|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

What a time it’s been for Hewlett Packard Enterprise. In the past six months alone, the company’s stock price has increased by a massive 71.4%, reaching $24.48 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Hewlett Packard Enterprise, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Despite the momentum, we're sitting this one out for now. Here are three reasons we avoid HPE and a stock we'd rather own.

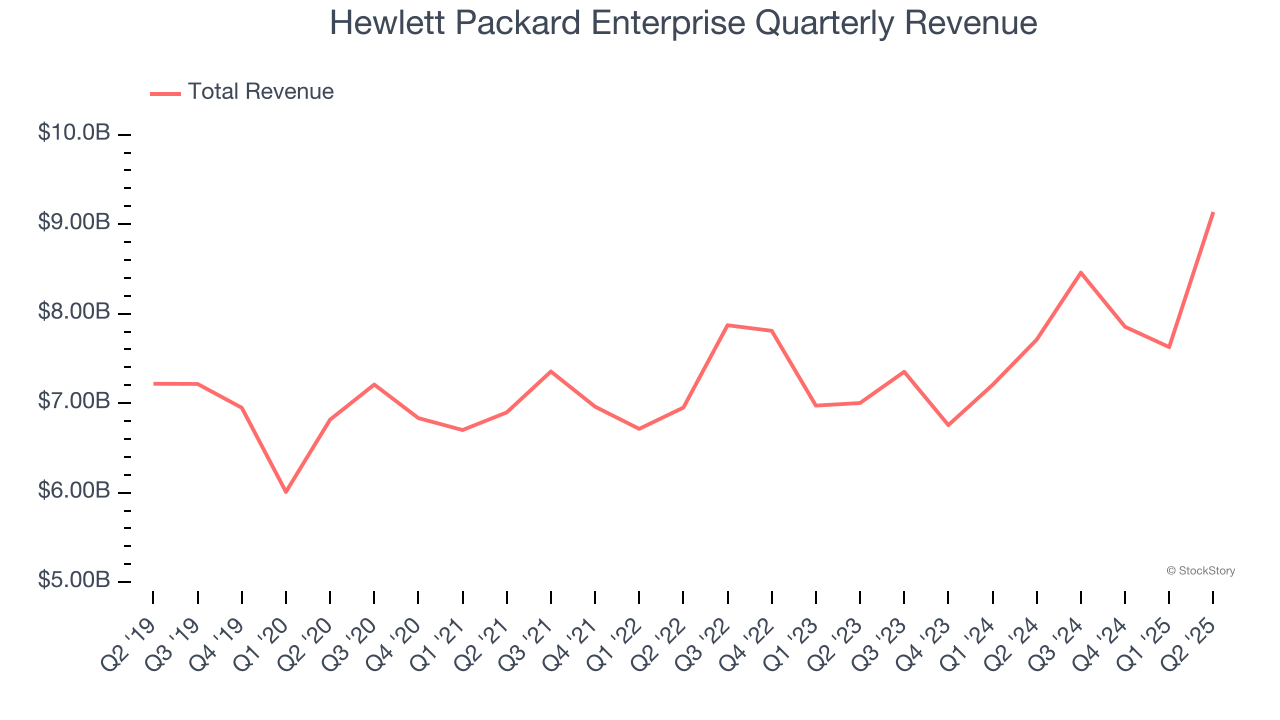

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Hewlett Packard Enterprise’s sales grew at a mediocre 4.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the business services sector.

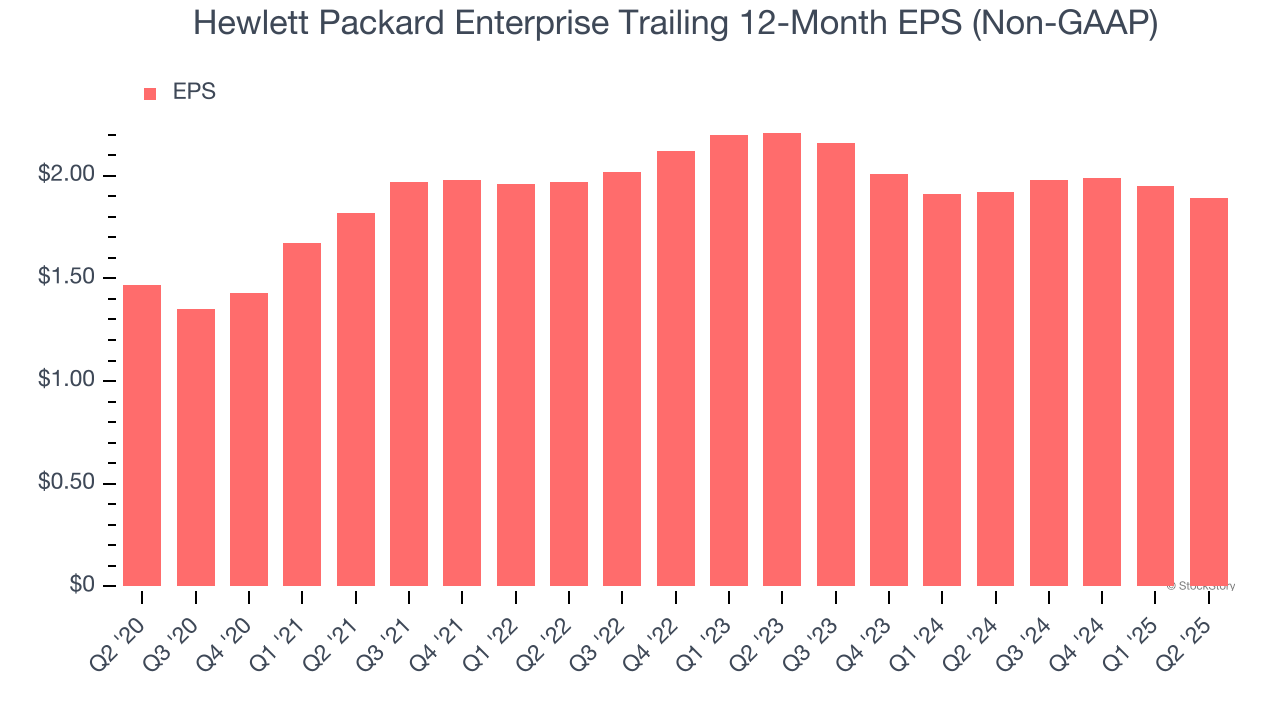

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Hewlett Packard Enterprise’s unimpressive 5.2% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

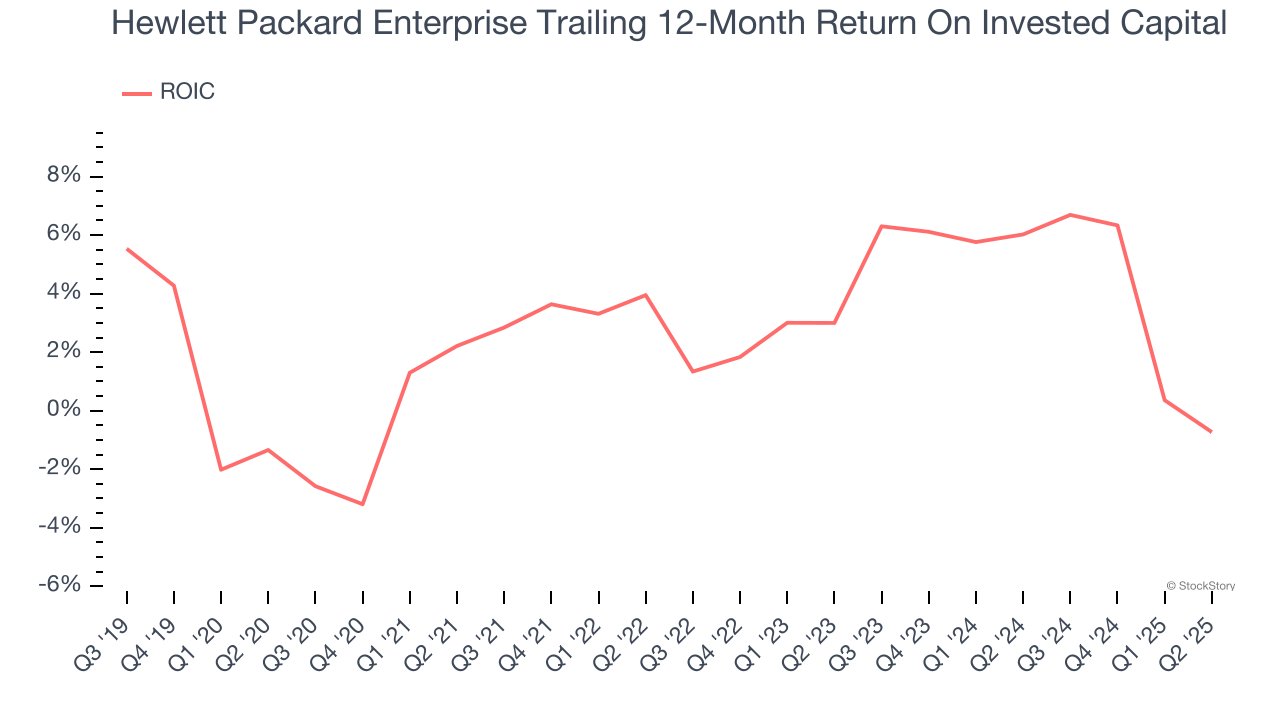

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Hewlett Packard Enterprise historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.9%, lower than the typical cost of capital (how much it costs to raise money) for business services companies.

Hewlett Packard Enterprise’s business quality ultimately falls short of our standards. Following the recent surge, the stock trades at 10.6× forward P/E (or $24.48 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 6 hours | |

| 7 hours | |

| 13 hours | |

| Feb-19 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 |

Top Trump antitrust official leaves post following disputes over big mergers

HPE -6.76%

Associated Press Finance

|

| Feb-12 |

Cisco Memory Chip Warning Sends Down Dell, HPE, Arista, NetApp Shares

HPE -6.76%

Investor's Business Daily

|

| Feb-12 |

Cisco Profit Margin Outlook Sends Down Dell, HPE, Arista, NetApp Shares

HPE -6.76%

Investor's Business Daily

|

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite