|

|

|

|

|||||

|

|

|

Although Lockheed Martin (currently trading at $501.95 per share) has gained 5.6% over the last six months, it has trailed the S&P 500’s 22.9% return during that period. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Lockheed Martin, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

We're swiping left on Lockheed Martin for now. Here are three reasons there are better opportunities than LMT and a stock we'd rather own.

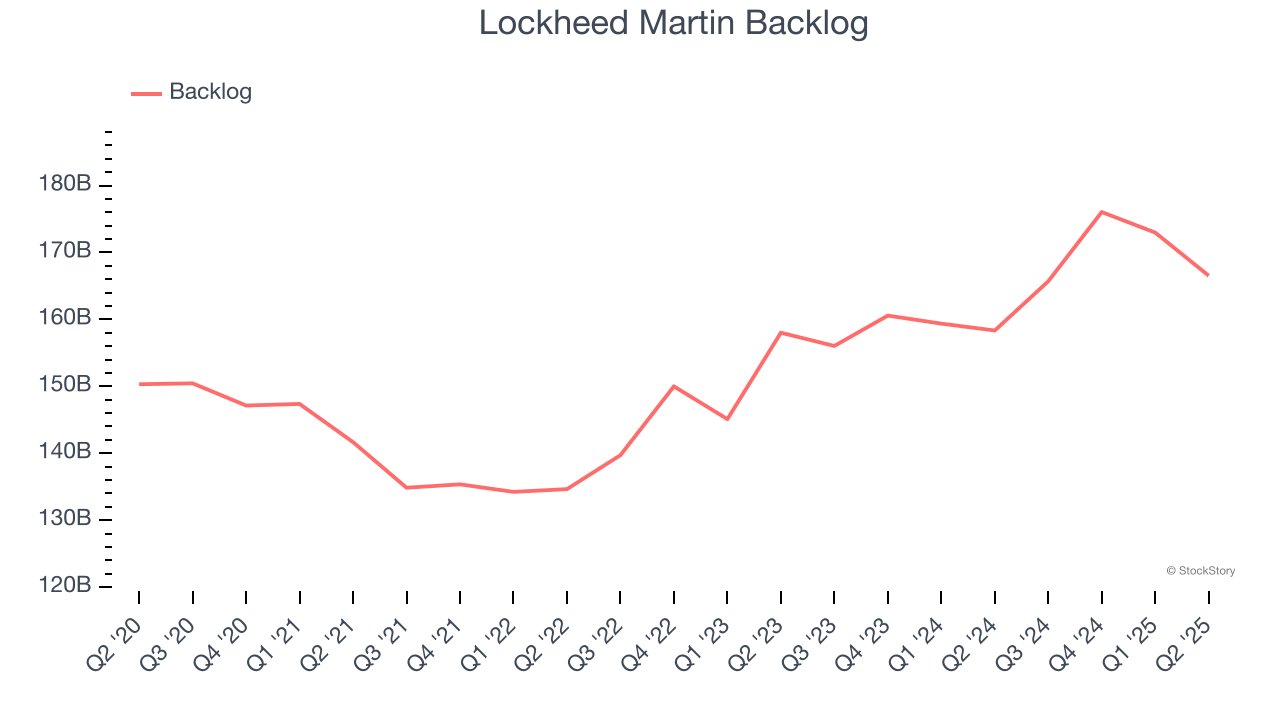

Investors interested in Defense Contractors companies should track backlog in addition to reported revenue. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Lockheed Martin’s future revenue streams.

Lockheed Martin’s backlog came in at $166.5 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 7.3%. This performance slightly lagged the sector and suggests that increasing competition is causing challenges in winning new orders.

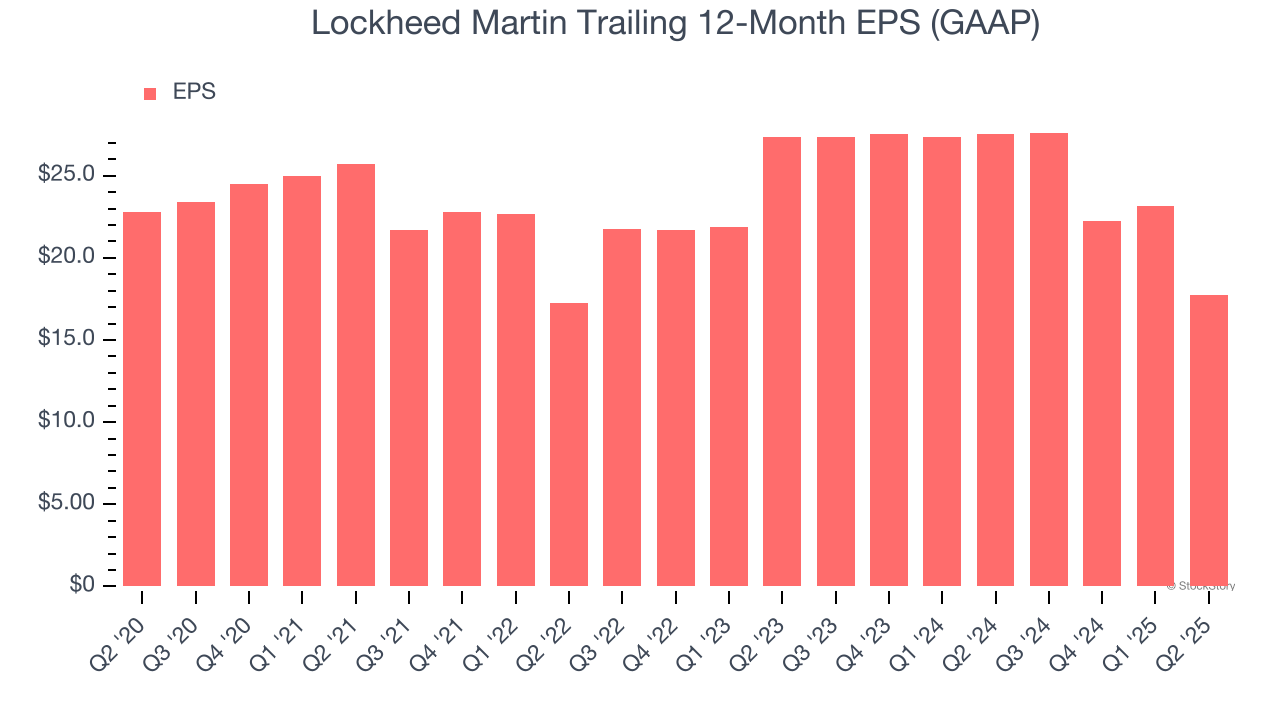

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Lockheed Martin, its EPS declined by 4.9% annually over the last five years while its revenue grew by 2.7%. This tells us the company became less profitable on a per-share basis as it expanded.

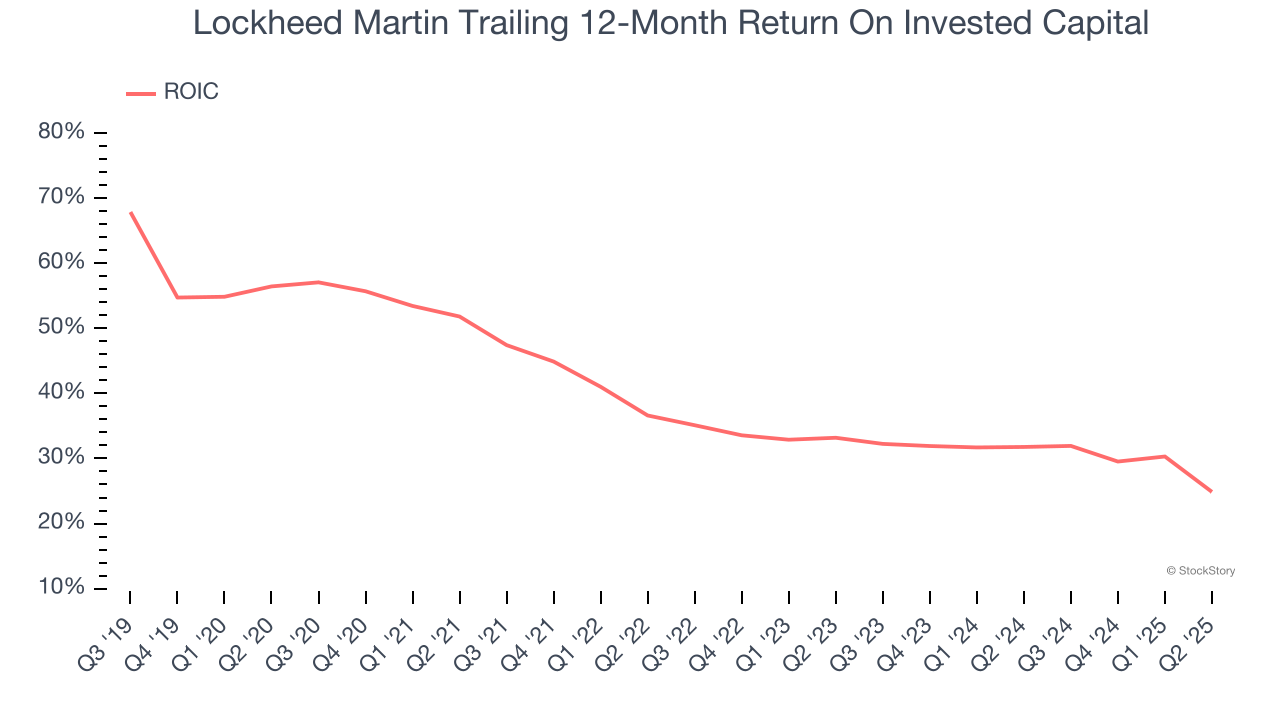

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Lockheed Martin’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

We see the value of companies helping their customers, but in the case of Lockheed Martin, we’re out. With its shares trailing the market in recent months, the stock trades at 18.4× forward P/E (or $501.95 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at one of our all-time favorite software stocks.

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 58 min | |

| Mar-13 | |

| Mar-13 | |

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 |

IPO Leader Set To Launch Breakout As Top Funds Jump In. Impact Of Iran War Raises Questions.

LMT

Investor's Business Daily

|

| Mar-11 | |

| Mar-11 | |

| Mar-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite