|

|

|

|

|||||

|

|

|

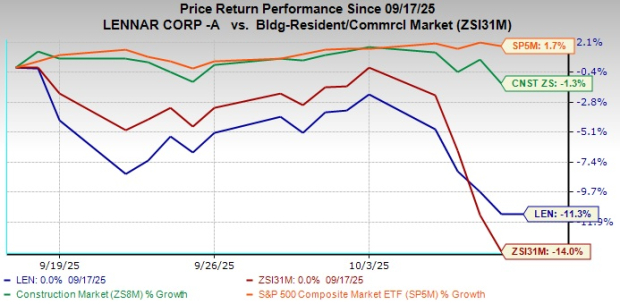

Lennar Corporation LEN has trended downward 11.3% since announcing its third-quarter fiscal 2025 earnings. It has outperformed the Zacks Building Products - Home Builders industry, but is hovering below the broader Zacks Construction sector and the S&P 500 index.

In the fiscal third quarter, this Florida-based homebuilder’s adjusted earnings per share and total revenues missed the Zacks Consensus Estimate by 5.6% and 2.5%, respectively. Both metrics even tumbled year over year by 48.7% and 6.4%, respectively. LEN’s performance was significantly hurt by the ongoing softness in the housing market, due to affordability challenges, with its initiative of lowering the ASP of home deliveries adding to the headwinds.

Let us dig deeper into understanding the factors that are hurting Lennar’s growth momentum.

The housing industry is cyclical and affected by consumer confidence levels, prevailing economic conditions and interest rates. Currently, the United States’ housing market is facing troubles in the form of affordability issues, as homebuyers are struggling between high mortgage rates and owning a house. Being a homebuilding company, Lennar’s business is getting affected, especially in the near and mid-term.

To counter the adverse impact of the housing market, the company has been offering homes at a lower ASP, which is reducing its top-line growth as a ripple effect. As of the first nine months of fiscal 2025, the ASP of home deliveries was $393,000, down 6.7% year over year from $421,000, leading to home sale revenues of $23.24 billion, down from $24.28 billion reported a year ago. For the fourth quarter of fiscal 2025, Lennar expects the ASP of the delivered homes to be in the range of $380,000-$390,000, down from $430,000 reported a year ago.

Lennar’s focus on maintaining volume by using price incentives and mortgage buydowns has been weighing heavily on its profitability for some time now. During the first nine months of fiscal 2025, home sales gross margin contracted year over year by 430 basis points (bps) to 18% from 22.3%. This decline was primarily caused by lower revenue per square foot and higher land costs year over year.

Despite management’s longer-term plan to rebuild margins through cost efficiencies, the near-term outlook remains muted. With home prices under pressure and Lennar continuing to deploy incentives to meet affordability thresholds, near-term margin expansion or earnings acceleration seems to be unrealistic. LEN’s guidance predicts margins will remain flat sequentially in the fiscal fourth quarter of 2025 at 17.5% and will decline from 22.1% a year ago.

After keeping the interest rate benchmark at 4.25-4.5%, on Sept. 17, 2025, the Federal Reserve slashed the interest rate by 0.25 percentage points, pulling the benchmark down to a range of 4-4.25%. Although the Fed hinted at two more rate cuts for the remainder of 2025, the ongoing market pressures resulting from the new tariff regime and other global political issues are concerning.

As of the week ending on Oct. 9, 2025, the mortgage rate per Freddie Mac has decreased to 6.3% after hovering around and above 6.5% since the start of 2025. This is somewhat good news, as Fed rate cuts are creating an optimistic buzz in the market; however, the intensity of macro uncertainties has not decreased much. Headwinds from ongoing affordability issues, elevated costs and economic uncertainty continue to haunt homebuilders like Lennar, restricting their near and mid-term growth possibilities despite a persistent housing inventory shortage.

Given the ongoing market fundamentals, Lennar remains cautious for its last fiscal quarter of 2025 and the start of fiscal 2026, as mortgage rates are expected to stay elevated for some time, or at least until there are market normalization signs.

LEN’s earnings estimates for fiscal 2025 and fiscal 2026 have moved down over the past 30 days to $8.58 and $9.22 per share, respectively, depicting analysts’ concerns about the stock’s growth potential.

The estimated figure for fiscal 2025 indicates a year-over-year decline of 38.1%, while that of fiscal 2026 reflects an improvement of 7.5%.

LEN stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 12.92, as shown in the chart below.

The overvaluation of the stock, compared with its peers, is making it difficult for investors to figure out a suitable entry point.

Lennar occupies one of the strongest positions among large U.S. homebuilders like D.R. Horton, Inc. DHI, PulteGroup, Inc. PHM and NVR, Inc. NVR.

D.R. Horton is leaning toward elevating incentive spending to increase homebuying. Its orders being the largest in the industry reflect scale-driven resilience and a heavier reliance on promotions to manage affordability. Contrarily, PulteGroup presents a mixed picture, where incentive offerings increased, but its net new orders and backlog trends indicate more regional variability.

Lastly, NVR practices a very asset-light approach, wherein it typically acquires finished lots (rather than developing land) and focuses on pre-sold homes, keeping its balance sheet lean and reducing exposure to land carrying costs and speculative risk. NVR also combines homebuilding with mortgage and title operations, but because it doesn’t tie up capital in land inventory, it can achieve strong returns on equity in up cycles.

Compared with the other market players, D.R. Horton, PulteGroup and NVR, Lennar’s competitive advantages include its scale, geographic diversification, vertical integration and financial strength. This allows it to ride through housing cycles more robustly than other peers.

As discussed above, Lennar’s efforts to support affordability, through lower ASPs and heavy use of buying incentives, are sustaining home delivery volumes but eroding profitability. Despite the company’s operational scale and efficiency-driven model, the overall U.S. housing market remains constrained by mortgage rates, keeping affordability at the forefront of challenges.

Thus, after considering muted earnings prospects for fiscal 2025 and a premium valuation, it is prudent for existing investors to sell off this Zacks Rank #5 (Strong Sell) stock from their portfolio until the market trends move in favor of it.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 10 hours | |

| 12 hours | |

| 15 hours | |

| 16 hours | |

| 16 hours | |

| 17 hours | |

| 18 hours | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite