|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Neocloud providers such as CoreWeave are growing at a terrific pace, a trend that's likely to continue as the company's swelling backlog indicates.

CoreWeave has been winning new business at a brisk pace, and its aggressive capex plan indicates that it is on track to become a key player in the global AI infrastructure market.

The good news isn't stopping for CoreWeave (NASDAQ: CRWV) investors as more and more evidence of the robust demand for the neocloud provider's cloud computing infrastructure emerges. CoreWeave is known for operating artificial intelligence (AI) data centers in Europe and the U.S., and major tech giants have been lining up to rent its data center capacity so that they can run AI workloads in the cloud. The company just struck another multibillion-dollar deal that's set to give its already booming revenue pipeline a massive boost.

It won't be surprising to see CoreWeave becoming a leader in the AI infrastructure market in the long run. Let's see why that's likely to be the case.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

CoreWeave's AI data centers are powered by graphics processing units (GPUs) from Nvidia. The company has been buying up Nvidia's latest GPUs, and that's a big reason why companies such as Microsoft, Meta Platforms, OpenAI, and others have been queuing up to lease its data center capacity.

Meta Platforms is one of its biggest customers, and the social media giant has just expanded its partnership with CoreWeave by offering it a $14.2 billion contract. This follows a recent expansion with OpenAI, which gave CoreWeave a $6.5 billion contract. As it stands, OpenAI has now offered total contracts worth $22.4 billion to CoreWeave this year.

Even Nvidia agreed to a $6.3 billion contract with CoreWeave last month, offering to buy the latter's unsold data center capacity through 2032. It is worth noting that CoreWeave was sitting on a $30.1 billion revenue backlog at the end of the second quarter. The three new contracts that the company has announced in the past few weeks indicate that its total revenue backlog is now worth more than $50 billion, a jump of over 3x as compared to its backlog in Q2 2024.

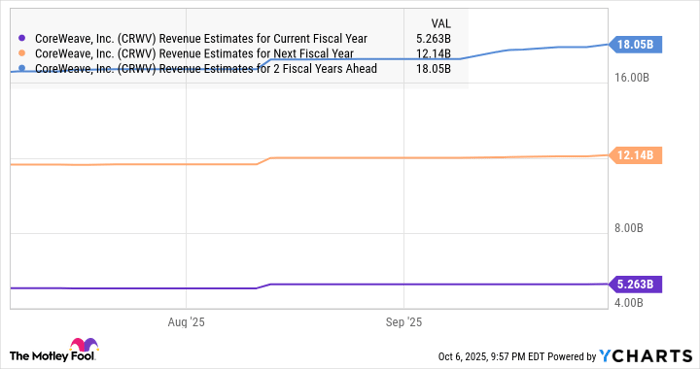

That's a big achievement for a company that's expecting to finish 2025 with an estimated $5.25 billion in revenue. To put things in perspective, CoreWeave is fast catching up to Oracle (NYSE: ORCL) in the cloud AI infrastructure market. Oracle is a much bigger player in this market with its massive data center network across the globe and was sitting on a $455 billion backlog at the end of the previous fiscal quarter.

Now, CoreWeave's backlog may be just a tenth of Oracle's, but the former has been punching hard when it comes to bringing more capacity online. For instance, CoreWeave is on track to spend $20 billion to $23 billion as capital expenditure (capex) in 2025, which would be a huge jump over its 2024 outlay of $8.3 billion. Oracle, meanwhile, is on track to increase its capex by 65% in the current fiscal year to $35 billion.

The faster expansion in CoreWeave's capex to significantly massive levels suggests that it is on its way to capturing a bigger chunk of the lucrative cloud AI infrastructure opportunity, which is set to get bigger in the long run. Importantly, the latest deals that the company has struck should also give it access to more funds so that it can continue adding new capacity at a brisk pace.

Management pointed out in August on its earnings call that it has increased its total contracted data center power capacity to 2.2 gigawatts from 600 megawatts. The contracted capacity refers to the available power agreements that will enable CoreWeave to equip more data centers with GPUs and other related equipment to service AI workloads.

So, as the company brings online more capacity, it should be able to convert a bigger share of its backlog into revenue. It should also be able to attract more customers, considering that data center capacity is expected to grow at an annual rate of 22%, according to McKinsey.

In all, it is easy to see why CoreWeave's revenue projections have moved higher in recent months, a trend that's likely to continue considering the new contracts that it recently signed.

Data by YCharts.

As the company reinvests its fast-expanding revenue into building more data centers, it should be able to sustain its outstanding growth for a long time to come.

CoreWeave's revenue is on track to jump by almost 2.8x this year at the midpoint of its guidance range. According to the previous chart, the company's top line could multiply by 3.4x in just two years. That's faster than what market leader Oracle is expecting.

Oracle's cloud infrastructure revenue is expected to jump by 77% in the ongoing fiscal year to $18 billion. It estimates a 77% increase in the next fiscal year to $32 billion, followed by a stronger increase to $73 billion in fiscal 2028. CoreWeave's backlog, its capacity expansion efforts, and the incredible opportunity in the cloud infrastructure market could eventually help it outpace Oracle's growth.

That's why it would be a good idea to buy CoreWeave while it is trading at 19 times sales, which isn't very expensive when compared to Oracle's sales multiple of 14, especially considering that the former has the ability to eventually become one of the leading players in the cloud AI infrastructure space.

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $654,835!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,159,218!*

Now, it’s worth noting Stock Advisor’s total average return is 1,081% — a market-crushing outperformance compared to 192% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of October 7, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

CoreWeave Stock Falls Amid Blue Owl Doubts, Data Center Debt Financing Report

CRWV -8.12%

Investor's Business Daily

|

| Feb-20 |

CoreWeave Stock Falls Amid Blue Owl Doubts, Data Center Debt Financing Report

ORCL -5.40%

Investor's Business Daily

|

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite