more diversified chip portfolio spanning smartphones, automotive, and IoT. Its solid royalty business and increasing footprint in AI-powered edge devices position Qualcomm for steady expansion. Both NVIDIA and Qualcomm have demonstrated the ability to monetize their innovations more effectively than ARM, making them compelling alternatives.

ARM stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Nvidia Partner Surges After Earnings Beat; Expects 'Momentum' To Continue In 2026

NVDA

Investor's Business Daily

|

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite