|

|

|

|

|||||

|

|

|

As fast-casual dining grows more crowded, Chipotle Mexican Grill, Inc. CMG is finding its once-uncontested position increasingly challenged. Rival chains are leaning on value meals and promotional offers to capture price-sensitive customers, especially in a softer consumer environment. Against this backdrop, investors are asking whether Chipotle’s brand moat, unique mix of quality, speed and loyalty, remains as strong as it once was.

Chipotle still commands powerful brand equity. Management underscored that core offerings, such as the Chicken Bowl, are priced 20-30% below comparable fast-casual meals, making its value proposition compelling despite consumer pullbacks. The company is also reinvesting in marketing to reinforce visibility and engagement, highlighted by the “Summer of Extras” rewards campaign, which drew participation from millions of customers and helped reenergize traffic.

At the same time, Chipotle is strengthening its operational foundation. Restaurant teams are deploying new back-of-house technology like produce slicers and high-efficiency equipment to improve consistency, throughput and prep efficiency. These initiatives aim not only to enhance customer experiences but also to unlock new avenues like catering, where Chipotle currently lags its peers.

Financially, the latest quarter reflected the pressures of this competitive environment: revenue growth slowed to 3%, comps slipped 4% and restaurant-level margins narrowed by 150 basis points. Yet management remains confident in returning to mid-single-digit comps over time, supported by menu innovation, international expansion and digital loyalty engagement with roughly 20 million active members.

Chipotle’s moat is being tested, but with scale, innovation and loyal customers, the brand’s defenses still appear resilient.

Chipotle’s strong brand moat is being tested by established quick-service giants and emerging fast-casual challengers. Taco Bell, owned by Yum! Brands YUM continue to leverage aggressive value offerings, such as $5 combo meals, to capture price-sensitive consumers. The brand’s scale, menu variety and late-night accessibility make it a formidable rival, particularly at a time when Chipotle is working to better communicate the value proposition.

On the other end, Sweetgreen SG is carving out share among health-conscious, digitally savvy diners. With an emphasis on sustainability, app-driven ordering and customizable bowls, Sweetgreen appeals to a similar urban demographic that Chipotle targets. Though still smaller in scale, its technological edge and premium positioning underscore how niche players are encroaching on Chipotle’s customer base.

Together, these competitors highlight the dual challenge for Chipotle: defending affordability against QSR heavyweights while staying ahead of fast-casual innovators.

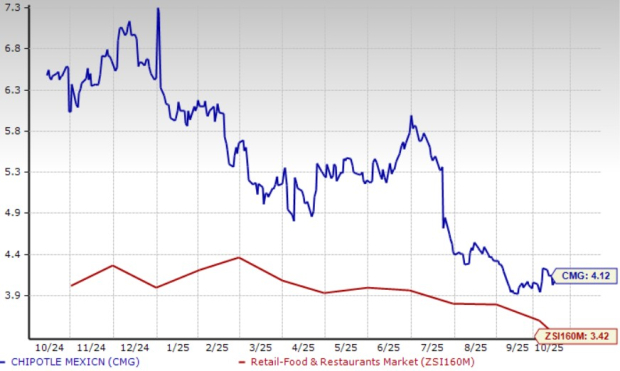

Chipotle’s shares have lost 16.1% in the past six months compared with the industry’s decline of 7.4%.

From a valuation standpoint, CMG trades at a forward price-to-sales ratio of 4.12X, up from the industry’s average.

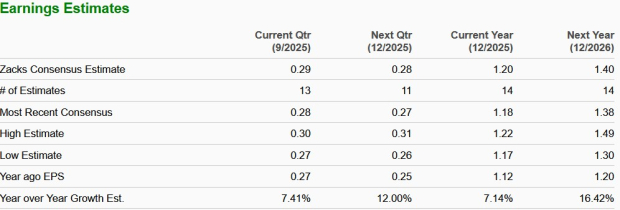

The Zacks Consensus Estimate for CMG’s 2025 and 2026 earnings implies a year-over-year uptick of 7.1% and 16.4%, respectively.

Chipotle currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-18 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite